October 10, 2024 – The best adjective to describe the US economy in the first three quarters of 2024 is ‘resilient’. Despite high interest rates, extensive layoffs, the threat (and promise) of AI, global geopolitical turmoil, and internal political uncertainty, the US economy continues to grow at a steady clip. Recent estimates suggest that Gross Domestic Product (GDP) grew at 2.5-3% in Q3, following 3% growth in Q2. By any measure, this above-trend growth is impressive. There’s no need to continue searching for a soft landing—the plane has already arrived at the gate.

To be sure, the landing has not been equally smooth for all passengers. As we discussed in previous notes, there is increasing economic pressure on certain low income and middle-class consumers, evidenced by decreasing savings and rising delinquencies. It remains to be seen whether the stress will spread to the rest of the economy. So far, that doesn’t seem to be the case, a point made clear by the September job report that showed an increase in 254,000 jobs, and an unemployment rate holding steady at 4.1%. It’s no surprise, then, that Fed officials have made it clear that a 50-basis-point rate cut is not the new normal.[1]

After years of economic uncertainty from Covid to high inflation to rapidly rising interest rates, the current economic condition seems tranquil by comparison. In part this is because public discourse is focused elsewhere, namely on the upcoming election and on the events in the Middle East.

Though the US economy has shown solid performance, investors remain mindful of global risks that could affect global markets, particularly in energy. This October marks the passing of a year since the Hamas attack on Israel that ignited the current round of hostilities in the Middle East. What started as a limited conflict between Israel, Hamas, and Hezbollah, has grown into a regional conflict involving Iranian proxies in Yemen, Syria, and Iraq, as well as unprecedented direct blows between Iran and Israel. Though far from over, the conflict is already reshaping the face of the Middle East, with an emphasis on the relationships between the Shite led Iran, the moderate Suni Gulf states led by Saudi Arabia, and the West.

What’s less clear is what impact the conflict in the Middle East will have on the global economy. For the past year, oil investors seemed numb to the turmoil, reflecting the growing dominance of the non-Arab oil producers, led by the US — now the largest oil producer in the world, as well as OPEC’s diminished control over oil production. This appears to have changed in the last week, as the prospect of an Israeli attack on Iranian oil facilities rattled the markets. Iran is the world’s 7th largest oil producer, and a disruption of its oil supply, especially if coupled with Iranian attacks on the facilities of neighboring countries, would have a meaningful impact on global supplies. No doubt, the Biden administrations would like to avoid skyrocketing gas just weeks before the election and has telegraphed as much to Israel.

Ultimately, nothing in the Middle East is likely to be resolved imminently, and the upcoming US election gives both sides ample reasons to hold out and see what the next administration will look like. Though an escalation is certainly possible, the diversity of today’s oil producing countries suggests that a repeat of the 1970s energy crises is unlikely even if oil prices do come under pressure. War is unpredictable though, and if the conflict grows to include other oil producing countries like Saudi Arabia, a constricted oil supply could challenge economic growth globally.

The Markets

Equity markets had a bumpy start to the quarter, driven by concerns over the economy, an assassination attempt on Donald Trump, and the unwinding of the Yen carry trade, which sent the S&P 500 down 8.5% from recent highs.[2] However, things shifted in September when the Fed announced victory over inflation. With investors enthusiastic about the prospect of rates coming down, the S&P 500 ended the quarter up 5.5%, bringing its year-to-date gain to 20.8%.

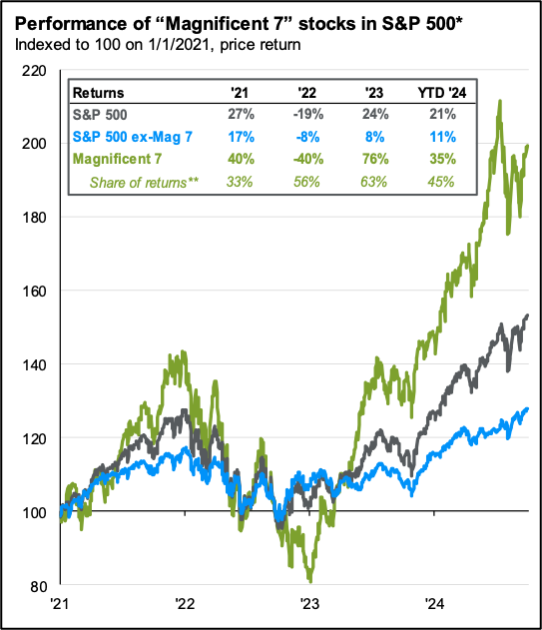

For the first time in a while, the rally in the stock market was not driven by a small group of mega-cap tech companies. Notably, the “S&P 493″—the S&P 500 excluding the Magnificent 7—posted earnings growth for the first time in five quarters. These improving financial results, coupled with decreasing rates, broadened the market rally, with small-cap, mid-cap, and rate-sensitive sectors outperforming large-cap growth.

Chart 2: Performance of “Magnificent 7” stocks in S&P 500. The “Magnificent 7” dipped in performance in Q3 while the rest of the S&P 500 saw strong growth. Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management.

*Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA. Earnings estimates for 2024 are forecasts based on consensus analyst expectations. **Share of returns represent how much each group contributed to the overall return. Numbers are always positive despite negative performance in 2022.

Globally, emerging markets returned 8.7% in Q3, aided by a one-day rally of 23.9% in Chinese markets after officials announced a series of stimulus measures designed to jump-start the local economy. It remains to be seen how effective this “Shock and Awe” campaign will be, given longstanding structural issues in the Chinese economy, including a troubled housing sector, low levels of consumer spending, and an aging population. Non-U.S. developed markets also had a strong quarter, returning 7.3%.

In the fixed income market, rates fell across the yield curve as the Fed signaled a shift in the monetary regime. The decrease was steeper on the shorter end of the curve, turning the spread between 10-year and 2-year Treasuries positive for the first time since July 2022, even as other parts of the curve remain inverted. With rates coming down, the Bloomberg Aggregate Index returned 5.2% in Q3.

The Outlook

With less than two months until the next U.S. election, the details of the candidates’ proposed policies are starting to come into focus. However, given that taxation and budgeting are controlled by Congress, not the president, and considering the tight races for the Senate and the House, a blowout win allowing either party to enact dramatic legislative changes seems unlikely. Of course, there are ways presidents can shape the economy without Congress, including trade agreements, foreign policy, tariffs, and aspects of immigration. Yet, pre-election promises often differ greatly from post-election realities.

Noticeably absent from either candidate’s agenda is a serious discussion about the U.S. budget deficit or the growing national debt. While the debt itself, currently at 120% of GDP, is not yet a pressing issue, running a deficit of over 6% while the economy is growing reflects a lack of financial discipline that is uncommon in the American system. One can only hope this topic reenters public discourse before financial markets force the issue, as they did in Britain in 2022.

With this uncertainty in mind, it’s important to highlight that, over time, the president’s party affiliation has had little impact on stock market returns. Research further suggests that attempting to time the market based on political views tends to be costly for investors. This isn’t to minimize the impact of the upcoming election, but to encourage a separation of politics from investment discipline. As always, investors should ensure their portfolios are aligned with their goals and risk tolerance so they can withstand the volatility that will inevitably accompany the election.

Wishing us all a peaceful fall, at home and abroad.

— AMD

[1] https://www.bls.gov/news.release/empsit.nr0.htm

[2] Market Data Sources: Robertson Stephens Investment Office, JP Morgan Asset Management Guide to the Markets.

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2024 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.