Economies: growth was as surprising in April as it has been since the start of the year – economic data showed that it was another positive month for the global economy, with growth remaining remarkably resilient in the face of higher interest rates. U.S., Eurozone and UK Purchasing Managers Index (PMI) surveys all beat expectations. China’s Q1 GDP print was also stronger than expected.

Inflation: falling energy prices helped bring headline inflation down in developed economies. OPEC announced a cut in production aimed at stabilizing oil prices at around $80/barrel. While this was a negative surprise to central banks globally (all of them fighting against inflation), even $80 oil, compared with sky high 2022 prices, means energy should still be a drag on inflation for at least a few more months.

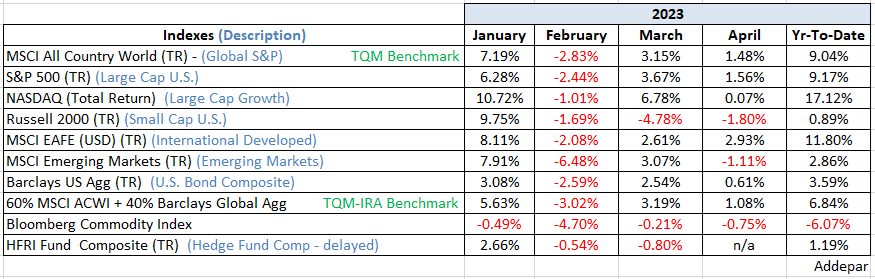

Thus far this year, positive economic momentum globally has supported risk assets. Just a little less so in the U.S. as we have had to live under the cloud of further stress in the banking sector. See returns below.

As widely expected Wednesday (5/3), the Fed raised Fed Funds another 25 bp (basis points) to 5.25%, the highest since September 2007. The Fed has raised rates a total of 500 bp since March of last year, making it the fastest hiking cycle ever. However, it never started out in such a deep hole either. In the Fed’s statement accompanying its hike announcement, it can be inferred that they will not make further hikes unless the data warrants on a meeting-by-meeting basis – the definition of a hawkish pause.

The Fed seems to be counting on tighter credit conditions (regional bank stress) to replace some of the rate hikes that may have been needed to achieve their “sufficiently restrictive” rate level, thought to be closer to 6% only six weeks ago. By pausing, the Fed implements their “hope and pray” policy – it hopes falling inflation and tighter credit will allow policy to be sufficiently restrictive and prays that nothing else breaks.

For an economy widely expected to be headed for a recession of some magnitude over the next 12 months, valuations seem too high, earnings estimates seem too high and inflation, in front of a Fed resolute on breaking it, seems too high. I remain cautious. The only reason I can think of for the equity market to go much higher from here is that I can’t think of a reason for the equity market to go much higher from here. And I know the market will do what fools the most. With what may be the least unexpected recession on record ahead, I am uncomfortably cautious – just like everyone else, it seems. I hate crowds.

Be well,

Mike

Sources: Addepar, Bloomberg, JP Morgan Asset Management, Ned Davis Research, Robertson Stephens Investment Office

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any investment decisions. The information contained herein was compiled from sources believed to be reliable, but Robertson Stephens does not guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Performance may be compared to several indices. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. A complete list of Robertson Stephens Investment Office recommendations over the previous 12 months is available upon request. Past performance does not guarantee future results. Forward-looking performance objectives, targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are speculative and involve substantial risks including significant loss of principal, high illiquidity, long time horizons, uneven growth rates, high fees, onerous tax consequences, limited transparency and limited regulation. Alternative investments are not suitable for all investors and are only available to qualified investors. Please refer to the private placement memorandum for a complete listing and description of terms and risks. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2024 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.