February 20, 2026 – After almost a year of AI euphoria, the stock market recently plunged into AI blues. Once seen as a great boost to all things technology, overnight AI turned into an imminent threat to software companies whose products are now seen as ripe for disruption.

While fears around the fate of software companies are probably overblown—these companies do more than just write code, and their mission critical functions, complex integrations, ongoing maintenance, and security features won’t be easily replaced by vibe coding—the fear itself signals the extent to which we are all struggling to imagine how AI is going to change our economy. These fears are everywhere, casting a long shadow that reinforces a broader sense of an unsettled society.

In this period of great technological innovation, history provides a useful guide for how the story could unfold. Sure, AI is a different, more powerful, and possibly faster evolving technological change than we’ve seen before, but it is still wielded by humans (for now?) who will seek to benefit from it. This will drive familiar behaviors of greed, fear, loss aversion, and adaptation, and ultimately will settle into a new normal with new winners and losers. Just like sewing machines, steam engines, the internet, or smartphones.

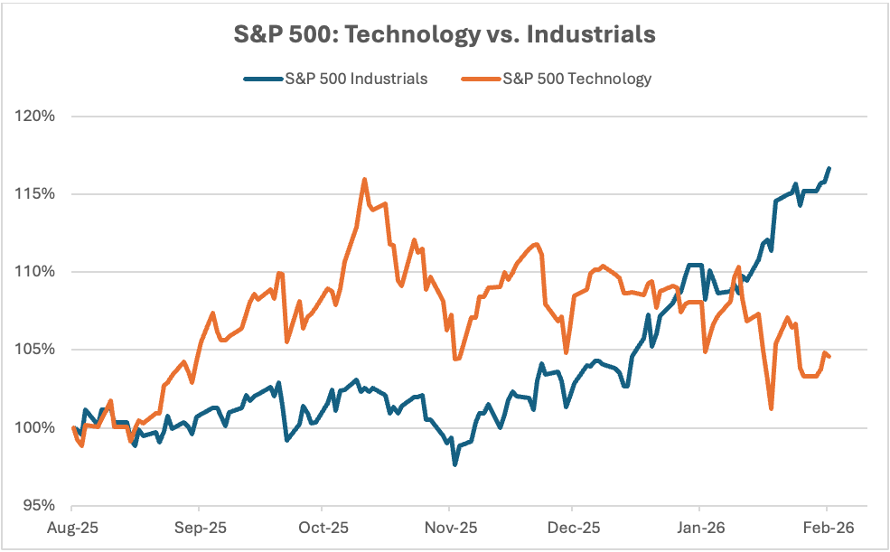

One possible outcome of the emergence of AI is a shift of financial and human capital, effort, and energy away from software and back into the world of hardware and industry. For decades, investment in software has soaked up our money, time, and the best minds of our generation. If AI reduces the marginal cost of software creation, capital and talent may increasingly flow toward physical industries, infrastructure, and applied science.

Only time will tell what opportunities AI will open to us, and how the victims of this change—those trained for jobs that may disappear—will fare. In the meantime, don’t expect software companies to be the last “victim” of AI cyclicality. Hardly. The speed of the turn against them is a testament to the herd mentality—the animal spirits—that govern the stock market. These are the same investors who pushed these stocks to new heights, supported by expectations of AI-driven productivity gains. That narrative is as true today as it was in December, perhaps even more so. What’s changed is how investors are choosing to interpret the story-driven productivity gains. That narrative is as true today as it was in December, perhaps even more so. What’s changed is how investors are choosing to interpret the story.‑driven productivity gains. That narrative is as true today as it was in December, perhaps even more so. What’s changed is how investors are choosing to interpret the story.

Please don’t hesitate to reach out with any questions or concerns.

Schedule a time to speak with me.

— AMD