The International Monetary Fund cut its outlook for global growth in 2025 to 2.8%, down from an earlier forecast of 3.3%. The reduction largely was driven by the 1.8% forecast for US economic activity, a notable slowing from the 2.7% growth in 2024. It is noteworthy that 1) the IMF is not forecasting a recession for the US, 2) global growth is forecast to be 3% in 2026, slightly below the longer-term trend of 3.3%, and 3) IMF forecasts have a high margin of error.

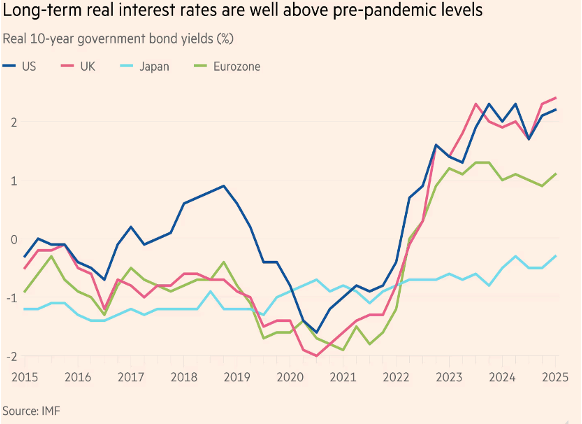

The real (inflation-adjusted) interest rate is thought to reflect the true cost of borrowing, or, alternatively, the actual return on savings. Ten-year government bond yields provide the benchmark for a host of investment decisions, ranging from business purchases of equipment to consumer purchases of real estate. As ten-year yields have increased, business fixed investment and residential investment in the US have weakened.

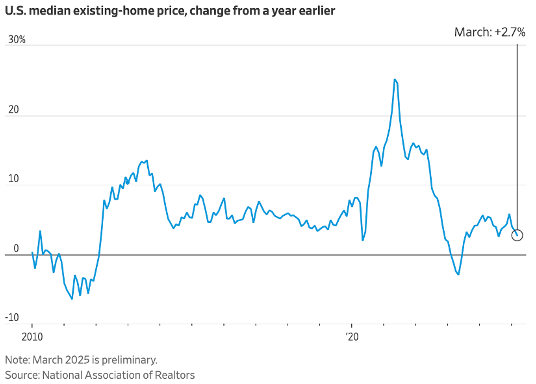

According to the National Association of Realtors, the US median home price in March was $403,700, the highest median home price on record and a 2.7% increase from the previous year. The median home price increase in the Northeast was the greatest, at 7.7%. At the same time, March existing home sales fell sharply, posting an unexpected 5.9% decline, and the inventory of unsold homes rose. At present, supply exceeds demand, and some adjustment to prices, demand, and supply is anticipated.

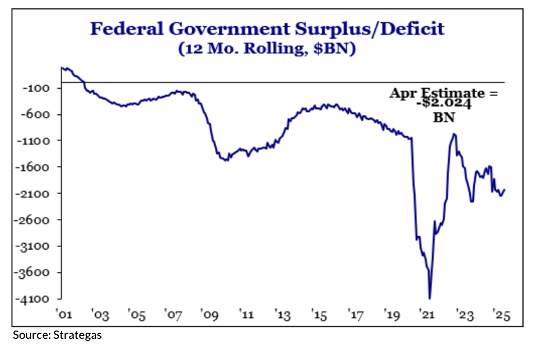

US tax revenues appear to be running slightly more than 3% above the same time period last year, largely due to strong economic growth in 2024. While the chart shows a small improvement in the Federal Government Deficit, the impact of tax revenue increases and DOGE spending cuts is, as yet, minimal.

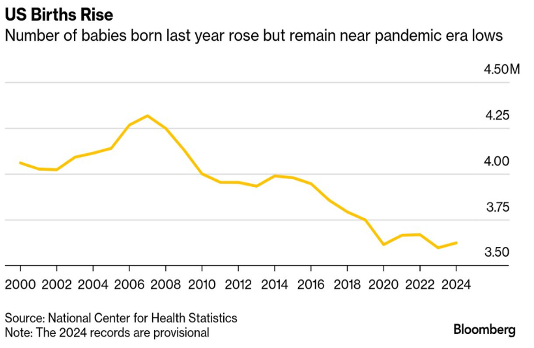

Finally, the pronatalist movement was much in the news this week. Whereas Malthus was famously concerned that population growth would eventually outstrip resources and promote economic decline, economists have long argued for a different relationship between an expanding population and economic growth, citing positive effects on consumer spending and the supply of labor. The evidence is inconclusive enough to allow for vigorous and contentious debate, complicated by different economic goals and social objectives. The 1% increase in US births in 2024 was entirely attributable to increased births in the Asian and Hispanic population of the country, and the greatest number of births was in California, the nation’s most populous state. Births declined the most in the District of Columbia, Louisiana, and Mississippi.