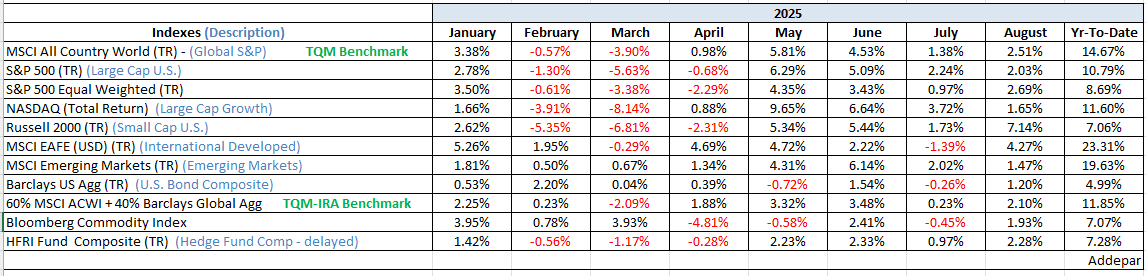

In a change of pattern, this month’s letter begins with the monthly index performance chart. As of September 14—two weeks into the month—the performance of the major indexes looks nearly identical to August, only compressed into half the time. Considering August and September are historically the weakest months of the year, the strength has been somewhat surprising.

Since April’s sharp 3-day, 15% decline in the S&P 500 following Liberation Day—and with many strategists and economists raising recession forecasts for late 2025/early 2026—I have kept a more guarded posture in portfolios, particularly in non-taxable accounts where risk can be managed without triggering tax consequences. My longstanding view remains that a non-zero probability of recession in a given year warrants measured risk reduction where it can be done tax-efficiently, given the damage recessions historically cause to portfolios.

The independent research firms I rely on—whose insights often filter into my Morning Notes—generally fall into two camps: the economists (often fixed-income oriented) and the strategists (more equity-focused). For the past 18 months, the recession warning bells have been loudest from the fixed-income side, with BCA Research as the most notable example. Meanwhile, equity-leaning firms like Ned Davis Research have remained more constructive, acknowledging elevated risks but staying bullish overall.

The divergence seems rooted in how each group evaluates the durability of AI and its impact on economic resilience. The bond-focused economists largely underestimated both the staying power of the AI trade and the surprising strength of the U.S. economy in the face of tariffs. They remain skeptical.

Equity strategists, by contrast, continue to project strength into year-end, though they see risks building in 2026. In a special webinar last week, Ned Davis Research concluded that the secular (long-term) bull market is still intact, but the risk of a major top—and the onset of a secular bear market—is rising. Cautionary signals include stretched valuations, weak market breadth, and high concentration in a handful of technology leaders.

As a result, a neutral, benchmark-weighted stance in equities remains prudent. NDR emphasized that the key threats to the bull market are a significant rise in interest rates or a stagflationary environment. Should a secular bear market unfold, the recommended pivots would be toward historically stronger segments: value stocks, small caps, emerging markets, and defensive sectors such as energy and utilities. Gold remains supported as a hedge, while a breakdown in the U.S. dollar would be a key warning sign for long-term equity weakness.

I remain guardedly bullish—with a quick finger on the eject button.

Be well,

Mike

Sources: Addepar, BCA Research, Bloomberg, Ned Davis Research.