In July, the Trump administration’s announcement of several trade agreements, along with the passage of the One Big Beautiful Bill Act (OBBBA), added some clarity to the future policy backdrop and bolstered market risk sentiment. While the removal of uncertainty typically supports market values, it may have been investors’ willingness to overlook the potential long-term impact of the new tariffs that most buoyed prices during the month.

After July’s modest decline in uncertainty, the August 1st employment report brought us right back into the uncertainty-mire that has defined much of 2025. Dramatic downward revisions to prior months have cast fresh doubt on the health of the U.S. labor market and even raised questions about data integrity. Adding to the ambiguity is the unsettled outlook for Federal Reserve policy—and, increasingly, for Chair Powell’s own tenure.

Meanwhile, President Trump’s tariffs on more than 90 countries have now taken effect. The economic and inflationary impact—both in the U.S. and globally—remains unclear and will require more time and data to assess.

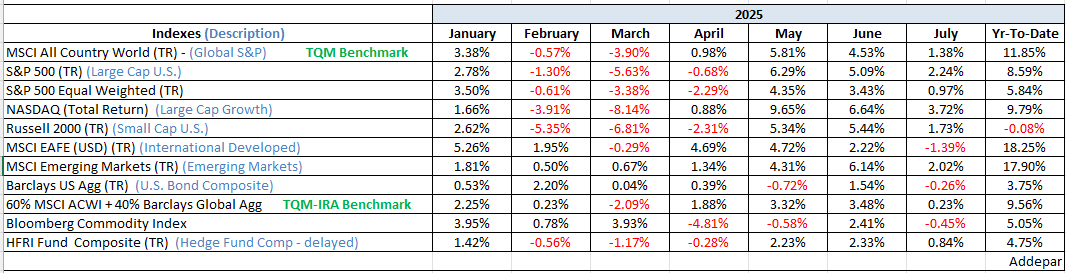

On the positive side, earnings season has offered some reassurance: with roughly 70% of companies having reported, 80% have beaten analyst estimates. Bond yields have remained range-bound, posing no immediate threat to equities. Still, markets dislike uncertainty, and there’s no shortage of it in the current macroeconomic backdrop—particularly given the volatility of policy decisions and the advanced age of this bull market.

While the fact that this bull run has lasted 1.4 times longer than the average since 1970 doesn’t guarantee an imminent end, conditions for a potential bear market are in place. Valuations are stretched, breadth has weakened, divergences are widening, and sentiment has been slipping from earlier extremes of optimism. Seasonally, we’ve also entered what have historically been the two weakest months of the year. On the plus side, both the S&P 500 and Nasdaq Composite are still notching incremental highs—a “tape” that remains the strongest argument on the bullish side of the ledger. On the bearish side, every other factor pushes the balance toward caution, leaving risk managers such as Ned Davis Research at a neutral weighting (neither over or under weight stocks and bonds).

Looking ahead, we must first navigate these historically difficult months. By then, tariff effects should begin to show up in hard data (bearish), and the Fed will likely be moving toward rate cuts (bullish). How it all plays out is uncertain, but with valuations at record levels, the potential upside from here appears far smaller than the downside risk for the remainder of the year.

Be well,

Mike

Sources: Addepar, BCA Research, Bloomberg, DoubleLine Capital, Ned Davis Research