March 2, 2023 – Given how the markets began the year, you might suspect all is fine worldwide. Stocks were up, bonds were up, energy prices had stabilized, and inflation appeared to be abating. Yet we are far from being out of the woods and, in fact, likely to have another rough period ahead of us in the markets. But first, a little perspective on where we have been: the three elephants standing in the room today.

The first is Covid. The global picture continues to evolve in ways we could have little expected just three years ago. If you recall, it was February 2020 when we first learned about the extent of some virus in China. Yet few of us had actually experienced it, nor could any of us have imagined what came next (unless you are a Hollywood screenwriter, in which case there was plenty of material to draw on).

The pandemic turned our world upside down in many ways, many of which we could not anticipate, from global supply chain failure to global awareness of the viral disease. What I learned, and did not previously understand, is that we are deeply social creatures, and we need human interaction like we need air or water. Remove that interaction while also changing most aspects of our daily routine, and people truly suffered. As a natural introvert, I initially found that notion perplexing and actually reveled in the quiet streets and time alone. But as time wore on, even I began to feel the pain of solitude.

We have been able to move beyond a pandemic to living with an endemic disease thanks to some of the most amazing science and biology of our civilization. It was truly a marvel of science in how we were able to manage this crisis through science in ways that were unimaginable just ten years ago. Yet the effects on the economy and our society will linger for years. Ultimately it will make society more resilient while opening our eyes to the perils of nature that should not be underestimated.

On that note, climate crisis is the second tectonic shift I’ve noticed in the past three years. No longer is there a debate on whether it should be called “global warming” or “climate change”. It is now a thing in the public consciousness, from the rapid adoption of electric vehicles to true bipartisan legislation. Unless you live under a rock, the impact of a century of industrialization combined with vicious attacks on our ecosystem has led to weather extremes never before witnessed.

I can’t pinpoint the event or series of events that triggered this shift in perspective, but it is tangible and happening. The Inflation Reduction Act (poorly named) may be one of the most important pieces of legislation in our generation, laying the groundwork for not just industrial expansion to abate the impacts of climate change but a conscious drive to create a robust and thriving economy to support it. In short, it could be a win-win. But time will tell, with execution being where all good intentions go to die. The years ahead will be critical for both the environment and the role that we can play in its evolution while potentially turning crisis into opportunity.

Third, and perhaps most pressing, is the war in Ukraine. I write this on the one-year anniversary of the invasion, and even I forgot some of the horrors of the past year. The Bucha Massacre still sits as one of the worst insults to human dignity and humanity in this era, yet it has slowly faded from memory as each month brings new outrages. How the war ends is unclear, nor is it clear how much further the U.S. and Europe are dragged into a direct conflict with Russia. One perspective that might be most disconcerting is that Putin will never accept defeat as long as he is alive, irrespective of the number of lives lost by either side.

What is clear, however, is that Putin has already lost. Whatever goals he may have had in mind at the outset, they have failed. NATO is now stronger than ever, the role of the U.S. in global politics is firm, and Europe will no longer depend on Russia for its energy needs. In short, Putin has started Russia down the path of global irrelevance (although their nuclear arsenal will always put an asterisk on that statement). As the Russian economy continues to shrink, and they are further isolated from their neighbors to the west and maybe even the east, the world will move past Russia and look for alliances and trade partners they can trust.

So with all these elephants in the room, how is the world of money and investing doing? Despite what you might have experienced in 2022, things are better than feared. What happened with stocks and bonds — sizable declines in both — was both needed and expected. The timing of these events is always the elusive part, but stocks were vastly overpriced thanks to years of Quantitative Easing along with some aggressive fiscal stimulus in response to Covid. The same could be said of bonds after a forty-year bull market with few pauses following the last inflation scare in the 1970s. What we did see was a relatively orderly decline in asset prices. While it hurts portfolios, it could have been far worse.

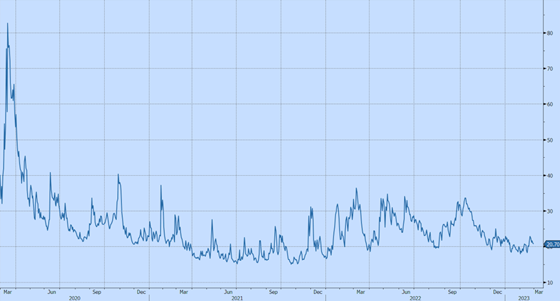

For the year to date, stocks continue to sit in a range-bound conundrum, limited in upward movement by years of overpricing, flat corporate earnings, and a general concern about the economy. While the selloff last year was painful, with the NASDAQ down as much as 30%, it was far better than it could have been given the above factors. Valuations alone say that a larger correction was warranted. One such valuation measure, the Shiller CAPE Ratio, the market “should” have corrected another 20% from where it is today to get to long-term averages. This is not set in stone, and there are always caveats to such an assessment, but that gives us a measure of what we could have experienced.

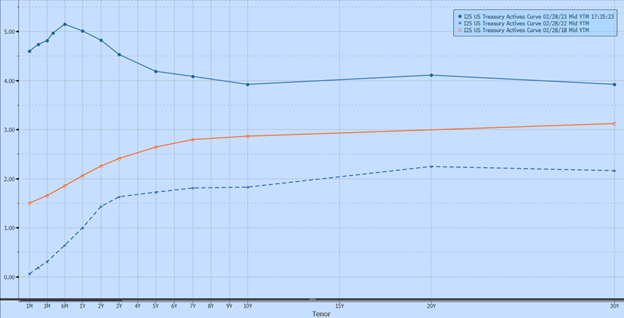

As discussed previously, the yield curve is the most disturbing bit of market data. As seen below, the inversion at the shortest end of the curve and the suppressed rates at the longest-end is unprecedented. Typical inversions of past recessions involve the 2-year and 10-year rates, effectively a mid-curve comparison, while the longest rates always stayed at or above the 2-year. Today one can invest in safe Treasuries at 5% for one year, while you can’t touch those rates for anything longer. The premium for the long-term tie-up of your money is gone, and the incentive is to park money for the short-term. That dynamic alone will create a strong headwind for any short-term stock recovery.

What happens next is never clear, but a soft economic landing is not a likely scenario despite the hopes of many. The Fed will continue to raise rates until they see clear signs of inflation reduction across all the major indices. Given January’s inflation data, that moment is still many months away. The Fed has been clear that they will prioritize inflation controls over a growing economy. Rate raises combined with Quantitative Tightening should do the job of controlling inflation, but don’t expect the economy also to thrive.

Should one of our elephants in the room get spooked, a mild recession could quickly turn into a deeper one. Spook two of them together, and you have a more dire situation that would require aggressive Fed action, which is not always a bad thing given how we have recovered from two major crises in the past 15 years. In some ways, the markets were pricing this potential into the January rally with the expectations of a near-term rate cut, a curious paradox of the equity markets. But as always, time will tell.

– DBM

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any investment decisions. The information contained herein was compiled from sources believed to be reliable, but Robertson Stephens does not guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Performance may be compared to several indices. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. A complete list of Robertson Stephens Investment Office recommendations over the previous 12 months is available upon request. Past performance does not guarantee future results. Forward-looking performance objectives, targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. Please refer to the private placement memorandum for a complete listing and description of terms and risks. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2023 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.