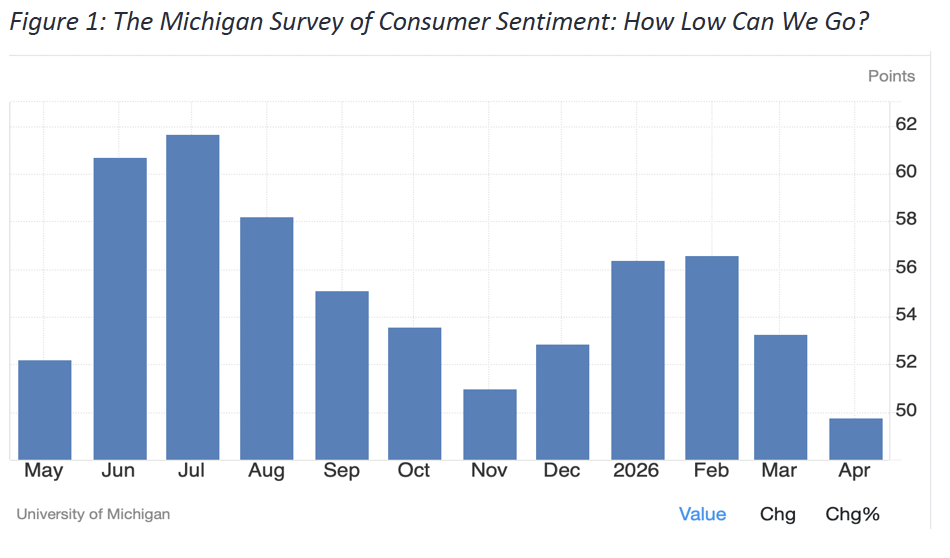

The final Michigan Consumer Sentiment number for April improved a bit over preliminary readings earlier in the month, reflecting the ceasefire in the war with Iran. Survey takers specifically cited the influence of the war and trends that were widely similar across demographic and political categories. The most eye-popping part of the report was the increase in one-year-ahead inflation expectations, which rose from 3.8% to 4.7%.

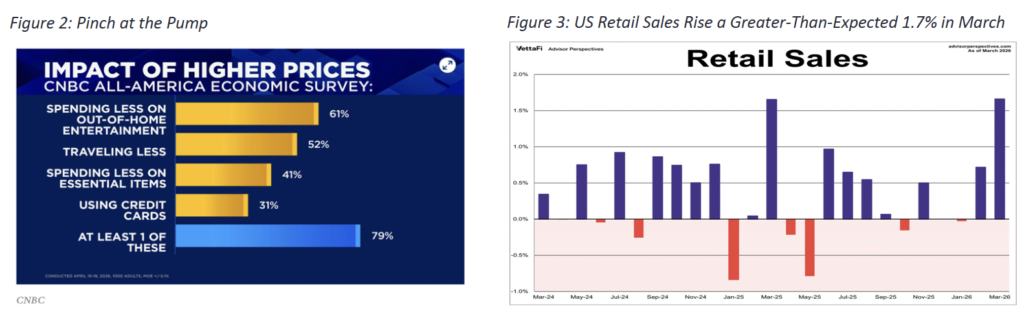

The Michigan Survey of Consumer Confidence is by no means the only survey out there. The CNBC All-America Economic Survey is a less prominent quarterly survey started in 2006, which, unlike the Michigan Survey, asks a variety of questions on topical issues. No subject is more topical at the moment than consumer spending and its ability to keep the US out of an economic recession. Spending less on various consumer products and services due to higher gas prices (see chart) does not necessarily mean spending less overall. Indeed, for the near term, higher gas prices will probably cause consumer spending to rise. US Retail Sales for March 2026 rose 1.7%, the biggest increase in over a year, driven higher by a 15.5% in retail gasoline sales.

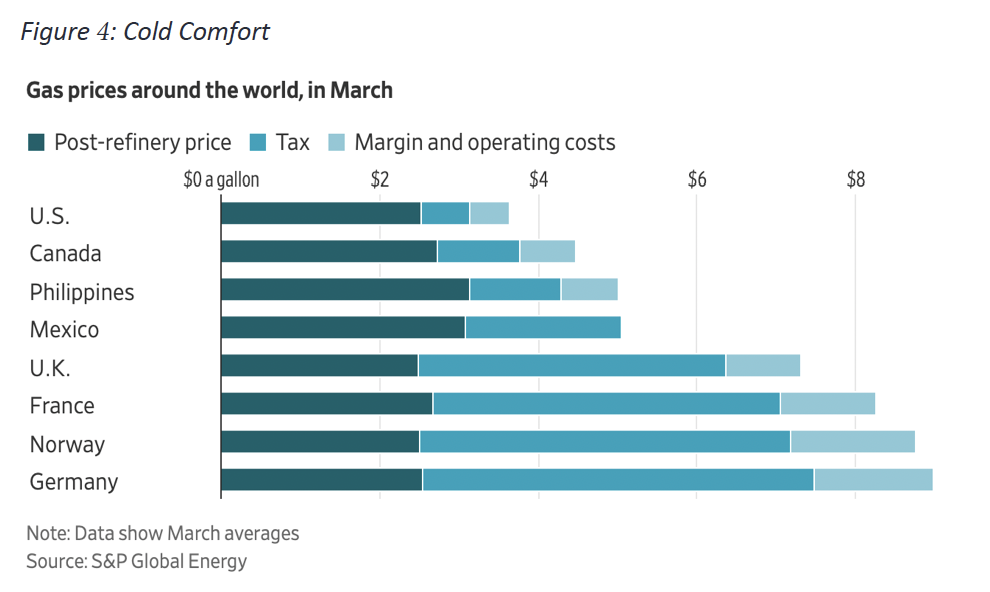

Retail gasoline prices in the United States are among the lowest in the developed world. Most other countries impose higher per gallon taxes in order to finance government budgets and a variety of expenditures; in Europe, gasoline taxes also have been explicitly used to encourage a shift away from carbon fuels. In contrast, the US uses gasoline taxes to pay for highways and other transportation-related projects, an approach that closely resembles a user tax. (California is an exception and of late has imposed gasoline taxes in a manner that more closely resembles Europe.) Perhaps the biggest surprise to many people, however, is the data suggesting that operating costs and profit margins are considerably lower in the US. Note that in Mexico, gasoline stations are privately owned but sell gasoline from the government-owned entity, Pemex.

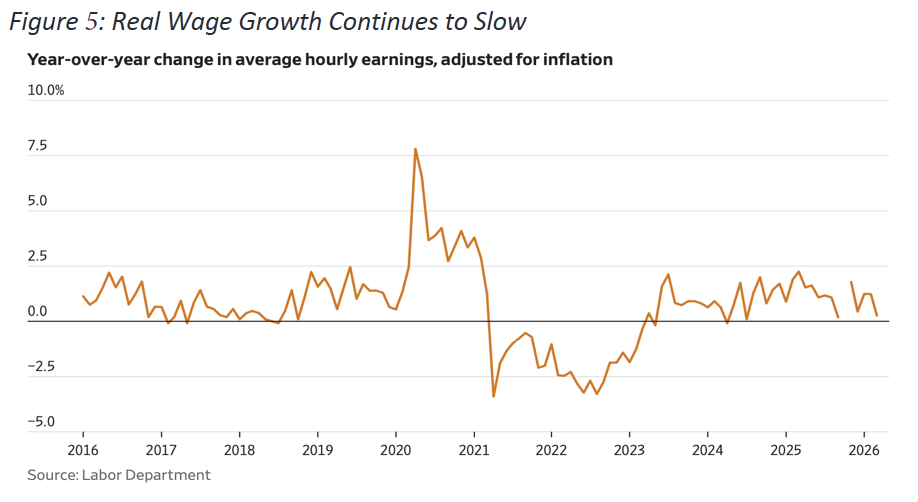

The ability of households to keep up in the face of broad inflationary pressures has been eroding for several months. This is more than just a story of rising gasoline prices. Although the unemployment rate has held steady and remains quite low, and immigration has fallen to virtually zero, an increase in average hourly earnings that might be expected in a tight labor market has not materialized. Detailed analyses of industries and job categories that were expected to be squeezed by higher labor costs as the availability of labor fell have consistently failed to detect any notable change in wage growth. Thus, as inflation has steadily moved towards 3% — measuring above 3% in March— the net effect is a reduction in the growth of spending power.