February 27, 2023

Good morning,

The shortest month of the year is coming to an end and none too soon. The S&P 500 Index (SPX) had its worst week since December and was down -2.67% last week. February has taken back about half of January’s gains. A -4.5% correction on the SPX is not a statistical outlier. It is a rather normal market move, especially considering the market rally from the October lows through January. Recall the record overbought market condition at the end of January. A correction was overdue.

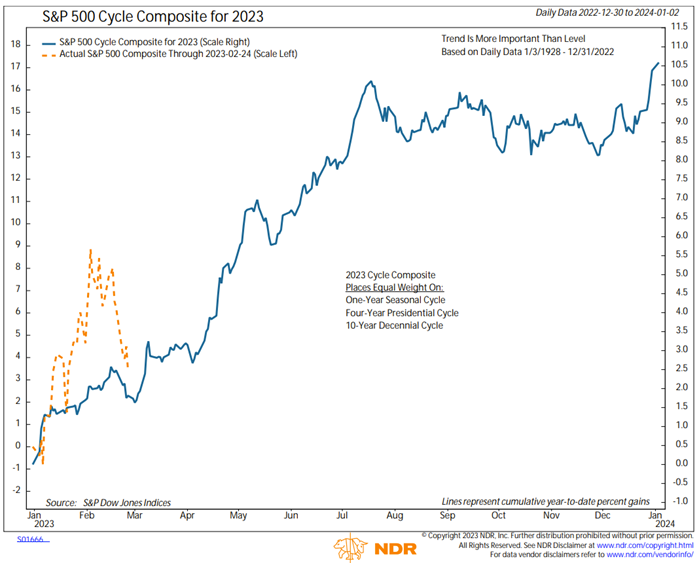

I do not know if the correction is over or even if the February selloff is not the beginning of a downward move to new lows for the market, as some market strategists are saying. But the next two weeks are unusually quiet from a key-economic-data perspective, the overbought pressure weighing on the market is gone, and some weakness in February was due according to the Cycle Composite for 2023 -see chart below.

Remember the three unequal legs of the market analysis stool? Don’t fight the tape (trend) – 50%, don’t fight the Fed – 30%, and beware of sentiment at extremes – 20%. Today, the sum of trend evidence leans bullish. It is not overwhelmingly bullish like you might see at the beginning of a bull market. It is just bullish enough to change the trend from downward to upward, but not enough for the uptrend to qualify as a bull market (yet). The Fed is still tightening – bulls get no help there. Sentiment, as mentioned, is neutral now. In sum, we have a market that, at least for now, leans slightly bullish. It appears as unlikely to turn into a runaway train upward as it does to collapse into a waterfall decline downward. We stick with the mildly bullish prognosis for now and until the market message turns more definitely bullish or bearish.

Be well,

Mike