February largely continued the trends that began in January, although the month included its share of crosscurrents. Among them were the U.S. Supreme Court ruling against the use of the International Economic Emergency Powers Act to justify the April 2025 reciprocal tariffs, as well as rising tensions between the United States and Iran. The latter has now become March’s challenge, with hostilities beginning only hours after markets closed for February.

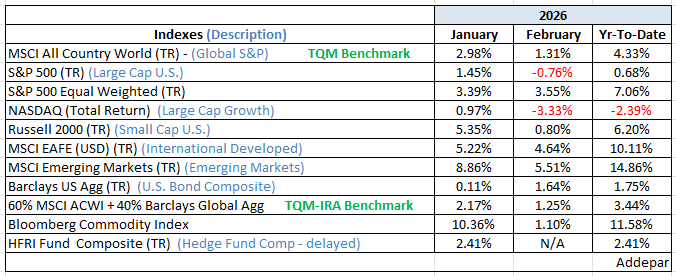

As in January, the primary driver of market returns during the month was the ongoing rotation away from large-cap growth—particularly certain software and AI-related companies—into a broader segment of the market not currently engaged in hyper-scaling or announcing ever-larger capital expenditure plans. International markets also continued their strong run, with emerging markets leading and outperforming their U.S. counterparts.

Global economic activity remained generally healthy during the month. Treasury yields declined as markets began to anticipate the possibility of a more dovish Federal Reserve Chair when the transition occurs in May. Against that backdrop, fixed income delivered a strong return of +1.64% for February, providing welcome diversification benefits.

Perhaps most important from a portfolio-management perspective, the broader set of market signals we monitor remained constructive throughout the month. That held true despite the various cross-currents, profit-taking in large-cap growth stocks, and periodic concerns about the pace and sustainability of AI-driven investment.

Events have moved quickly since the month-end. As I write this on Friday morning, March 6th, we are on Day 6 of the conflict with Iran, an event that has already pushed February’s market narrative well into the rearview mirror. If a resolution were to emerge in the coming days, markets would likely resume the trajectory that had been forming since the beginning of the year. Should the conflict persist deeper into the month, however, the outlook for asset returns could become more uncertain.

As always, our approach is to follow the market’s message rather than predict it. For the moment, despite the geopolitical uncertainty, that message continues to lean cautiously favorable for risk assets.

Be well,

Mike