By Stuart Katz, Chief Investment Officer

October 28, 2021 – Every year, the markets seem to exhibit some new idiosyncratic risk. Most recently, we saw the tremors caused by China’s abrupt shift in regulatory policy as it tightened control across all facets of society, targeting technology, education and real estate companies in particular.

While these developments have understandably eroded confidence in China’s markets, it would be rash to dismiss the country’s investment potential altogether. They simply mean investors have to be more discerning when it comes to choosing which markets seem primed for performance.

Investors will miss out, however, if they become distracted by the escalating rivalry between the two countries and fail to see the new opportunities these tensions create. There are reasons to be optimistic about China’s innovative trends, despite the accompanying volatility.

China resets EM trajectory

We remain cautious in our approach toward the world’s single largest emerging market. China’s policy announcements are bound to affect markets due to the country’s sheer size and global economic clout alone.

This is especially true with emerging markets (EM), which have seen acute underperformance this year, particularly in equities, where China has been prominent. China’s economic policy also has been inexorably tied to political objectives, which are, in turn, affected by the country’s need to address demographic challenges of its rapidly aging population.

China’s equity markets remain one quarter the size of those in the U.S., despite trailing the country by one rank as the world’s second largest capital market, while China’s bond market is only about one third that of the

U.S. Both are indications there is a lot of room to grow. Investors who fail to compensate for the China under- weighting in their portfolio risk losses from the missed upside of improving domestic quality growth.

We do, however, see strengthening tailwinds for EM as a whole. These include an improving macroeconomic situation, with vaccinations sharply on the rise and Delta finally fading, as well as improving valuations. Additionally, an increased demand for income has drawn investors into higher yielding markets with lower valuations and other improving macroeconomic conditions.

China’s global ambitions in areas like technology innovation, green energy transition and domestic consumer

services give us continued reason to invest there. But investors should be deliberately selective—our firm approach to portfolio construction—as geo-political risks increase and broad ETF index-based strategies have less to offer.

The ‘tech factor’ alters landscape

We have seen over the last year how China’s growing economic prominence and its technological prowess have begun to reshape the investment landscape—and how the blurring of geopolitical, physical and virtual lines has given rise to new thematic investment opportunities.

China, with its state-operated capitalistic system, opted to “partner” with major tech companies to help generate global competitors, recognizing how geopolitical compe- tition intersects with technology in ways the U.S. and its policies have not.

This year, as we hit a stride with a strong economy recovery in the U.S., we see China’s prominence beginning to emerge in other ways, most notably with “data sovereignty,” as it moves to strengthen data protection in what some have called a startling clamp-down on tech companies. This campaign has further blurred the line between technology and geopolitics and heightened fears of China’s economy surpassing that of the U.S.

Data sovereignty is becoming a global issue with many governments taking the view that data collected in a par- ticular country should remain in that country under the jurisdiction of the local government. The decentralized nature of the internet, of course, makes this challenging. China, nonetheless, has recently focused on creating more laws and regulations targeting data accessibility and cross-border transfer of data in what some might call an attempt to catch up to European and U.S. tech- nology regulations.

In this bid, the Chinese Communist Party has focused on China’s largest most recognized companies to show that the government is in control, as if to serve as a warning not to interfere with its authority. DiDi, China’s ride-sharing giant, became the subject of regulators’ cybersecurity probe just after its recent listing on New York Stock Exchange, then ordered pulled from app-store operators over allegations it was illegally collecting user data.

This is a departure from the role of Chinese technology regulators who had previously taken a less hands-on approach, allowing companies to flourish. The government has become more active, however, as technology has become a larger geopolitical issue. Most critically, it has targeted artificial intelligence technology, which relies on data for its development.

How long the DiDi security review lasts will be important to watch in the short term. From a longer-term perspective, the ban is likely another indicator that it will be increasingly difficult to separate technology from geopolitics. It is also a sign we are experiencing the real-time strain of China’s economy surpassing that of the U.S. and will continue to do so over the next several years.

Semiconductors create new fault lines

Another source of friction between the two countries lies with advanced semiconductors, which remains China’s biggest obstacle to becoming a technological leader. In this case, the issue is tied to Taiwanese tensions. China’s chip champion Semiconductor Manufacturing International Corp (SMIC), the world’s fourth-largest chip foundry and China’s best hope at achieving self-sufficiency in semiconductors, has been recruiting talent from the Taiwan Semi-conductor Manufacturing Company (TSMC).

Here, it’s important to note, however, that there are successful U.S. tech companies such as Apple that make up roughly one-fifth of TSMC’s total revenue and have a meaningful percentage of their revenues and manufacturing facilities already in China.

Energy transition raises geopolitical concerns

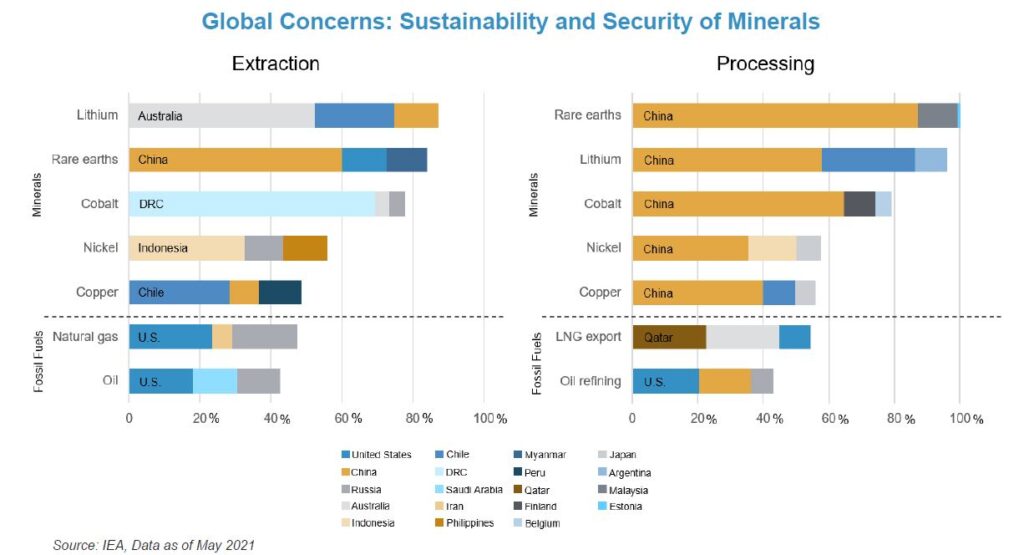

Finally, as the energy transition continues to accelerate, the global economy is transforming from one that is highly de- pendent on fossil fuels, such as coal, natural gas and crude oil, to one more reliant on minerals, such as nickel, cobalt and lithium.

The geographic location of clean energy transition minerals raises geopolitical concerns. According to the Interna- tional Energy Association (IEA), the top three producers account for 50% to 85% of global supply, with a majority of these minerals processed in just a single country—China. Ironically, the process of mining rare earths and transform- ing them into usable materials is expensive and damaging to the environment.

Global trends make their mark

As a backdrop to these developments, we see other global agendas playing less conspicuous roles. Earlier this year, China’s President Xi Jinping held a virtual summit with French President Emmanuel Macron and German Chancellor Angela Merkel, calling on China and Europe to cooperate on tackling global challenges. Europe does not want to lose access to China’s large economy and has been less willing to go along with more aggressive measures pushed by the U.S.

Some on the world stage have found China’s sudden tech industry regulatory interest baffling. But regulation is a short-term pain that leads to a constructive long-term development gain. Despite significant worldwide discussions on tech industry anti-trust and regulatory oversight, no other country has successfully constrained these giant corporations.

The Chinese government is making its attempt to do so during the 100th Communist Party anniversary while creating an environment for further long-term innovation and encouragement of capital formation directly through its domestic exchanges such as Hong Kong, Shenzen and Shanghai. We believe the Chinese government doesn’t want to completely rethink the role of private capital, private enterprise and foreign investors, but rather is trying to find the proper balance for this development story over the long term.

The People’s Bank of China (PBOC), for its part, stated recently it’s committed to supporting higher quality growth while keeping tabs on the digital economy. This creates an opportunity to rebalance into EM, including China. We continue to believe that China will eventually have to prioritize growth over longer-term strategic reform, particularly given the current pressures of elevated energy prices.

For now, the plot thickens as we wait to see where these tensions go next. The China Securities Regulatory Commission, the Chinese equivalent of the U.S. Securities and Exchange Commission, stated recently it has always been open to companies choosing where to go public, saying, “the financial opening to the outside world will continue.”

But investors should watch for a classic “tit-for-tat” negotiating strategy, where the U.S. responds with a move to prevent Chinese companies from listing in its backyard unless it can monitor trust and verify certain accounting and other local Chinese regulatory risks. We shouldn’t forget that the developed world is also focused on many recent Chinese regulatory initiatives as well.

This may feel like an uncertain climate for China’s tech companies. For investors, escalating tensions between the U.S. and China shouldn’t automatically trigger a “flight to safety” though. They should remain overall optimistic about partnering with active management to capture China’s innovation trends and the trajectory of its growth stocks while paying close attention to new developments and matters across its economy and governance regime.

We believe there are strong secular trends in China, which are too big to ignore, where the country will continue to surpass the U.S. in terms of growth in coming years. While finding sources of differentiated growth and positive return in an expected low return world will remain a challenge, we know that consistently underweighting the Chinese engine for next several years will likely only result in missed opportunity.

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advi- sor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is forgeneral informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the infor- mation available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, the opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guaran- tee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as il- liquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment ad- visory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2021 Robertson Stephens Wealth Management, LLC. All rights reserved.Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.