April 17, 2023

Good morning,

For weeks now, in the Morning Notes and my last monthly note, I have expressed concerns over what has appeared to me to be signs that the probability of a recession in late 2023 – early 2024 is rising. My investment posture has been cautious. The rising fear of a recession and commensurate price declines in stocks has been based on macroeconomic and fundamental signals ranging from a resolute Fed committed to taming inflation, a regional bank liquidity tremor that likely dampens loan activity, and elevated earnings estimates that have yet to be adjusted for any downtick in economic growth, let alone a recession.

Meanwhile, on the technical side of the market analytics ledger, there have been more bullish signs than bearish ones. An honest appraisal of the technical picture of the market today would have you leaning bullish. The near-term data is more bullish than the longer-term data. In other words, you could afford to be constructive on stock prices near term (wks) but only neutral, at best, for longer terms (months).

There is one market condition that exists today and possibly another one in two weeks that may cause cautious investors discomfort. Structurally, in terms of investor positioning, hedge funds, as a class of investors, are massively short S&P Futures. The reason this is structurally important is that it is an extreme condition. Leveraged funds are at a record net short as a percent of open interest. It means that the vast majority of those who put their money on the line each day, with leverage, is betting that the market will go down very soon. Betting against these investors is typically not a smart move, but when any trade gets overwhelmingly one-sided, smarts go out the door and market dynamics walk in. It means the slightest surprisingly good news could create a significant short squeeze as many funds will be forced to buy-in and cover their shorts. It’s a condition where a little buying can beget a lot of buying, and the market, for a time, detaches from fundamentals.

Another possible bullish trigger is the market’s belief that the Fed will pause its tightening after the next rate hike in two weeks. In the post Greenspan era, stocks have consistently rallied around the last rate hike. This may not even be the last rate hike, but given the market’s willingness to react to their own bullish narrative regardless of Fed-speak, the May 3rd rate hike and comments by the Fed might be the catalyst for stocks to lift further. One other point that warrants mention – stocks have rallied 2-5% through most earnings seasons for the past few years. Friday was the first day of the current earnings season.

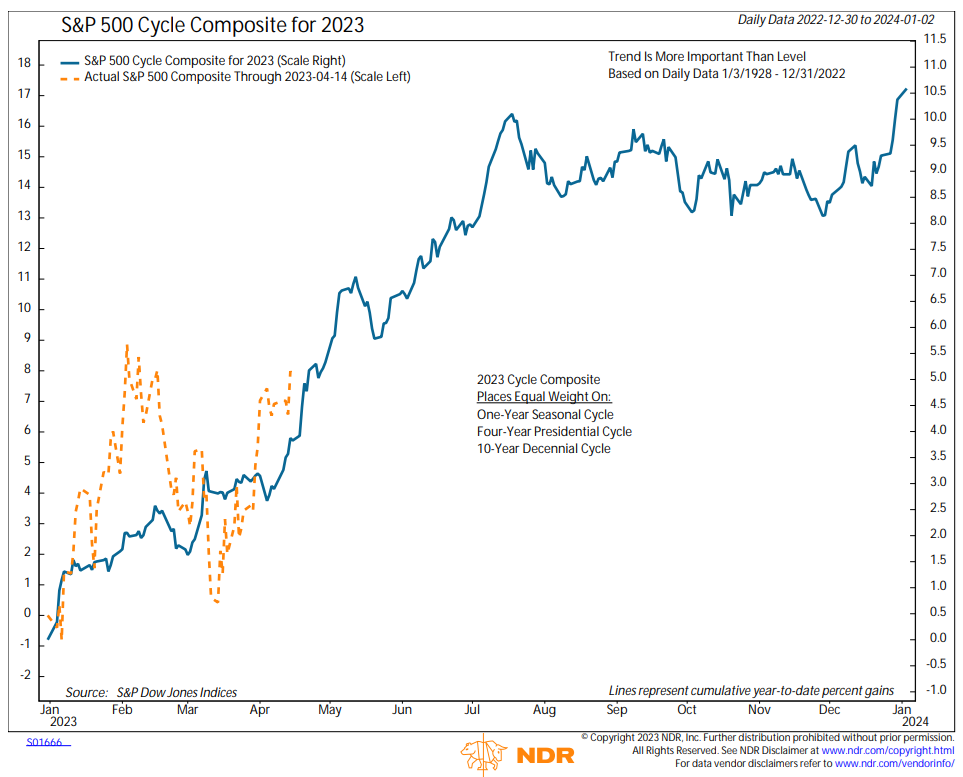

You have seen the following chart several times a year, each year for years. It is the Cycles chart. A combination of the 1yr, 4yr, and 10yr cycles is drawn each January prospectively and watched all year to see if cycle influences are strong in any given year. This year may be one of those years where the market tracks its historical cycle path closely.

Be well,

Mike