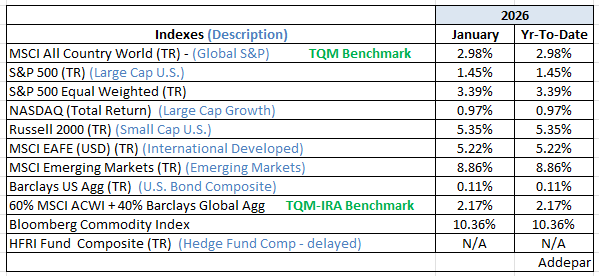

Despite heightened geopolitical tensions and increased volatility across all financial markets—stocks, bonds, commodities, and currencies—January ultimately reflected a renewed appetite for risk as investors turned the calendar page. As illustrated in the chart below, global equities continued to lead and outperform their U.S. counterparts, while U.S. equity investors further diversified away from highly concentrated AI exposure.

Fixed income was essentially flat for the month, while commodities—led by metals—were notably strong, with gold standing out in particular. Bitcoin, often viewed as the preferred risk asset of a younger investor cohort, was the exception that proved the rule: down roughly 11% in January and continuing to weaken in the opening days of February.

We entered the year guardedly constructive on equities. The bearish case rests on a mature bull market with elevated valuation measures. Offsetting this, however, is an economy that remains mixed but fundamentally constructive—continuing to grow without signs of runaway inflation. Importantly, there are still no clear market signals pointing to an imminent downturn. Market tops typically take time to form, often longer than bottoms, and while we acknowledge the possibility that we may be operating on borrowed time, we would expect clearer signals to emerge as we move closer to the second quarter.

As always, we remain focused on balancing opportunity with discipline as the market narrative evolves.

Be well,

Mike