April 18, 2024

Good morning,

Finally, an equity market pullback. Almost on cue, as the 2nd quarter got underway and investors had been enjoying 5 months of historically low downside volatility, the S&P 500 Index (SPX) began its overdue pullback. It has not endured a -3% pullback (a minimum threshold by definition) since 10/27/2023 – 105 days puts this stretch in the historically long category. More on this down below.

Stronger-than-expected jobs, manufacturing, CPI, and retail sales data suggest that inflation is sticky enough and economic growth is solid enough for the Fed to wait for more evidence before cutting its target rate. Both the two-year and 10-year Treasury yields have hit five-month highs.

Good economic numbers, matched by a decent start to Q1 earnings season, should not be reasons for a significant sell-off. But overly bullish sentiment left little cushion for uncertainty – enter growing geopolitical instability and a pullback has begun.

Historically, early pullbacks following strong uptrends (SPX up 25% in 5 months qualifies) are typically short and shallow and occur in the early stages of a recovery cycle. However, short and shallow doesn’t hold up to historically long periods of low downside volatility (above), late in a recovery cycle, which is where we are.

Given the offsetting historical records for pullbacks, we’re left with closely monitoring the technical damage as the full extent of the pullback/correction unfolds. The good news, technically, is the sentiment is no longer bullish – so we’ve got that going for us. Short-term indicators have broadly reversed – that happens in most pullbacks. If the longer-term technical measures begin to signal caution, we’ll interpret that as worse than a correction ahead.

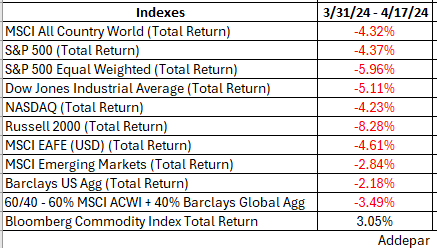

Below are the various equity indexes performance numbers since the start of April.

As is so often the case, this pullback feels worse than the numbers may reflect. Unfortunately, our pullback probably has more to go. We are in a seasonally difficult period of markets due to low liquidity that lasts until June. One reason is that investors need funds to pay taxes. Unlike last year, investors had plenty of capital gains taxes to pay this tax season.

On Monday, we’ll look at the bond market and where yields may be going. Have a good weekend.

Be well,

Mike

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was compiled from sources believed to be reliable, but Robertson Stephens does not guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Performance may be compared to several indices. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. A complete list of Robertson Stephens Investment Office recommendations over the previous 12 months is available upon request. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2024 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.