By Stuart Katz, Chief Investment Officer

March 5, 2025 -March Madness and market uncertainty share striking parallels in their unpredictability and high stakes. The NCAA basketball tournament, known for its “Cinderella stories” and upsets, is a single-elimination event where even top-seeded teams can fall unexpectedly. Similarly, financial markets operate under constant uncertainty, with prices influenced by incomplete information, shifting macro conditions, changing fundamental performance, and dynamic investor sentiment.

In March Madness, the odds of predicting a perfect bracket are astronomically low, underscoring the randomness of outcomes. This mirrors market dynamics, where asset pricing often deviates from expectations due to exogenous factors or limited knowledge regarding such events as the U.S. implementing the highest tariffs since WWII, how countries may retaliate, how companies may respond (increase prices and/or suffer margin compression) and finally how consumers spending and inflation expectations may change. Both arenas thrive on volatility: the tournament’s excitement comes from underdog victories, while market fluctuations create opportunities and risks for investors.

Currently, the S&P500 is trading approximately 5% below the all-time high. Mag 7 and DeepSeek are reminders that disruption is a feature not a bug of technological innovation. The Mag 7 has declined nearly 10% year to date, an important reminder to consider broadening out equity exposure, especially in a market where elevated valuation multiples provide a limited buffer for disappointing developments.

Tariffs on Mexico, Canada, and China went into effect – and the question now is how long they remain in place. Our framework to understand the current investment environment includes but is not limited to evaluating the following.

- Macro Economy. The U.S. ended 2024 with particularly strong momentum in domestic retail sales, which grew by 3.1%. Good momentum for earnings growth as well, with an encouraging recovery in margins. Early in 2025, the economy did seem to be cooling, and the underlying pace of demand seemed to be around 2%, as consumer spending downshifted from a strong fourth quarter. The two-trading day drop in the Atlanta Fed GDPNow metric from +2.3% on Thursday last week to -2.8% this Monday also caught investors by surprise. However, we believe the import surge in January and the GDPNow calculation methodology may help explain some of the decline. Additionally, the University Michigan sentiment decline may not ultimately translate to as big of an anticipated pullback in capital expenditure and consumer spending. Overseas, investors in Germany are brewing rumors that it may launch a substantial fiscal package worth EUR ~500 billion (10%+ of GDP), which removes the government’s “debt brake,” a constitutional limit that prevents Germany from delivering large fiscal deficits.

- Fundamentals. The earnings reporting season for the S&P 500 fourth quarter indicates strong performance, with growth at ~15% year-over-year. If this rate holds, it will be the highest reported growth since Q4 2021 and the sixth consecutive quarter of year-over-year earnings growth. We continue to expect U.S. equity returns in 2025 to be more modest than last year. We anticipate they will largely match the path of earnings growth in the high single-digit range, albeit with elevated volatility and intra-calendar year peak-to-trough declines consistent with historic figures of approximately 15%. After two years of strong performance in U.S. stock markets, with little volatility – the last 10% correction was in October 2023.

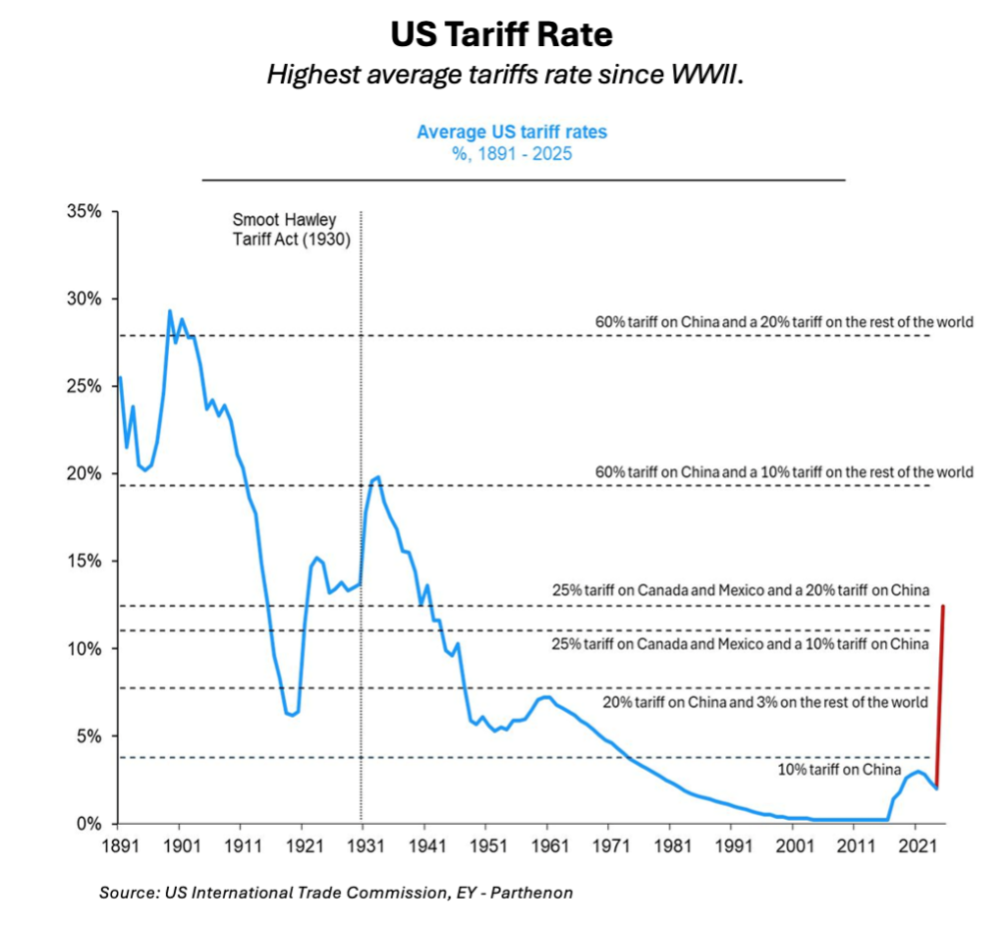

- Policy Changes. The approximate 7% point increase in the average U.S. tariff rate versus the start of the year is meaningful, especially the 25% increase in tariffs on imports from Mexico and ex-oil imports from Canada. The question is, what is the “exit strategy” to de-escalate these actions and reactions? The China, Canada, Mexico, and potentially European tariffs are mixed into a pot of substantial uncertainty around federal spending, which can affect the broader economy. Sectors in the epicenter include auto & auto parts, retail, agriculture, materials, construction, and energy, and geographies such as California, Texas, and Washington D.C. have the highest concentration of federal works. These front-loaded developments may be part of an administration strategy of short-term pain for long-term gain, where, later in 2025, tailwinds from tax cuts/extensions and deregulation may take effect. Elevated policy uncertainty creates opportunities and risks around greed and fear.

- Stagflation. We believe events that significantly reduce the supply of goods and services to an economy may lead to “stagflation,” but we are more mindful of the downside risk to the real economic growth side as businesses and consumers adopt a “wait and see” attitude and as business margins come under pressure. Confidence measures have fallen on the industry and consumer side, but this Friday’s February jobs data might help alleviate some rising growth concerns. With an economy that is led by consumer spending the health of the job market will be critical to monitor. The downward revision in GDPNow, softening ISM manufacturing new orders, and rising cost pressures underscore that growth risks are shifting as inflationary pressures persist in the 3% range.

- The Fed. The U.S. central bank has two main objectives: (1) price stability, meaning low and stable inflation, and (2) full employment, which refers to conditions that create new jobs and keep unemployment low. The central bank began cutting rates (the short end of the yield curve) in 2024 as its focus shifted from reducing inflation to supporting the labor market. However, with inflation progress stalling and the labor market holding firm (so far…), many believe the Fed will pause its rate-cutting cycle until there is more clarity on both fronts. However, the long end of the yield curve is declining and recently inverted (again), signaling concerns about economic growth. The 10-year Treasury yield declined 30bps in February. Elon Musk is reportedly using a falling 10-year yield as a sign of success for DOGE spending cuts, while Treasury Secretary Scott Bessent has stated that lower rates will boost growth. Plus, Trump has tweeted very little about the stock market (unlike Trump 1.0), tweeting instead about the debt ceiling, government spending, and other matters.

- Quality Bonds and Equity. We believe the tug-of-war between growth and inflation will continue this year. For moments like these when concerns are more about a real economic growth shock, core bonds do work as diversifiers: the U.S. investment grade aggregate index is up approximately 2.4% since the end of January (and ~4% since yields peaked in mid-January). For stocks, quality is key – across market caps and certain geographies. The bigger picture right now is that the U.S. economy is slowing and not collapsing, and we are monitoring inflation expectations to determine if they become unanchored.

- What does all this mean for the market outlook? First, for US risk assets to resume their strong performance, investors need to be confident that the soft growth patch is only temporary. Second, this is unlikely to happen in the very near term. Softer growth metrics are not uncommon during the first quarter of the year, and thus far, the signals continue to point to a softening – not a recession. What is unique this time, though, is that the cooling in growth is also accompanied by rising uncertainty around tariffs and trade, government funding and employment, immigration, and foreign policy. Third, Trump’s policies appear to be short-term, targeting aggregate demand with the hope that inflationary pressures and rates will subsequently decline. Fourth, the re-pricing of growth expectations is increasing dispersion across equities and fixed income pricing and putting pressure on fundamentals. The distressed exchange default rate for the Morningstar LSTA US Leveraged Loan Index, which includes liability management exercises (LMEs), has been rising due to a growing number of balance sheet restructurings outside of bankruptcy.

Tactical Decision-Making During Periods of Uncertainty

Basketball fans analyze team performance and matchups to predict outcomes, akin to investors evaluating economic indicators and fundamentals to make informed decisions. However, just as a lower-seeded team can defy the odds, macro developments can surprise even the most seasoned analysts.

Ultimately, March Madness and market uncertainty exemplify environments where preparation meets unpredictability. Success in both demands balance calculated risks with an acceptance of inherent variability. Adaptability is key in managing this unpredictability. Basketball teams adjust strategies mid-game to counter surprises, while investors must periodically reassess portfolios to align with changing market conditions while being tax aware. Additionally, patience is vital; while March Madness thrives on single-elimination drama, long-term investing benefits from a multi-year perspective that mitigates short-term volatility.

Disclosures

Investment Commentary Sources: Bloomberg. Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2025 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.