March 10, 2026 – As the war between the U.S., Israel, and Iran enters its second week, the hope for a short, Venezuela-style campaign is fading. Iran’s reported choice of Mojtaba Khamenei, the son of Ali Khamenei, as its next supreme leader suggests that a mood of defiance persists in Tehran. With no popular uprising in sight, the limitations of an air-only campaign are once again becoming clear. Iran is certainly significantly weakened, and is likely to remain so for some time, but it is not out of the game.

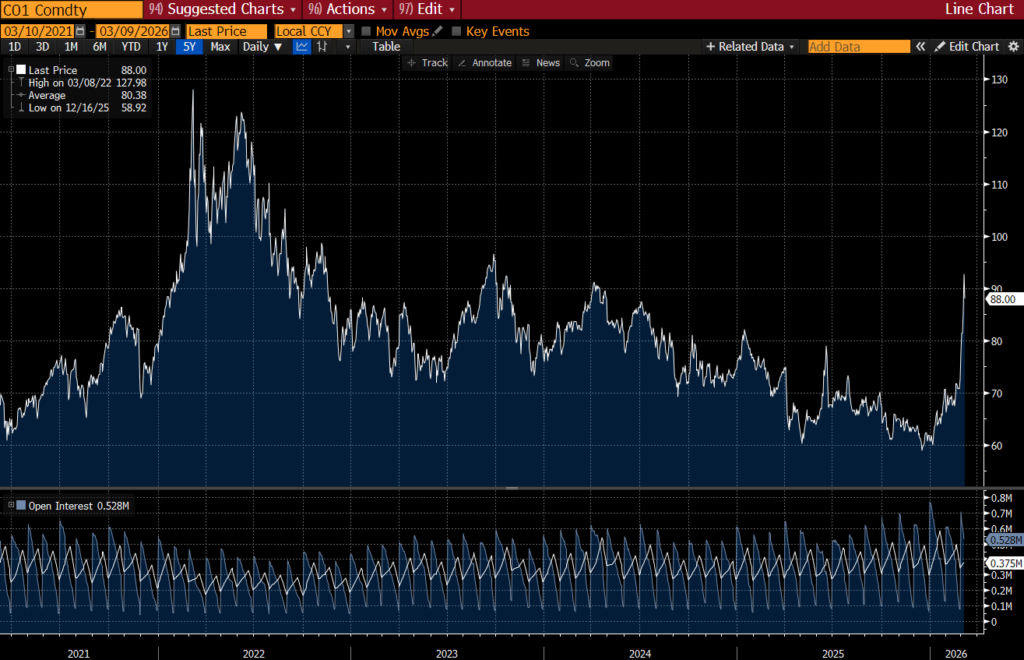

Lacking the military means to resist sustained air attacks, the Iranian regime appears focused on increasing the political and economic cost to the U.S. and its allies. Iran has fired more missiles and drones into Gulf states than into Israel, hoping that these U.S. allies—and key sources of foreign investment—will apply pressure on Washington. In addition, Iran has effectively closed the Strait of Hormuz, the critical waterway linking the Persian Gulf with the Indian Ocean, through which roughly 20 percent of the world’s oil flows. The result has been a double-digit increase in gasoline prices and a sharp rise in oil prices, now exceeding $100 per barrel.

Much now depends on how long the war continues, or at least how long Iran can keep the Strait of Hormuz closed, a reality that the U.S. and others will fight hard to overturn. The global energy backdrop entering this conflict was one of excess supply, with oil production outpacing demand. Further, many countries—including the U.S., Japan, and Germany—hold substantial strategic petroleum reserves that could be released to ease supply constraints. There is no shortage of oil yet. However, the longer the conflict continues, and the more damage Iran inflicts on the energy infrastructure of its neighbors, the greater the risk that perceptions of shortage turn into real shortages. Research from Goldman Sachs suggests that a one-month closure of the Strait could increase oil prices by approximately $15 per barrel if no strategic reserves are released.

While global oil markets remain highly interdependent, the U.S. is far less dependent on Middle Eastern oil than in past conflicts such as the 1973 Yom Kippur War or the 1991 Gulf War. The U.S. is now the world’s largest oil producer and a net exporter of oil. This means that while consumers will feel pain at the pump and in other energy-intensive services, domestic oil producers will see rising revenues. The oil price spike of 2022, following Russia’s invasion of Ukraine, may offer a useful comparison. Research from the Federal Reserve suggests that the rise in oil prices from $80 to $125 per barrel during the first two quarters of 2022 increased core inflation by just 0.17 percentage points and reduced economic growth by 0.13 percentage points. Still, higher oil prices did contribute roughly a one percent increase to headline inflation in the first quarter of 2022, inflicting real pain on consumers.

The U.S. economy entered this conflict with mixed conditions. On the positive side, real economic growth exceeded two percent in both 2024 and 2025, driven by consumer spending, investment in artificial intelligence, and, increasingly, productivity gains. On the other hand, the labor market has shown growing signs of weakness, though certainly not collapse. Complicating matters further is sticky inflation, with prices rising 2.6 percent in 2025. This elevated inflation has limited the Federal Reserve’s ability to lower interest rates, and any sustained increase in oil prices only adds to the central bank’s dilemma. This is perhaps the biggest current economic risk associated with the conflict—higher oil prices reduce the Fed’s ability to stimulate the economy while balancing price stability.

Against this backdrop, Friday’s jobs report showing job losses of 92,000 in February sent jitters through financial markets. While the number was a negative surprise, it should be viewed in context. Employment data have been subject to increasing revisions, and severe weather disrupted much of the country in February. When averaged with January’s stronger report, which showed 130,000 jobs added, the data remain consistent with a weak but stable labor market.

An exogenous shock to oil prices can have minimal economic impact if it lasts only a few weeks, or far more serious consequences if disruptions spread and generate knock-on effects across financial markets, global energy markets, or the broader conflict itself. At present, uncertainty and fear are driving market behavior—an understandable response to a violent conflict with an unknown end. Still, regardless of what this cycle brings, certain wealth management principles continue to hold: Investors with intentional asset allocations should avoid selling in down markets. Volatility often creates opportunity. And over the long term, countries, companies, individuals, and investors adapt to changing circumstances.

Please do not hesitate to reach out if we can be of assistance.

With continued hope for the safety of our troops and a more peaceful future,

— AMD