April 10, 2024 – The fall of 1982 was truly a depressing economic period. In November, unemployment hit 10.8%, its highest rate since the great depression. Flint, Michigan, experienced the highest unemployment rate of any metropolitan area, with 23.4% of the labor force out of work.[1] Even President Ronald Reagan, then in the second year of his presidency and trying to soothe a reeling nation, was forced to admit that “behind every one of those numbers are millions of individual lives — young couples struggling to make ends meet, teenagers looking for work, older Americans threatened by inflation, small businessmen fighting for survival, and parents working for a better future for their children.”[2]

The recession of 1982 came on the heels of a multi-year battle with inflation. After reaching 11% in 1974, inflation decreased to 5.7% in 1976, only to top out at 13.5% in 1980.[3] By 1982, the Federal Reserve was well on its way to getting inflation under control, but at a devastating price to the American economy. Still, the Fed chairman Paul Volcker argued that “the inflationary process, after continuing for years, is embodied in a whole pattern of economic, social, and political behavior that tends to sustain — and accelerate -its own momentum.” Only “starving the inflationary process by restraining money and credit long enough can ultimately curb that behavior”.[4]

There’s no doubt that this episode in history looms large in the minds of Fed Chairman Jerome Powell and the FOMC members as they debate the timing of the much-awaited rate cuts. While the 2020s are different than the 1970s and 80s in many ways, the fundamental dynamic of entrenched inflation is one that the Fed can’t ignore. That’s why February’s inflation reading of 3.2%, a slight increase over January’s 3.1%, prompted many to question if and how many rate cuts the Fed would carry out in 2024.[5]

At least for the time being, the Fed is maintaining its expectation that inflation will continue to ease, reaching 2.4% by year-end and allowing for three interest rate cuts this year. While this is certainly soothing to investors, it could change in a hurry should inflation not play along. Don’t expect the Fed to take any chances, certainly not while economic growth remains robust. If today’s economic reality seems strained, a return to the 1970-80s unending cycle of inflation and recession would be infinitely worse. In the meantime, we’ll keep waiting.

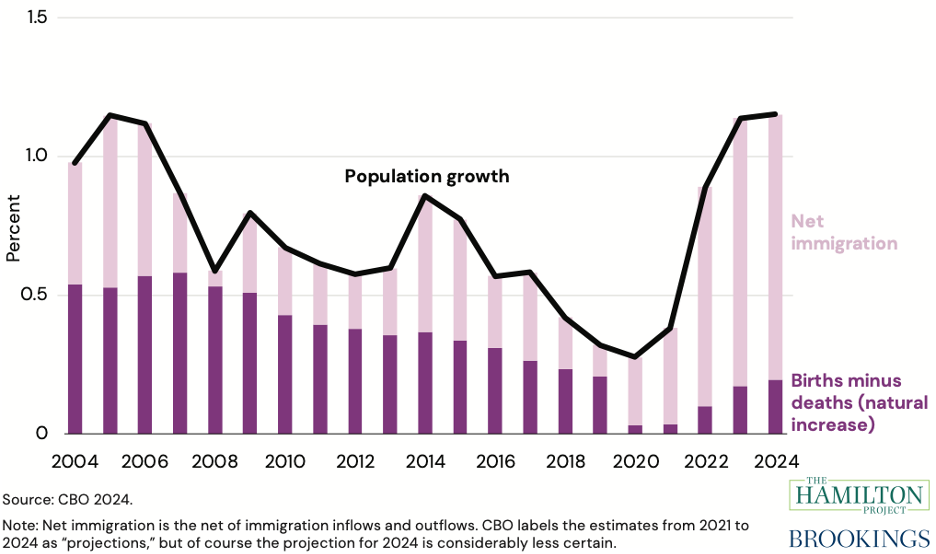

We’ve spoken here before about some of the reasons the US economy continues to defy expectations—a buildup of savings during Covid, extensive government savings, and increased productivity. But a new explanation has recently begun to emerge that help explain how prices have been coming down despite the tightness in the labor market—immigration.

Prior to the pandemic, the CBO estimated that sustainable monthly employment growth in 2023 would range from 60,000 to 130,000 based on the prevailing population growth and employment trends.[6] In reality, employment grew by 250,000 jobs a month in 2023, almost double even the most optimistic estimates. The main reason for this appears to be immigration, specifically, the spike in immigration that began in 2020—see Chart 1. A recent analysis by the Brookings Institute suggests that with the current level of immigration, the US economy could support up to 200,000 new jobs a month in 2024 without stressing the labor market or creating inflationary pressures.[7]

Chart 1: Demographic factors that contribute to population growth, 2004 to 2024. Starting from 2020, net immigration population growth surpassed natural population increase. Source: CBO, the Brookings Institute

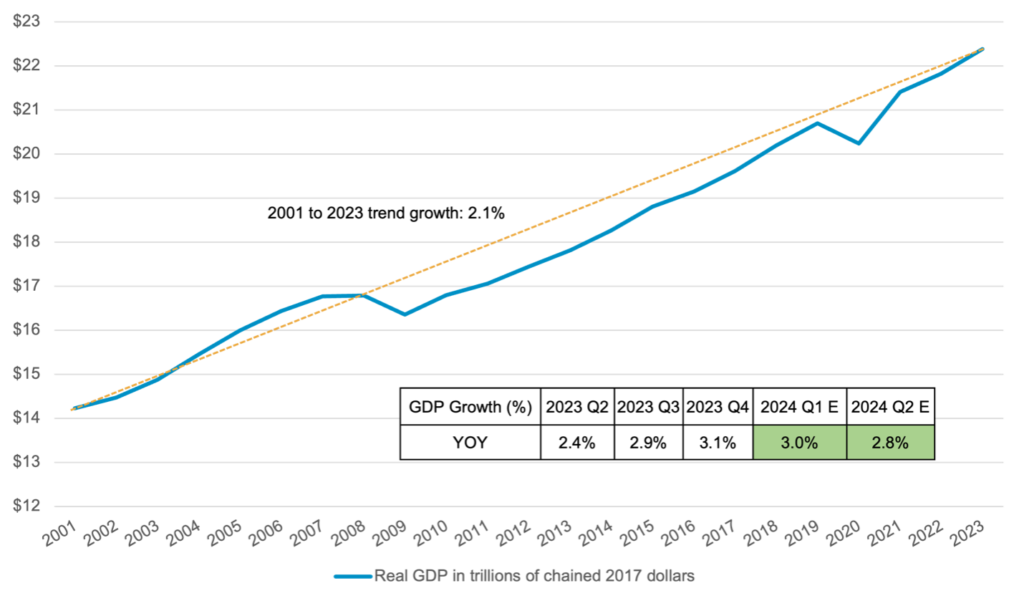

In all, the US economy is wrapping up a strong quarter of economic growth, albeit with weakness continuing in certain sectors like commercial real estate, and mild cracks beginning to appear in others like consumer balance sheets. Still, a recession doesn’t appear imminent, barring unforeseen incidents. While the national economic fallout from the collapse of the Francis Scott Key Bridge in Baltimore is expected to be limited, it’s a good example of the type of unforeseen event that could tip an economy into a recession.

Chart 2: U.S. Real GDP in trillions of chained (2017) dollars and YoY growth, 2001 to 2023. Trend growth is measured as the average annual growth rate. Source: Bloomberg Finance and U.S. Bureau of Economic Analysis.

Globally, tensions remain high as the war in the Middle East drags on with no obvious end in sight. Glimmers of hope for a ceasefire in Gaza have failed to materialize, though discussions about a mega-deal involving Saudi Arabia appear to be back on the table. The situation in Ukraine meanwhile continues to deteriorate, and it’s unclear whether the country can contain the expected Russian summer offensive.

Economic news from around the world was slightly more optimistic, with Europe showing early signs of revival after a rough 2023. Global economic tailwinds would be especially important if the US economy begins to slow. The global outlier remains China, whose economy continues to stagnate.

The Markets

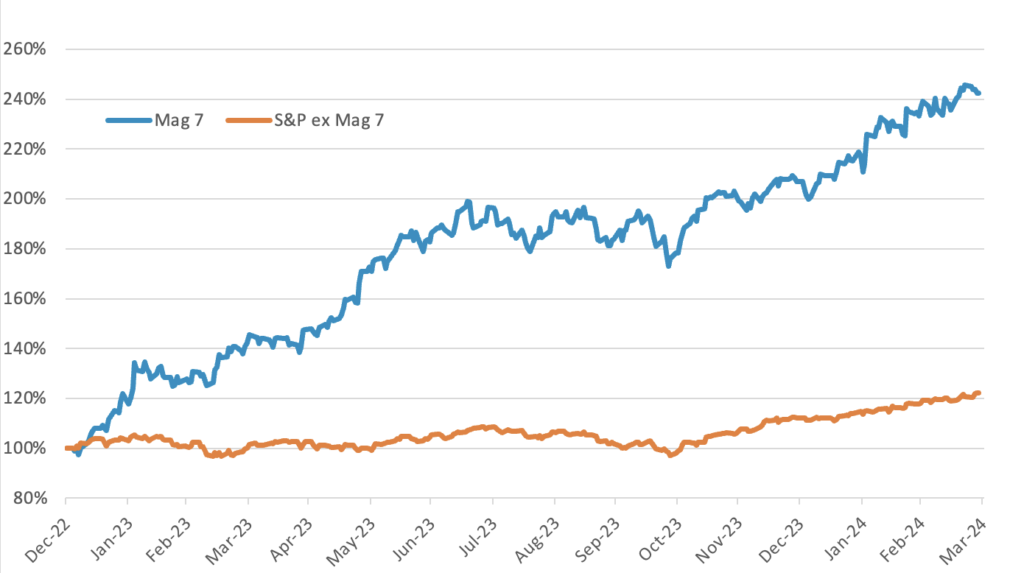

After a jittery January, the stock market resumed its upward climb buoyed by the strong economy, with the MSCI All World Index ending the quarter up 8%. Whatever concerns February’s inflation reading triggered in the bond market were nowhere to be seen in the stock market. The market remains highly concentrated, with the Magnificent 7 adding over 140% from January 1, 2023, while the remaining S&P 493 have added only 23%.

Chart 3: Performance of the Magnificent 7 and the S&P 500 without the Magnificent 7, December 31, 2022, to March 31, 2024. The S&P 493, meaning the S&P 500 without the Magnificent 7, rose only 23% from 2023, while the Magnificent 7 added 142%. Source: Bloomberg Finance.

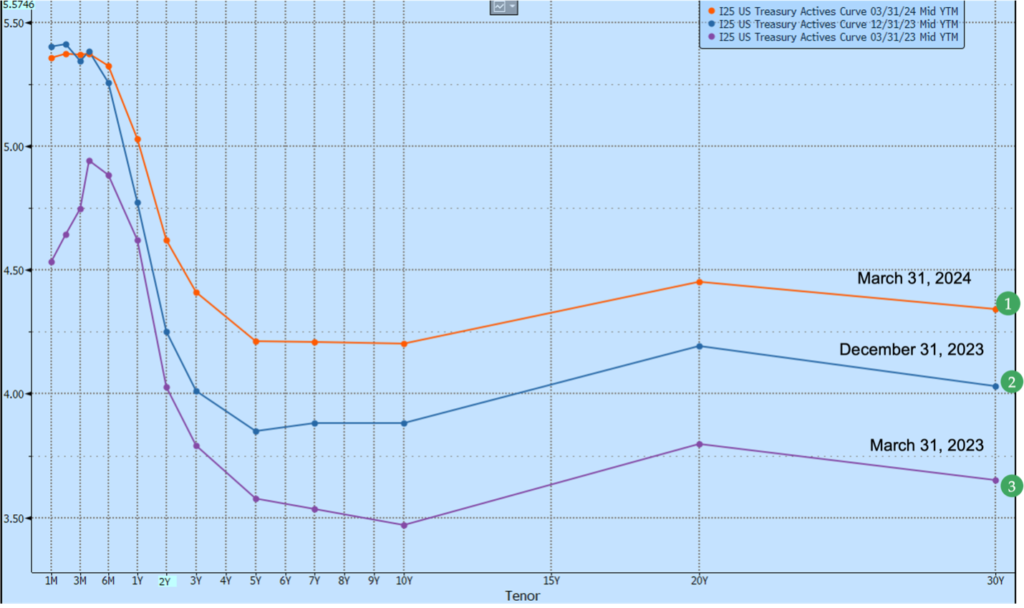

The bond market, meanwhile, was less sanguine in its reaction to the inflation data. The horizontal shift of the treasury yield curve between December and March (see Chart 4) suggests that investors not only expect rate cuts to be delayed but are gearing up for higher interest rates for the foreseeable future. Higher rates mean lower prices, and accordingly, the Barclay Global Agg ended the quarter down 2.1%.[8]

Chart 4: US Treasury Active Curve, March 31, 2024, December 31, 2023 and March 31, 2023. The horizontal shift of the treasury yield curve between December and March suggests that investors not only expect rate cuts to be delayed but are gearing up for higher interest rates for the foreseeable future. Source: Bloomberg Finance.

The Outlook

We expect inflation numbers and the resulting monetary policy to be the main driver of economic outcomes for the remainder of 2024. While the economy remained strong in the first quarter of 2024, the longer interest rates stay high, the greater the chances that something breaks, turning an economic slowdown into a recession. There are, as of yet no obvious contenders for the role, but then again, there rarely are. Commercial real estate remains deeply troubled, but most economists expect the fallout to be limited to regional banks.

Also on the minds of many is the upcoming US election. With the candidates from both parties all but confirmed, this appears to be an election few are looking forward to. Still, it’s important to detach political sentiment from attitudes toward the economy, and we here will do our best to focus on the latter while discussing the impact of different policy proposals.

Finally, the conflicts in Ukraine and the Middle East are not only a source of devastating losses but are also a potential destabilizer of a fragile global order. Let us hope for peaceful outcomes to these and the many other conflicts causing pain and suffering around the world. In the meantime, these uncertainties are a good reminder to make sure the risk level in your portfolio is appropriate for your needs.

Wishing us all a warm and peaceful spring.

— AMD

Photo Credit: ppmsca 03433 https://hdl.loc.gov/loc.pnp/ppmsca.03433

[1]https://news.google.com/newspapers?id=UqQfAAAAIBAJ&sjid=KdYEAAAAIBAJ&dq=unemployment%20rate%20by%20state&pg=1321%2C2664591

[2] https://www.reaganlibrary.gov/archives/speech/address-nation-economy-october-1982

[3] https://fred.stlouisfed.org/graph/?g=1jGaT

[4] https://fraser.stlouisfed.org/title/statements-speeches-paul-a-volcker-451/time-backsliding-8243/fulltext

[5] https://www.bls.gov/opub/ted/2024/consumer-prices-up-3-2-percent-from-february-2023-to-february-2024.htm

[6] https://www.hamiltonproject.org/wp-content/uploads/2024/03/20240307_ImmigrationEmployment_Paper.pdf

[7] https://www.hamiltonproject.org/wp-content/uploads/2024/03/20240307_ImmigrationEmployment_Paper.pdf

[8] Source: Bloomberg Finance

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2024 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.