June 5, 2023

Good morning,

The new week begins with the fixed income market still struggling with last Friday’s strong payroll figure (meaning yields are up again / prices are down). Fed Fund Futures are now pricing in a rate hike at next week’s FOMC meeting (Jun 14) at a 25% probability. That is up from a zero probability a month ago. Equities have shrugged off the higher rate of re-calibration with the aid of the AI frenzy. Although, in fairness, on Friday, the price action broadened out significantly and it looked much healthier for the bull argument. However, Futures are flat this morning and we’ll need a lot more than a one-day broad-based rally to lower our cautious flag.

Poking the bear argument, a bit now; perhaps Friday marked a change in tone as recession fears were dismissed by another strong labor report. After all, an economic contraction is the greatest threat to risky assets. At some point, one would have to think that the interest-rate backdrop would start to have an impact. And here is the key point, perhaps it already has been having an effect, looking at the average small cap and S&P 500 stock. The question is whether the AI complex can continue its ascent in perpetuity without feeling the heat from yields. Forecasting when it will happen is a lot harder than saying if it will happen.

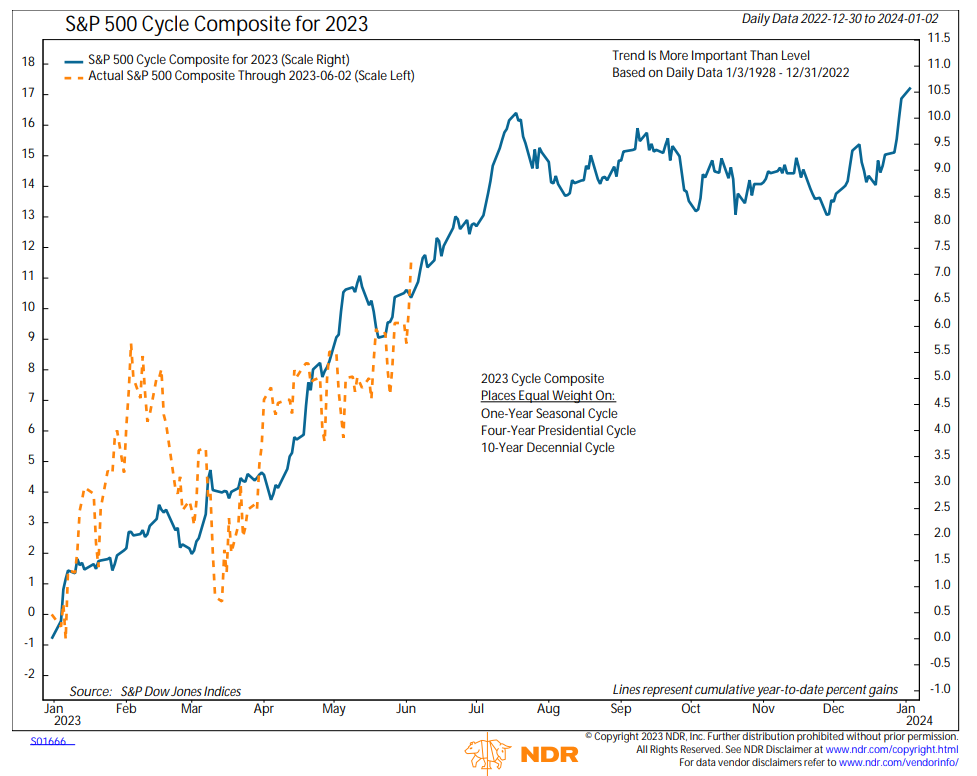

One tool that hints at what might be ahead and something you’ve seen in these Morning Notes for years now is the Cycle Composite Chart (below). It supports a breakout of the equity market’s 10-month trading range and suggests an uptrend into mid-July. From a cycles perspective, the bullish message for the 2023 Cycle Composite in the first half is driven by pre-election year stimulus, which has been due to COLA adjustments in 2023. There is nothing in the cycles chart about artificial intelligence.

Back in March, we talked several times about upcoming discomfort for the cautious. Well, here we are.

Be well,

Mike