With the start of tax season looming, here’s what taxpayers need to know about effective planning amid the uncertainty posed by the partisan split between the House of Representatives and Senate.

By Mallon FitzPatrick and Alicia Denton

January 25, 2023 – Earlier this month, Robertson Stephens Managing Director and Head of Wealth Planning Mallon FitzPatrick and Wealth Planner Alicia Denton were approached by Financial Advisor to share their thoughts on what the split between the Republican-controlled House of Representatives and the Democratic-controlled Senate means for taxpayers and how it will affect tax policy in 2023. Their responses have been shared in full below:

Can the public anticipate fewer tax code changes under a split Congress?

Yes — We expect to see gridlock between the GOP and Democrats as well as within the parties themselves, as evidenced by House Speaker Kevin McCarthy’s confirmation process. Shared goals between the GOP and Dems will likely remain difficult to execute, as each party holds opposing views about how to best legislate.

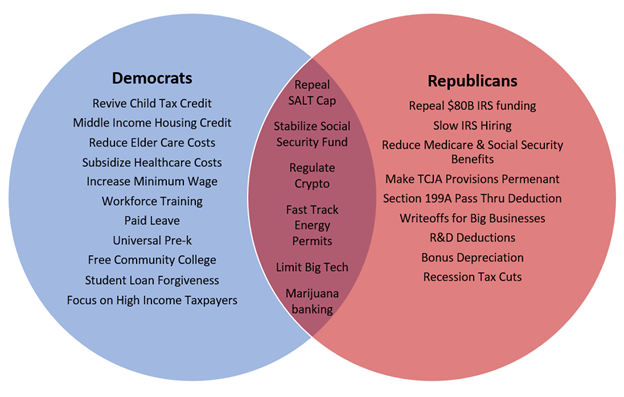

For example, while Republicans and Democrats both say they would like to curb inflation, their proposed solutions vary:

- Democrats have suggested raising the minimum wage and reducing the costs of services such as healthcare, elder care, housing, and childcare. This strategy is at odds with the GOP’s objective to curb government spending on social programs.

- Republicans would like to implement deregulatory policies they claim will spur private sector growth — this includes increasing energy production and boosting corporate tax benefits.

There are a few bills that must be revisited this year and passed regardless of political strife such as the farm bill and government funding bill. Republicans and Democrats alike could use these bills to extract compromises from the other party. The few measures that both parties might agree upon include: repealing the SALT cap since there are more Republicans in the House from high-tax states, regulating cryptocurrency, stabilizing the social security fund, streamlining the energy permitting process, limiting the powers of Big Tech, and allowing banks to accept money from cannabis businesses in states where that particular industry been legalized.

Have investors expressed concerns about potential tax-planning complications in this political environment? What do you tell clients who ask about them?

Clients are far less concerned with tax changes today than they were in 2021 when it seemed that the Build Back Better (BBB) Act would pass. 2021 was a roller coaster of a year for high-net-worth and ultra-high-net-worth clients and the planners who serve them. While we can only speculate as to how this year’s Congressional sessions will play out, there are a few agenda items worth paying close attention to.

With multiple provisions from the 2017 Tax Cut and Jobs Act set to expire at the end of 2025, Republicans will likely attempt to enshrine certain measures such as lower income tax rates into permanent law. However, we cannot count on this as a certainty. We have been advising clients to plan for the known, namely, that income taxes are set to increase while estate and gift exemptions will decrease. Our tax and estate planning discussions with high and ultra-high-net-worth clients have focused on strategies we are implementing to take full advantage of existing and relatively favorably tax laws such as Roth conversions, wealth transfers, and a few others.

Another point worth noting is that while audits on high and ultra-high-net-worth clients are likely to increase, the overall probability of being audited remains low. While the shift in the IRS’s capacities may not be as severe as some have warned, advisors and clients may benefit from understanding the red flags that can raise the risk of an income tax audit. Sizeable transactions, especially those pertaining to income, raise red flags. These include rental losses, business sales, charitable deductions, gifts, cryptocurrency transactions, and foreign transactions. Other audit triggers may be high self-employment income, missed RMDs, suspicious business expenses, failing to report foreign accounts, and self-dealing for private foundations. Clients working with a qualified accountant to accurately report income tax events and structure businesses should have little to fear in the future.

Additionally, the Treasury Green Book released in March 2022 included proposed tax rate increases for high-income corporations and taxpayers in order to raise revenue for ambitious social spending. We are assuming that the White House will float similar proposals in this year’s edition. Typically, these green books spur a lot of press and commotion around their contents upon release. While investors will likely react negatively to these suggestions, we don’t anticipate a gridlocked Congress passing any legislation that will raise taxes; we intend to stress as much to clients.

There are other considerations to consider: Republicans are expected to make a strong effort to salvage the 20% pass-through deduction from businesses to non-corporate taxpayers, another provision of the Tax Cuts and Jobs Act of 2017 that’s set to expire in 2025. The GOP has also conveyed interest in boosting large businesses through deductions for R&D expenses, interest expenses, and bonus depreciation. These changes may have a positive impact on corporate profits. Should the U.S. economy slump further, we can envision a Republican House suggesting a recession-driven income tax cut.

Likewise, Democrats might have to shelve goals such as universal pre-K and tuition-free community college. However, Dems will likely still push for an enhanced child tax credit, student loan forgiveness, and lower healthcare costs via avenues such as drug pricing regulation. Senate Democrats have also proposed a middle-income housing credit to alleviate housing costs.

What’s your best tax-planning advice for wealthy clients this year?

Although the next few years stand to be politically volatile, significant tax law changes may be few and far between. Don’t worry too much about the circus in D.C. and focus on your long-term objectives and what is within your control. Assuming the TCJA expires at the end of 2025, we recommend taking advantage of today’s higher federal estate tax exemption ($12.92 million for single filers and $25.84 million for married couples). For clients projected to have estate tax liabilities — generally seen with estates valued at more than $20 million today — we recommend transferring wealth prior to 2026.

In some cases, transferring wealth efficiently might necessitate setting up trusts, charitable entities, and family LPs or LLCs. It was popular circa 2021 to set up a SLAT or other types of grantors trusts to take advantage of the higher lifetime exemption; this was seen as a pre-emptive step to the BBB Act lowering the exemption. Because it can take time to evaluate different strategies and decide on a course of action, we recommend consulting a wealth manager and attorney to get started. It’s important to remember that given enough time and planning, estate taxes are typically elective.

Moreover, many high-net-worth and ultra-high-net-worth clients have significant assets within IRAs and do not require the funds to maintain their respective lifestyles. Converting the IRA to a Roth stands to be a good estate planning strategy for transferring a “tax-free” account to heirs, especially with the likelihood of new IRS Inherited IRA rules taking effect later this year. Additionally, any Roth conversions should be completed prior to 2026 to take advantage of lower income tax rates, as the highest marginal individual rate is set to increase from 37% to 39.6% that year.

Is there anything else taxpayers ought to expect or plan for with Congress’ current configuration in mind?

Yes — This year Republicans will take control of the House Ways and Means Committee, the chief tax-writing committee of the house. We expect increased IRS oversight and attempts to constrain the $80 billion in funding the IRS received from the Inflation Reduction Act passed last year. Far-right members of the Republican Party have gone so far as saying they would like to abolish an income tax system and replace it with a consumption tax system. While a complete restructuring of the tax system is unlikely to happen in our view, the suggestion provides insight into the divisions permeating the contemporary Republican Party. As a result, Democrats will have to contend with a more right-leaning GOP. For example, should they need to satisfy a Republican House, Dems could concede to IRS funding cuts in order to pass next year’s spending bill. In such an event, a continuously underfunded IRS would likely result in lower audit rates for all taxpayers.

More information on how taxpayers can account for a divided Congress can be found by reading the full Financial Advisor piece right here.