The stock market’s July performance was the living embodiment of the notion that the stock market is not the economy. Yes, they are related and even positively correlated over very wide time spans (years) but their moves are often diametrically opposed when viewed in daily, weekly and monthly time periods. The reason is simple to understand but easy to forget in highly volatile market times. The stock market moves based on what investors believe the macro-economic world will look like in 6-8 months – it is said to be forward looking. Hard economic data is collected and released after the fact – it is said to be backwards looking.

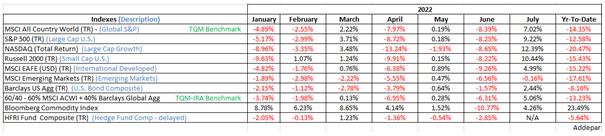

July-released economic data provided further evidence of a slowing global economy. Inflation continued to soar to new highs, economic growth data disappointed and even surveys (soft data) like the Purchasing Manager’s Index (PMI) showed economic activity losing momentum and quickly. What did the market do in July against all this economic blight? See the distinct lack of large red numbers (for a change) under July on the chart below

What’s the market’s message likely imbedded in July’s performance? I think it suggests that a bona-fide economic recession is much less likely in 2022 than was believed only a month ago. And 2023? No one knows for sure, but it would seem reasonable to presuppose the following: if the current rally (see July again) can broaden out and be more inclusive from a sector perspective, a painful recession in 2023 will most likely be avoided. However, if the current rally stalls and cannot advance much more than it already has, the chances of a 2023 recession will loom and market prices may retreat back to previous lows.

We’re watching closely.

Be well,

Mike