Welcome back! Wherever you traveled to or even stayed home, I hope you had the opportunity to mentally get away and re-charge for the second (shorter) half of the year. Personally, I find re-entry after vacations to be challenging. The market seems to feel the same way. As I write this holiday delayed monthly note (9/6), both stock and bond markets are struggling to hold on to the upward momentum they enjoyed in the final days of August.

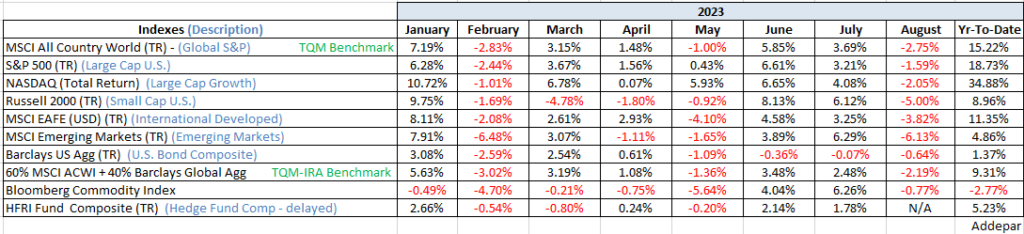

August, as it turned out, wasn’t the sleepy summer month I expected. Market volatility increased, yields climbed markedly and beginning on the first day of the month, equities (via the S&P 500 Index) suffered a 3 weeklong, 5% correction. It was worse for almost every other equity index. Commodities (energy) won the month by losing the least.

The most common pattern of a market correction (defined as down 10%) is best described as two steep declines with a bounce rally in between. The rally in the final days of August, if followed by more market weakness like we’ve had the first two days of the post-labor day week, would define this period as a historically normal correction.

In Morning Notes for the past month, I have shared market concerns ranging from higher for longer rates than the market has priced in, a recession that is delayed but not denied, and inflation that actually goes up into year-end against a Fed still resolute on taming it. These concerns are intertwined with one another and not new to any market narrative. But let me share another concern that is new. On Tuesday (9/5), the S&P 500 equal weighted index (SPW) hit a new low against the S&P cap weighted index (SPX) (see Bloomberg chart below). The Main Street message from this Wall Street data point is, SPW is a better reflection of the broader market, and it is weakening at a much faster pace than the AI influenced SPX. Bulls might say that this is nothing more than the continuation of large caps beating small caps (the AI influence), as we’ve seen for months now. However, that argument is stronger in a rallying mode where more buying is in large caps, less buying in small caps. However, if small caps (with much more representation in the equal-weighted SPW) are leading the market down, as yesterday’s data point suggests, then investors are actively selling small caps. Not incidentally, small caps are the weakest group in a slowing economy, dare I say recession.

Be well,

Mike

Sources: Addepar, BCA Research, Bloomberg, JP Morgan Asset Management, Ned Davis Research

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any investment decisions. The information contained herein was compiled from sources believed to be reliable, but Robertson Stephens does not guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Performance may be compared to several indices. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. A complete list of Robertson Stephens Investment Office recommendations over the previous 12 months is available upon request. Past performance does not guarantee future results. Forward-looking performance objectives, targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are speculative and involve substantial risks including significant loss of principal, high illiquidity, long time horizons, uneven growth rates, high fees, onerous tax consequences, limited transparency and limited regulation. Alternative investments are not suitable for all investors and are only available to qualified investors. Please refer to the private placement memorandum for a complete listing and description of terms and risks. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2024 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.