By Stuart Katz, Chief Investment Officer

Recap of Year-to-Date Market Performance

Stocks started 2025 trading higher but have since pulled back. The S&P 500 has declined more than -8% from its all-time high on February 19th, lowering its year-to-date return to -5% (Figure 1). The Nasdaq 100, an index of technology and growth stocks, is down -7% year-to-date, while the small-cap-focused Russell 2000 has fallen -9%. The Magnificent 7, a group that includes Microsoft, Apple, Meta, Alphabet, Amazon, Nvidia, and Tesla, has declined nearly -15%. Given the recent volatility, our team wanted to discuss the current environment and provide a market update.

What’s Behind the Market Selloff?

Several factors are contributing to the current market selloff. First, momentum stocks that led the 2024 rally are now experiencing a sharp reversal. Figure 2 shows 2024’s top performers have become 2025’s underperformers. Technology stocks, the Magnificent 7, and Large Cap Growth powered last year’s gains, fueled by enthusiasm for the artificial intelligence industry. However, the concentrated rally led to stretched valuations and crowded positioning, particularly among the biggest companies. As those stocks lose momentum, it’s triggering a rapid unwind, with a large amount of capital rotating at once. Second, investor exposure to the stock market was high entering 2025. Households’ allocation to stocks reached a record high, and institutional investors, such as pension funds, endowments, and insurance companies, increased their leverage and equity exposure last year as stocks traded higher. Now, institutional investors and hedge funds are deleveraging, adding to the selling pressure. Third, optimism around the Trump administration’s pro-growth policies has given way to concern, with worries that spending cuts and the uncertainty created by tariffs will slow economic growth.

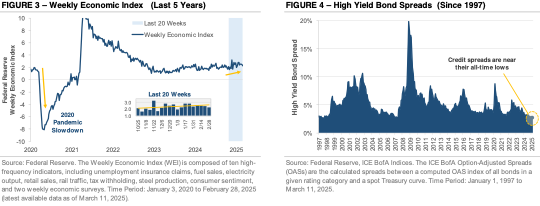

Market Volatility vs. Economic Reality

It’s important to remember that the stock market isn’t the economy, with some data points signaling a different economic reality. The Federal Reserve’s Weekly Economic Index (WEI), which tracks real-time activity using data such as unemployment claims, rail traffic, steel production, and tax withholdings, remains positive (Figure 3). Despite recent stock market volatility, the WEI suggests the broader economy hasn’t felt a significant impact. In the bond market, high-yield credit spreads, which measure the difference in yield between riskier corporate bonds and U.S. Treasuries, remain near all-time lows (Figure 4). The stability of credit spreads indicates that, so far, the selloff has been largely confined to the stock market. Together, these two data points suggest the recent volatility may be a market-specific adjustment rather than a systemic issue or sign of broader financial strain.

Is This Normal and Can the Market Selloff Continue?

Market volatility can be unsettling, but it’s a normal part of investing. Periods of enthusiasm often lead to recalibration. It’s natural to feel uncertain, but history shows that staying invested through volatility and maintaining a longer-term view is a prudent approach. Since 1928, the S&P 500 has experienced a decline of -5% or more in 91 of the past 98 years. Yet, markets have demonstrated an ability to recover and reward patience. By maintaining a diversified portfolio aligned with your long-term goals, we’re positioned to weather the market’s swings and short-term volatility.

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, any individual opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2025 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.