Despite ongoing headlines about Middle East tensions and potential disruptions, the global oil market enters 2026 with a fundamental backdrop of supply exceeding demand. Crude inventories remain adequate, and analysts still see surplus capacity relative to underlying consumption. In other words, there is no structural shortage of oil barrels — the market is fundamentally oversupplied.

Prior to this recent Middle East conflict, the LNG market was moving from a supply-constrained environment to one with substantial surplus, likely making 2026 a transitional year toward lower prices and higher market liquidity. The increased supply is anticipated to be driven by new liquefaction projects, particularly in the U.S. and Qatar. However, project delays in the U.S. and potential data center demand, combined with Qatar production uncertainty due to the conflict, could partially delay the speed of excess supply in the short term.

But what is driving price volatility — and recent price strength — is geopolitical risk and not fundamentals.

A portion of the price per barrel today reflects the market pricing in the risk of disruption, which is normal: historically, geopolitical risk premiums can typically add about 5–10% to the fundamental oil price during periods of tension, absent specific sustained geopolitical negative catalysts. However, European LNG prices have spiked 30%+ upon the headlines that supply from Qatar may be less reliable, given the already tight global LNG market.

Where Oil and LNG Natural Gas Supply Really Stands

Before recent conflict escalations, major producers — including Saudi Arabia and other members of OPEC+ — were able to meet global demand comfortably. Saudi Arabia signaled intentions to increase production earlier this year.

Even with some cuts, the global oil system has surplus production capacity on paper, meaning enough barrels exist to meet global demand. However, markets are increasingly focused on where those barrels can physically flow, not just that they exist.

The European bloc sources 60 percent of its liquefied natural gas from the U.S., followed by Algeria and Russia. Gulf-based producer Qatar, the world’s second biggest LNG exporter, only supplied around 6 percent of Europe’s LNG in the third quarter of 2025.

But that is likely to change. The EU is already in the process of weaning itself off Russian oil and gas and is increasingly concerned that its growing dependence on the United States for LNG as EU-U.S. relations are strained.

The Strait of Hormuz and Energy Infrastructure: Why It Matters

We believe the single greatest driver of oil market risk right now is the Strait of Hormuz, a narrow maritime passage between Iran and Oman that serves as the linchpin of global oil logistics. Roughly 20% of the world’s oil and liquefied natural gas shipments transit this chokepoint daily. If traffic through Hormuz were materially disrupted, it would immediately affect crude and LNG flows headed to Asia, Europe, and beyond.

Iran itself accounts for a significant share of crude exports, and virtually all of that oil moves through Hormuz. Recent data shows that China has been the dominant buyer of Iranian crude, purchasing more than 80% of Iran’s exported oil — a sizable flow that buyers prefer because it often comes at a discount due to U.S. sanctions.

A complete closure of the Strait remains unlikely given the high economic cost — especially to major importers like China — but even a partial or de facto disruption (for example, due to insurers refusing coverage) drives prices higher because alternative routes and pipeline capacity cannot fully handle the volume.

We could see further upside and sustained oil and LNG gas prices if access through the Strait and LNG gas infrastructure production deteriorates.

China’s Exposure

China remains the world’s largest crude importer and is uniquely exposed to disruptions in Middle Eastern flows because a significant share of its oil — especially Iranian crude — arrives via Hormuz. Disruptions reverberate through Chinese refineries and inventories. Broadly, there is a narrowing of supply options for China — whether from Iran, Venezuela, Russia, or elsewhere — adding a layer of fragility to the Chinese economy. This complicates President Trump’s scheduled visit to China from March 31 to April 2, 2026, for a summit with President Xi Jinping.

What Investors Should Watch Next

Inflationary Pressures

Oil and gas prices are one of the most direct inputs into headline inflation. Before recent tensions, U.S. inflation was running near 3%. A sustained period of higher crude prices would likely push that number higher in the short term as energy costs filter through goods and services.

Federal Reserve Policy

The Federal Reserve’s rate outlook — particularly whether it sees room to cut rates — is sensitive to inflation and job market data. Higher oil prices that leak into broader inflation data could delay anticipated rate cuts or reduce the number of cuts the market expects this year. Higher crude near $80/bbl places more upward pressure on inflation than prices near $60/bbl, making a dovish pivot less likely or at least delayed.

Financial Market Behavior

In recent trading, markets have shown classic “risk-off” behavior: strong demand for the U.S. dollar and safe-haven assets like Treasuries and gold, and a flatter yield curve as traders reassess rate expectations.

February was a strong month for bonds, as the 10-year Treasury yield fell nearly 30bps to end the month below 4.00%, the lowest since October 2025. The decline in Treasury yields drove the bond market rally, with longer-maturity and higher-quality bonds outperforming as investors sought stability amid tech sector volatility, trade policy uncertainty tied to the Supreme Court’s tariff ruling, and rising geopolitical tensions.

Portfolio and Headline Risk

It’s understandable — even rational — for investors to feel uneasy when geopolitical news dominates financial headlines. However, not all risk warrants the same response:

Risks that merit attention:

- Energy or commodity supply disruptions that materially affect prices.

- Major trade route interruptions or logistical bottlenecks.

- Permanent Fiscal, Monetary, and Regulatory Policy shocks that change sector fundamentals.

Risks that are more noise than signal:

- General political tension without a clear economic mechanism.

- “Fear-driven” headlines that lack substantive impact on cash flows or earnings.

- Short-term market reactions are detached from underlying fundamentals.

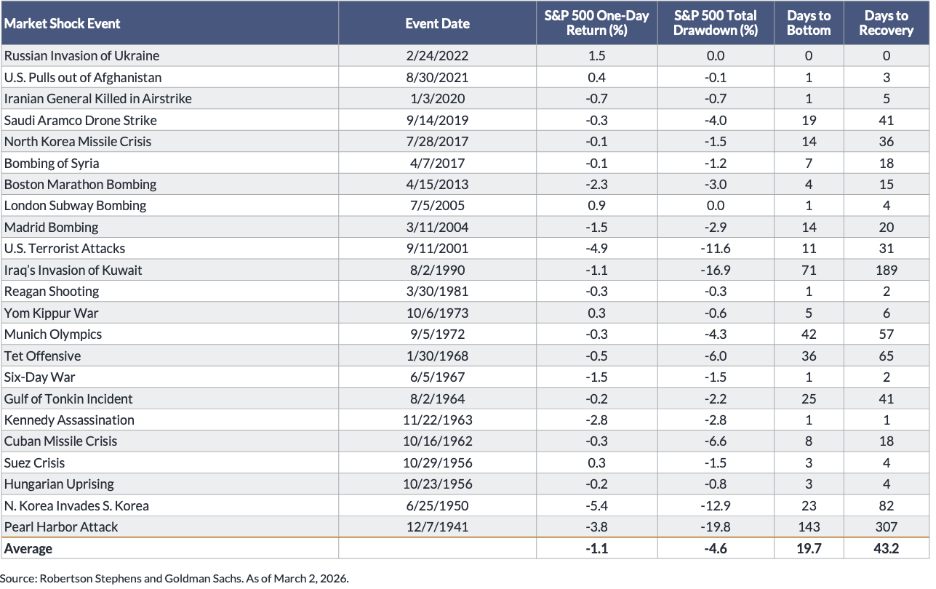

The key for long-term investors is discipline. While geopolitical events can cause volatility — and sometimes sizeable moves in oil and equity markets — history shows that markets adjust and absorb shocks over time. Patient investors with clear goals and adequate liquidity tend to be rewarded for staying focused on business fundamentals and their financial plan, including liquidity requirements, rather than letting headlines drive emotional decisions.