The following is your January 2025 Robertson Stephens Monthly Performance Report.

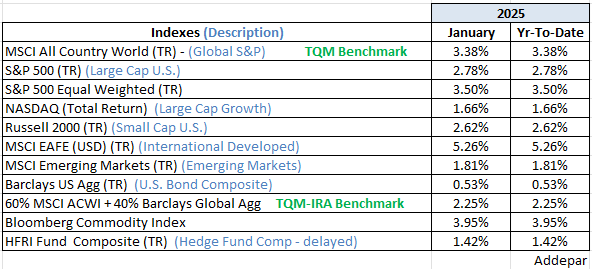

Recall the correction stocks and bonds were suffering under as the New Year began. Markets got back on track in January, with both stocks and bonds broadly delivering positive returns (see red-free chart below). It was not a smooth ride – daily volatility increased considerably in both markets.

In equities, there was a departure from U.S. Index dominance; the International Developed market was the best performer. Another departure from the status quo of the last two years was the loss of leadership by large-cap growth companies tied to AI. These two observations are closely connected by cause and effect. The emergence of Chinese AI technology company DeepSeek called into question the U.S. technology sector’s ability to deliver against lofty expectations.

In the bond market, President Trump’s proposed policy mix of tax cuts, immigration curbs, and tariffs fueled expectations of higher inflation, pushing up yields globally. New Treasury Secretary Bessent saved the month for bonds as he laid out plans for lower yields, specifically on the 10yr U.S. Treasury. Worth noting, stronger than expected CPI inflation data was released this morning (2/12), and all the yield gains from January have been erased.

Commodities were one of the top performers of the month, with the broad Bloomberg Commodity Index rising ~4.0%. Not on the chart, Gold and other metal prices rose on the back of Trump’s tariff threats, while oil prices were lifted by cold winter weather and unaffected, thus far, by promised deregulation policies.

There is little debate over the extreme valuation of the S&P 500 Index. Its valuation is stretched, relative to its 100-year price trend after adjusting for inflation, by the most in history except the market peak in 1929. The S&P 500 is in a historic bubble on a long-term basis. However, one of the most influential economists of modern times, John Maynard Keynes, said, ‘Markets can remain irrational longer than you can remain solvent”. Momentum is the strongest of all factors that influence market prices. – hence, the number one rule of investing “Don’t fight the tape” – an equivalency to don’t fight momentum.

The tape remains mostly bullish, and the Fed is probably best described as neutral – neither hiking nor cutting rates. Most market indicators are bullish except ones connected to interest rates. Rising yields while the Fed cut rates last year was the only fly in the ointment of the bullish thesis.

We know that bubbles can be lasting, and valuation is not a good timing mechanism. But as a risk manager, it makes sense that those who know something is coming are better prepared to act when it happens. Granted we need some trend (tape) deterioration to turn bearish. The market message currently is – stay invested. History says bubbles burst. These two opposing concepts leave us on high alert. We feel like we’re whistling past the graveyard since another one of the “most influential” investors of our time is currently over 30% allocated to cash, and Mr. Buffet has been clear on this point in the past; periods of bubble valuations have led to poor returns looking out one to 11 years later. We are forewarned and forearmed.

e well,

Mike

Sources: Addepar, BCA Research, Bloomberg, and Ned Davis Research

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was compiled from sources believed to be reliable, but Robertson Stephens does not guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Performance may be compared to several indices. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. A complete list of Robertson Stephens Investment Office recommendations over the previous 12 months is available upon request. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2025 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.