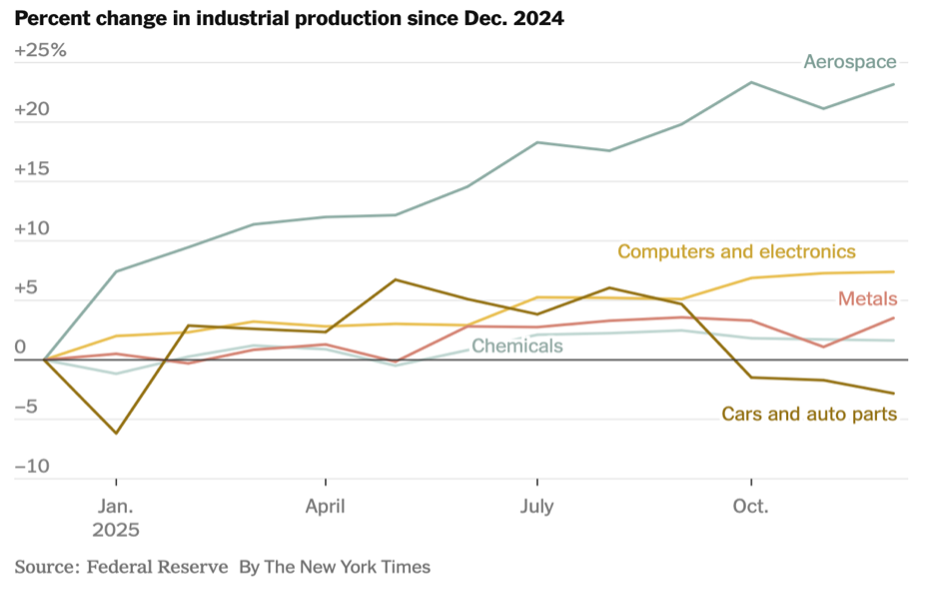

Life, as they say, is complicated. “US Manufacturing” is better understood in terms of its subsectors, some of which are doing quite well under the tariff regime installed in 2025 (and continuously modified), and others not so much. Computers and electronics have fared far better than cars and auto parts, due to a form of industrial policy favoring technology companies and the harsh impact of tariffs on “metal-bending” industries. The history of US industrial policy targeting strategically important industries dates back to Alexander Hamilton, with a more recent heyday attributable to Lester Thurow and the 1980s competitive battle with Japan. Generally, industrial policy has not been particularly successful, especially in the pursuit of long-term economic goals such as maximum employment and high levels of investment. Nevertheless, evolving global markets always seem to merit another try.

China has been an aggressive user of industrial policy as part of its adoption of a highly managed form of “capitalism.” This has contributed to a predicament for which China currently has no easy answers. Deflation has been a problem since 2023 as industrial production has been kept at a high level while domestic consumption has lagged, resulting in falling prices, which cause producers to suffer lower profits, which in turn causes them to increase production. Much of that production ends up directed to overseas markets out of necessity. Exports from China to the rest of the world have surged so greatly in 2025 that Chinese products invite tariffs or outright import controls in many important global markets. If production is forced to depend on onshore markets, deflation will worsen, and consumption may weaken further, in a textbook case of what economists and central bankers have always feared about deflation. Japan’s lost decades are attributable to similar circumstances.

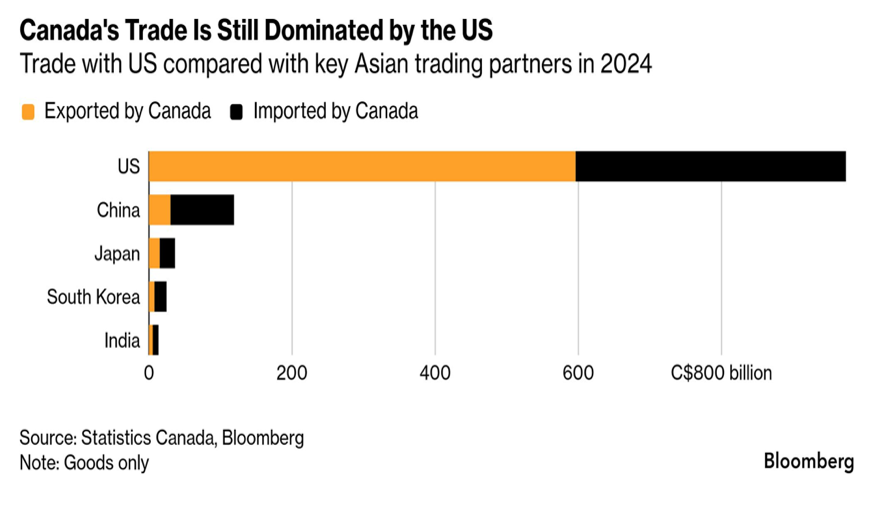

China has been assiduously seeking to bolster its relations with international trading partners, taking advantage of opportunities created by volatile and punitive US trade behaviors. Trade discussions between Canada and China have been much in the news and have created irritation for US authorities, but Canada’s market for Chinese products is relatively small – its population is approximately 1/8th that of the United States. Canada’s largest trading partner is, by far, the United States, and that is unlikely to change any time soon. Normally, industrial policy and strategic trade arrangements are ultimately aimed at boosting economic growth and employment, but it is not clear how an expanded partnership with China would play out in this regard, other than rumored joint ventures in electric car manufacturing.

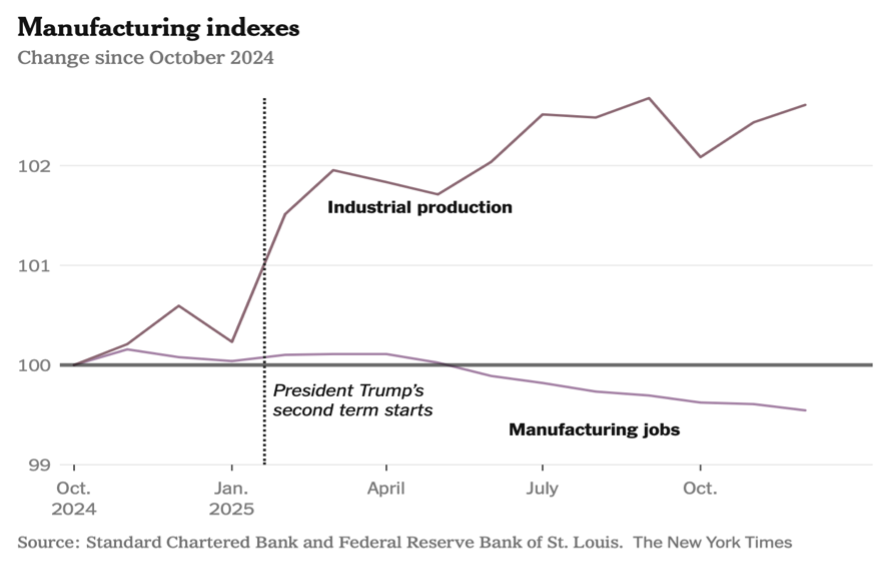

Of course, US policies intended to return manufacturing jobs to US soil haven’t exactly played out as intended, at least in the short term. The industries being most heavily impacted (negatively) by protectionist tariffs are the industries that tend to create the most manufacturing jobs. And the parts of US manufacturing that have benefited from barriers to foreign competition – integrated steel companies and domestic steel mills, for example – simply do not have production processes with the same labor intensity as existed three decades ago. It may be that industrial policy needs to be redefined from a 1960s-era concept of bolstering domestic employment to more relevant tactical and strategic objectives associated with global competition and national security.

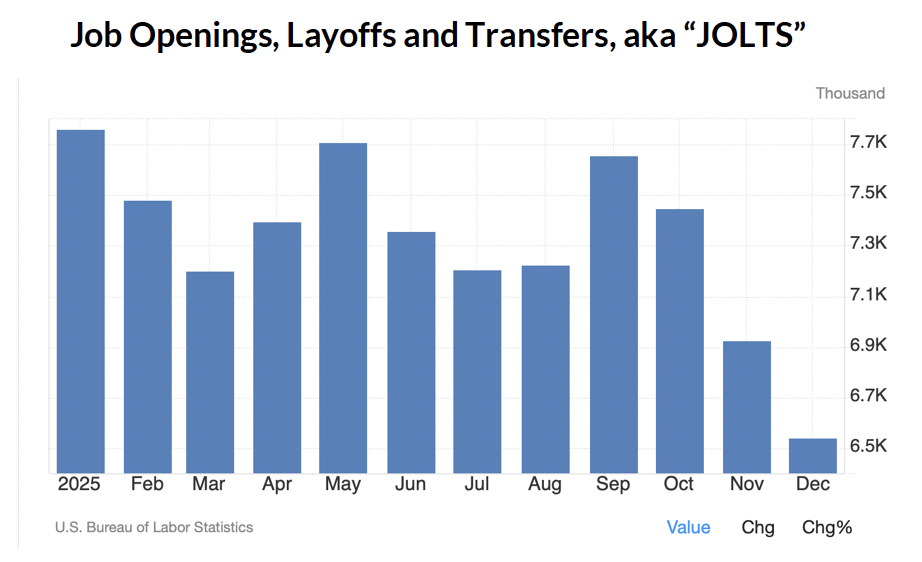

Despite strong economic growth and what some would deem to be an overall protectionist policy, job openings continue to decline in the United States. The December drop reported on February 5 was unexpectedly sharp, but foreshadowed by the ADP employment report on February 4, which indicated scant job creation of 22,000 net new jobs in January. Details from the ADP report were revealing: while truly small businesses (1-19 employees) and medium-sized businesses (50-500 employees) added jobs, large businesses cut their payrolls. Manufacturing and professional/business services (often closely tied to manufacturing trends) notably cut approximately 70,000 jobs. Yet annual pay growth for those who survived the cuts remained a comfortable 4.5% on average. As recently commented upon by the head of the Bank of Canada Tiff Macklem, these are strange times with easily misdiagnosed economic signals.