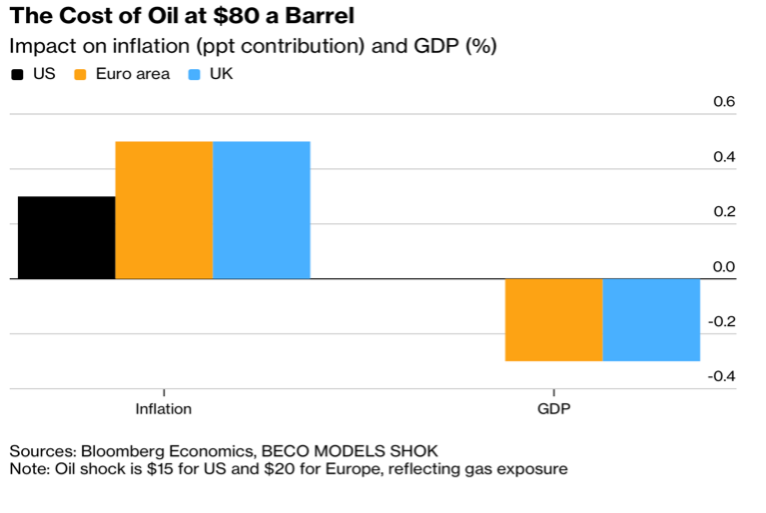

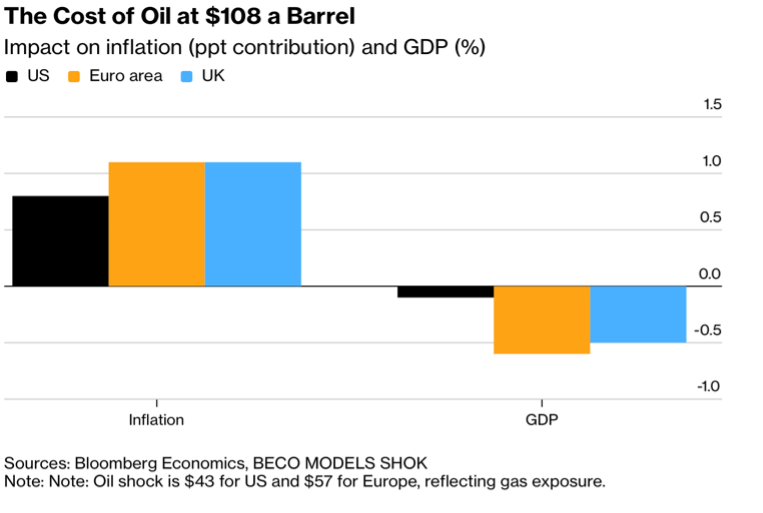

In times of extreme uncertainty, sometimes the best that one can do is to put some guardrails around one’s fears. Bloomberg has attempted to do just that by looking at the effect on inflation and growth in the US and the European theater of a sustained higher oil price. It is important to emphasize “sustained”; the greatest uncertainty at this moment is the length of time for which Middle East oil and gas deliveries will be curtailed by the Iranian War. One reason that US shale oil producers have declined to commit to increasing production is the lack of clarity on how long elevated oil prices might persist; economic effects differ considerably as things move from temporary to quasi-permanent. Nevertheless, Bloomberg’s analysis of both price scenarios supports the current view that the impact on US inflation and growth is less than one might expect, and decidedly less than in Europe.

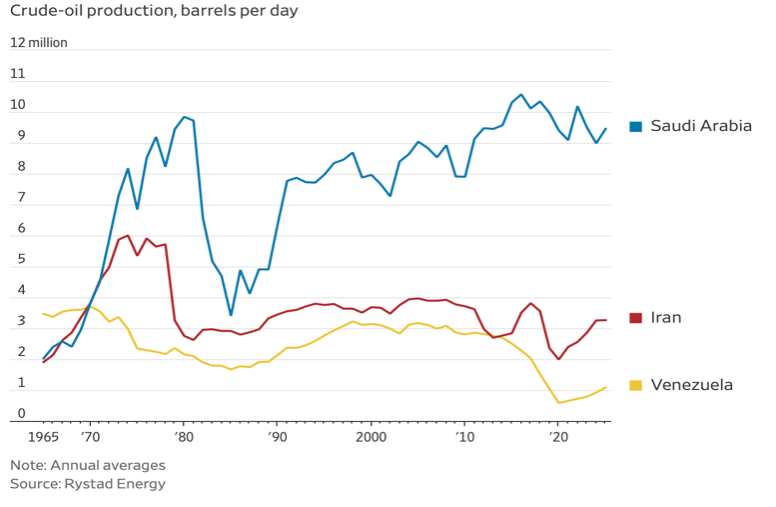

Historically, Saudi Arabia has been the notable “safety valve” for oil market interruptions from volatile producers like Iran and Venezuela. Saudi Arabia’s large Ras Tanura field has been targeted by Iranian drones and missiles, but little damage has been reported. The biggest problem is that the Saudi’s are also heavily dependent upon getting crude out to the world via the Straits of Hormuz. If the US moves forward on plans to provide US Navy protection and US government insurance to oil moving through the Straits, Saudi Arabia may be the biggest beneficiary of this largesse. In the meantime, there is a quiet effort underway to get crude out via the East-West Pipeline and Red Sea ports. The East-West Pipeline can handle approximately 5 million barrels per day (mmbd), and another 2 million mmbd can go through other pipelines intended for natural gas. Cutting natural gas shipments, however, makes some problems much worse (see below.)

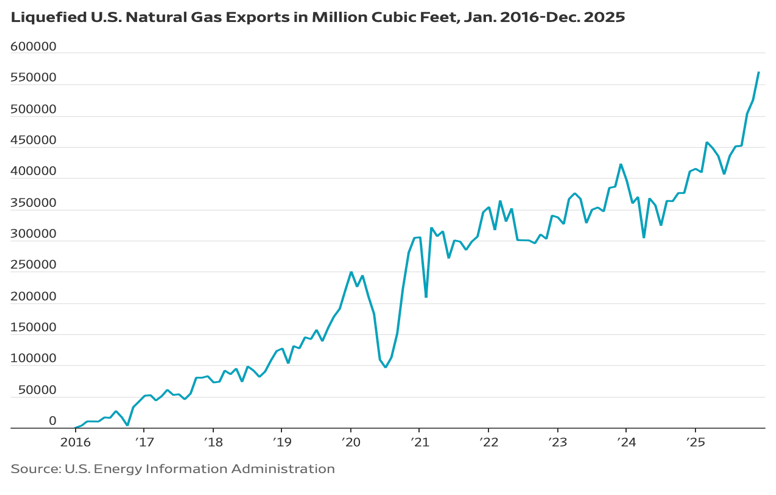

A focus on oil is only one part of the picture in terms of energy and the economic impact of the war. For example, European natural gas prices have surged in excess of 50% as Qatar first curtailed and then shut down its natural gas liquefaction (LNG) facilities. Qatar supplies 20% of global LNG and is a major supplier to Europe, though China, India, Japan, and South Korea are thought to be its largest markets. The largest LNG producer is the United States, and, over time, its exports of LNG have increased, sometimes controversially because of fears that LNG exports will raise domestic natural gas prices. Yet, the ability of the US to fill the supply shortfall created by Qatar is limited. At this point, if Qatar has truly completely closed down the Ras Laffan LNG export facility and associated liquefaction operations – the world’s largest—it will take two weeks to restart the operations.

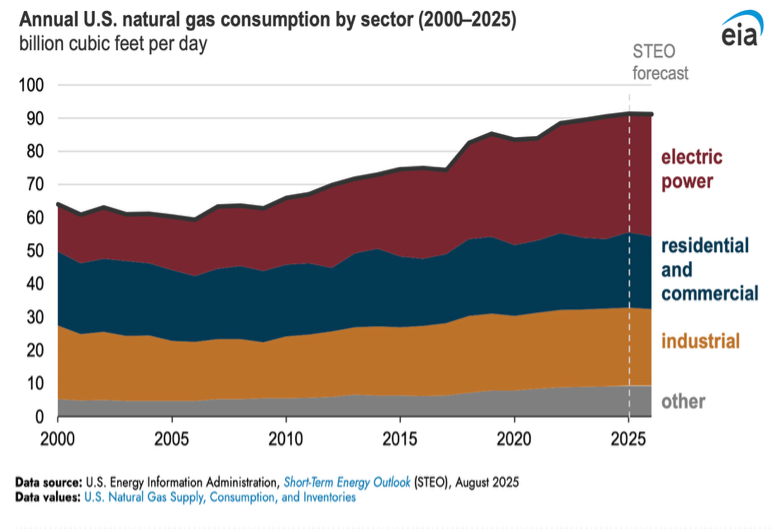

US natural gas usage by industry is fairly typical of other developed global markets, with the caveat that countries without domestic oil or coal resources are even more dependent on natural gas for electric power and residential/commercial heating. Industrial uses of natural gas are primarily in chemicals, plastics, and fertilizer production. Natural gas prices in the United States rose 81% in January 2026 due to a seasonal increase in residential/commercial demand attributable to cold weather, volatility that is not unusual in the marketplace. Upward pressure on US prices due to world events may be mitigated by declining demand as the weather warms, but it is quite possible that the price level will remain higher than in past years, adding to the monthly budget pain already facing a number of US households.

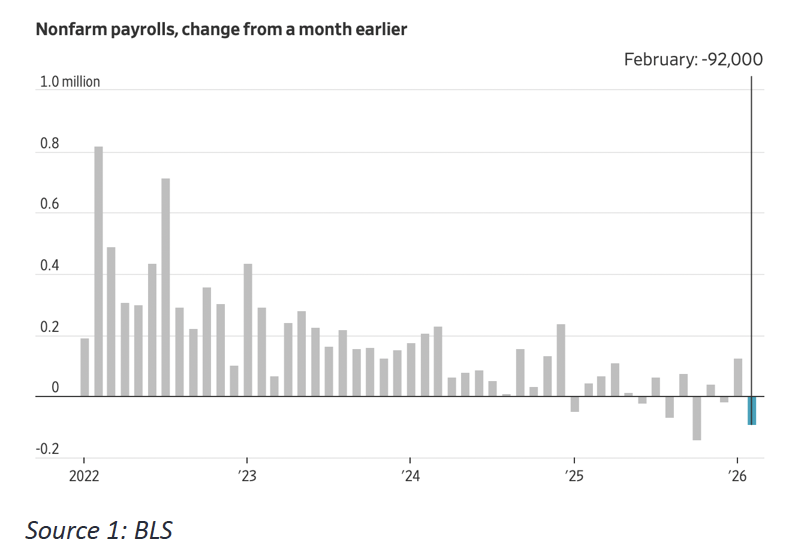

A net loss of 92,000 jobs in February doesn’t help the budget—federal government or individual household—worries either. The decline announced on Friday was unexpectedly large, driven by employment weakness across many sectors. However, the Bureau of Labor Statistics report was part of three days of mixed messages on employment: a downward revision in the ADP January employment numbers, a sharp reduction in job cuts in February according to the Challenger job cuts report, and an upbeat message on small business employment from the National Federation of Independent Business (NFIB). The next meeting of the Federal Reserve Open Market Committee (FOMC), on March 17-18, is suddenly looking very interesting . . .