August 27, 2021

Good morning,

The long anticipated speech from the Jackson Hole Symposium by Jay Powell hits the tape at 10am ET this morning. A virtual mountain of words have been written about what JP will say. There’s no point in adding to that this morning.

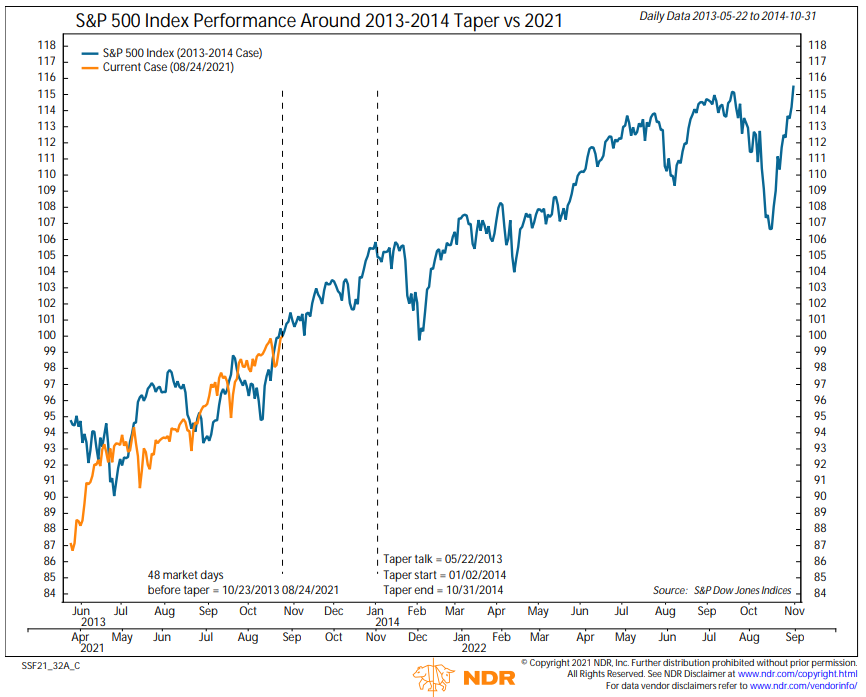

Instead, let’s look back at previous tapers and see how the equity market responded. Ideally, when looking for historical analogs, there would be dozens of past cases to study so that outliers would have minimal impact. Unfortunately, that is not the case. Quantitative easing was first applied in the U.S. during the financial crisis. The only true taper was off QE3 from 1/1/2014 – 10/31/2014. QE1 and QE2 had preset end dates.

With one historical case, it is important to compare and contrast 2013 and today. First, the Fed is telegraphing the taper differently. Taper talk started on 5/22/2013 when then-Chair Bernanke answered a question during Congressional testimony. The shock sent bond yields soaring, with the 10-year Treasury yield jumping 103 basis points from 5/23/2013 to 12/31/2013, the day before tapering began. Second, there is no singular taper talk start date this cycle. Instead, Fed officials gradually moved from “not even thinking about thinking about” tapering to discussing timelines at FOMC meetings.

The macro team at NDR expects taper to start in November and end in June 2022. See chart below, but even discounting the fact that the S&P 500 uptrend is stronger now than 2013, it’s easy to see that Quantitative Easing is not a catastrophe for equities. A nice note to end the week on. Have a good second-to-last of the summer weekend.

Be well,

Mike