By Avi Deutsch

October 10, 2025 – As I write this, the U.S. government remains shut down as Congress once again fails to agree on a path to keep the government funded. Government shutdowns have been a feature of American politics since the 1980s, but they have been increasing in frequency and length. The last shutdown, in 2018–2019, lasted 36 days. We’re nine days into the current one, with no clear end in sight and seemingly little appetite for compromise.

In a twist on the traditional shutdown dynamics, the administration has threatened to leverage the shutdown to bypass Congress and cut parts of the federal workforce. This unorthodox move only deepens the Democratic bind and raises the stakes for a party still seeking its political footing in the wake of the 2024 losses.

More broadly, this reflects an administration that views itself as reforming—or opposing—the parts of government it sees as inefficient or misaligned with its priorities. It is operating under the belief that the country faces a period of profound challenge, one that justifies a break with traditional norms. We are living in an era where the limits of executive power are being tested and reshaped, including by the courts, and new institutional norms are being set for years to come.

Consider the firing of Bureau of Labor Statistics Commissioner Erika McEntarfer. There’s no doubt that the data coming out of the BLS has been lacking and has made it difficult for decision-makers to assess the current state of the U.S. economy (how long can we talk about how the rent-equivalent calculations are lagging reality?). This reflects both methodological issues and resource constraints. Yet removing the commissioner sets a concerning precedent, one that risks politicizing data essential to economic decision-making.

A similar tension has emerged with the Federal Reserve. Political pressure to cut rates, attempts to remove Board of Governors member Dr. Lisa Cook (currently blocked by the courts), and the appointment of administration advisor Stephen Miran to the Fed Board while retaining a White House role all blur the line between monetary and political policy. This pressure appears to have had its intended effect: the Fed is now cutting interest rates even though the economy remains strong (if slowing) and inflation is above target. While political influence on the Fed is not new—recall the late-2010s debates on the left around Modern Monetary Theory—the Fed’s reputation for independence has taken a blow.

Importantly, today’s sense of urgency did not begin with this administration. In fact, a palpable sense of emergency may be the one common denominator of our political system. Both parties have governed under a self-imposed state of crisis, convinced that the country is on the brink of collapse and that the other party represents an existential threat to their version of America. In the middle sits a large portion of the American public, exhausted by dysfunction and distrusting of their leaders.

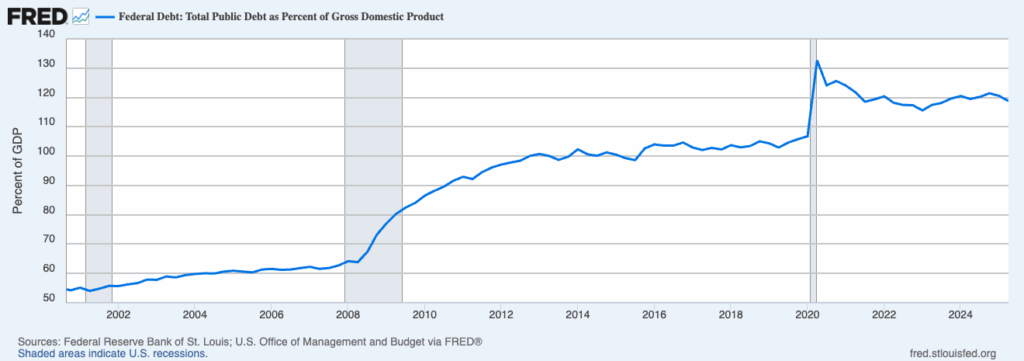

It is therefore not surprising that other structural barriers to growth have languished under successive administrations, each preoccupied with its own emergencies. Federal debt as a share of GDP has risen steadily since 2000, reaching levels that threaten to crowd out future investment and limit fiscal flexibility. Immigration reform—central to sustaining labor force growth—remains unresolved, even as shortages in human capital constrain the economy.

In the long run, these trends amount to more than political dysfunction and result in structural constraints on economic potential. Independent institutions, from statistical agencies to the central bank, are pillars of an open-market economy. When they are weakened or politicized, the quality of data, policymaking, and investor confidence all suffer. And when polarization prevents meaningful action on issues like deficits, healthcare, or infrastructure, the cost is borne in slower, less resilient economic growth.

The AI Investment Economy

The 2025 economy has been shaped by competing forces, many of them originating from government action. The current administration has eased regulation and removed barriers to consolidation while at the same time intervening directly in corporate affairs. Taxes were cut, but tariffs were imposed. Deportations have increased alongside government layoffs. Inflation remains above target even as the Fed cuts rates.

Overall, the economy continues to grow at a reasonable pace, though there are clear signs of slowing, especially in the labor market. Companies are neither hiring nor firing, and employees are hesitant to make big moves, bringing the job market to a standstill. For the first time since 2009, fewer foreign-born workers joined the labor force than native-born workers, suggesting a labor crunch could be on the horizon. At the same time, many federal layoffs are set to take effect in October, adding further drag to the economy.

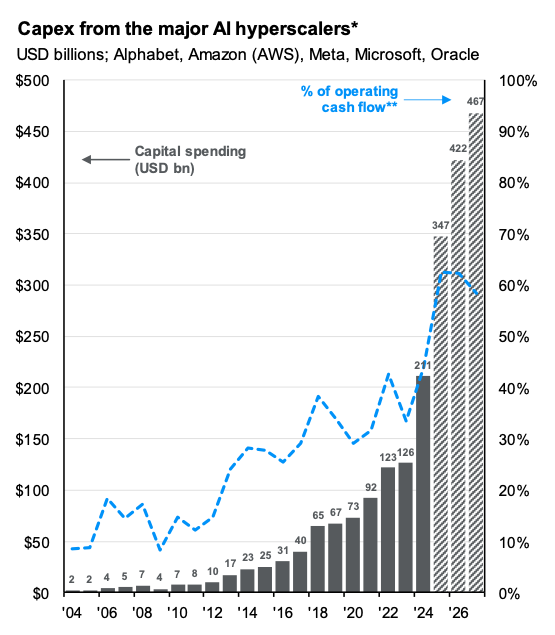

A clear bright spot remains AI investment, as cloud providers race to build the data centers that will house, operate, and cool the massive servers powering AI applications. The buildout of this infrastructure is supported by investment in AI across sectors and industries. While it’s too early to quantify the impact of AI on productivity and growth, it’s clear the U.S. economy is making a significant bet on the technology, and though the payoff may not be linear, it will almost certainly prove worthwhile over time.

Source: J.P. Morgan Asset Management; Data for 2025, 2026 and 2027 reflect consensus estimates. Capex shown is company total, except for Amazon, which reflects an estimate for AWS spend (2004 to 2012 are J.P. Morgan Asset Management estimates and 2012 to current are Bloomberg consensus estimates). *Hyperscalers are the large cloud computing companies that own and operate data centers with horizontally linked servers that, along with cooling and data storage capabilities, enable them to house and operate AI workloads. **Reflects cash flow before capital expenditures in contrast to free cash flow, which subtracts out capital expenditures. JP Morgan Guide to the Markets – U.S. Data are as of September 30, 2025.

The Unbearable Weight of Massive Optimism

Perhaps the most striking feature of today’s economic and financial landscape is the extreme optimism prevailing in the stock market. Explaining investor behavior is always speculative, but much of this enthusiasm is almost certainly tied to AI and its potential to transform business operations. Indeed, equity performance remains highly concentrated in the AI-race leaders.

With valuations on the S&P 500 nearing 23× estimated earnings, comparisons to the dot-com bubble are increasingly common. While caution is warranted, there are key differences, namely, that today’s leading companies are profitable and generating substantial cash flow.

Ultimately, there are few safe havens in markets driven by extreme optimism. Most investors are best served by adhering to time-tested principles: ensure your risk allocation matches your time horizon, cash needs, and risk appetite; diversify intentionally within your risk assets; and maintain discipline, especially when markets are running very hot or very cold.

The Outlook

The U.S. economy has few bright spots to look forward to for the rest of 2025. Many federal layoffs are taking effect in October, consumers are entering the holiday period with very low confidence in the economy, and the pass-through of tariffs from companies to consumers appears inevitable. The beginning of 2026 offers more reasons for optimism, as tax cuts take effect and households begin receiving 2025 refunds. Overall, the outlook is for an economy that continues to grow but closer to its long-term trend of roughly 2%.

Stock market performance is, of course, impossible to predict, but suffice it to say that many things must go right for current valuations to make sense, including Fed rate cuts, AI-driven productivity gains, and continued economic growth. Still, markets are inherently forward-looking, and they may ride out setbacks to this outlook—or they may not. The key, as always, is to stay invested.

Finally, the dominant force shaping the U.S. economy remains the federal government. If the mix of stimulative and restrictive policies has taught us anything, it’s that American businesses and consumers are remarkably resilient in the face of uncertainty. But for how long? Time will tell.

With high hopes for peace in the Middle East, I wish everyone a beautiful fall.

– AMD