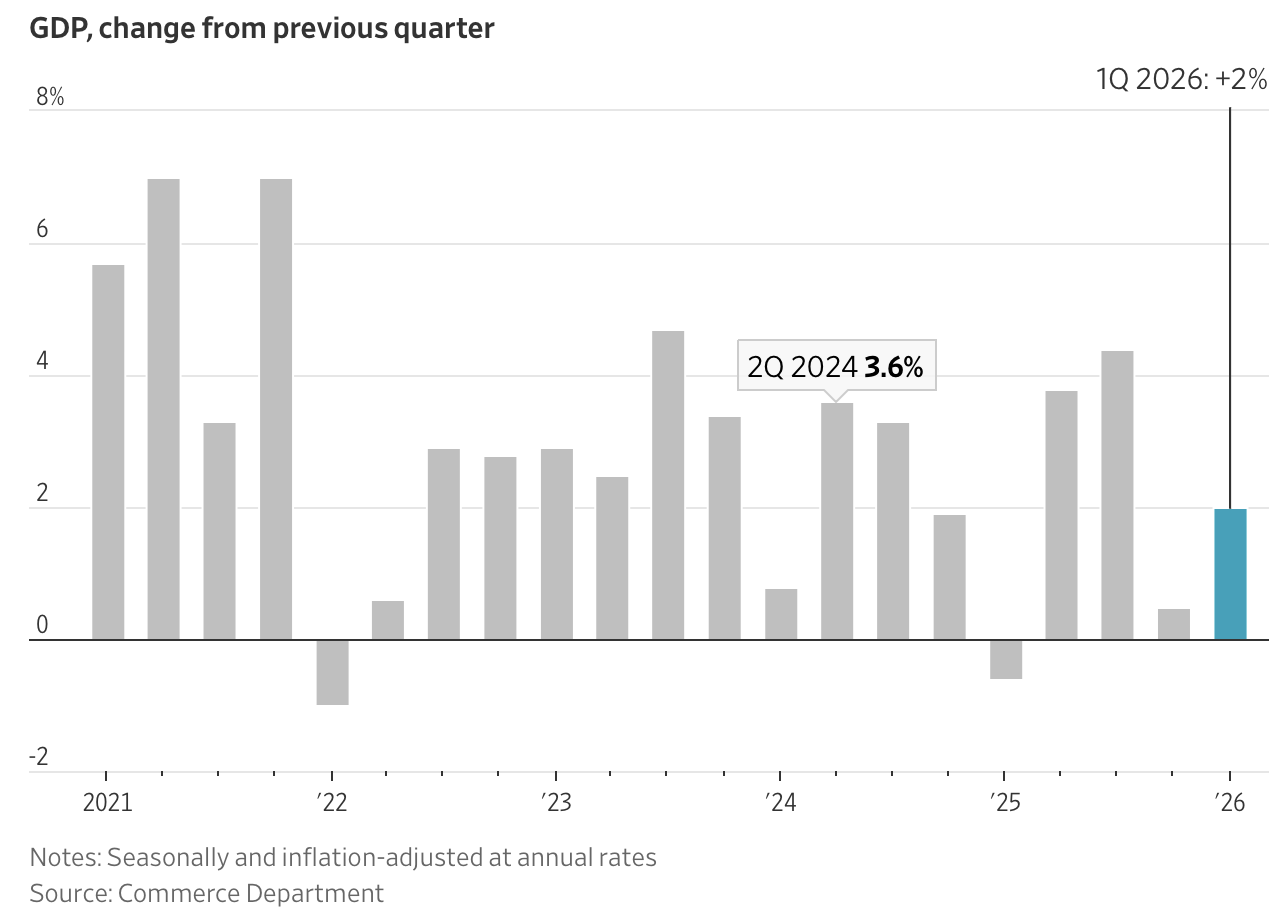

US economic growth rebounded somewhat in the first quarter of 2026, although consumer spending growth slowed to 1.6% compared to the 1.9% of the fourth quarter of 2025. Business fixed investment, fueled by spending on AI and construction of associated data centers, was exceptionally strong.

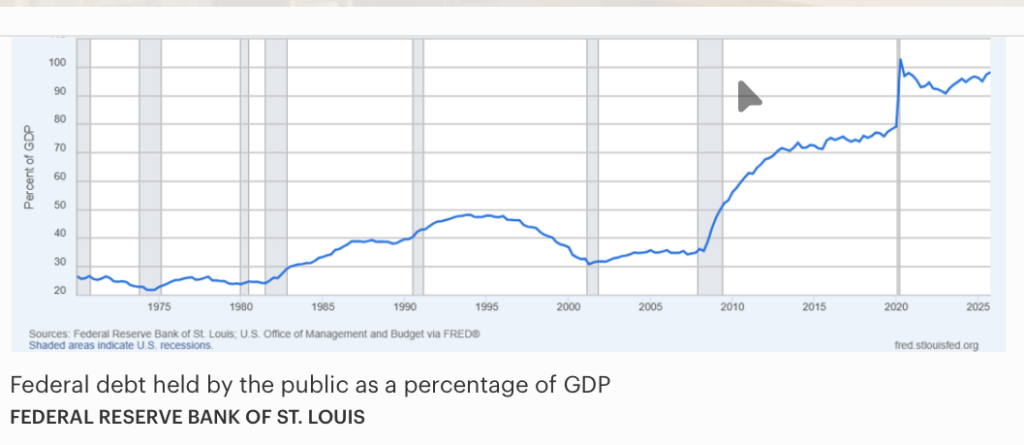

First quarter US economic growth failed to put much of a dent in the rise in federal debt, however. As of March 31, 2026, the national debt was $31.265 trillion, slightly more than the total value of US GDP. Although this has happened only once before in US history, in 1946, this is not a particularly unusual occurrence in the developed world, where France, Canada, Japan, Italy, Spain, Belgium, and the UK all have government debt that is larger than the size of their respective economies. Unlike individuals where debt exceeding one’s income might be cause for immediate concern, the major implications of this development are probably further down the road: 1) an increasing amount of economic growth needed to pay for interest on the debt, 2) a decreasing budgetary flexibility, i.e. an obstacle to funding future new programs without reducing spending in some other program or category and 3) potential economic fragility during a recession that will inevitably make the level of the debt far worse

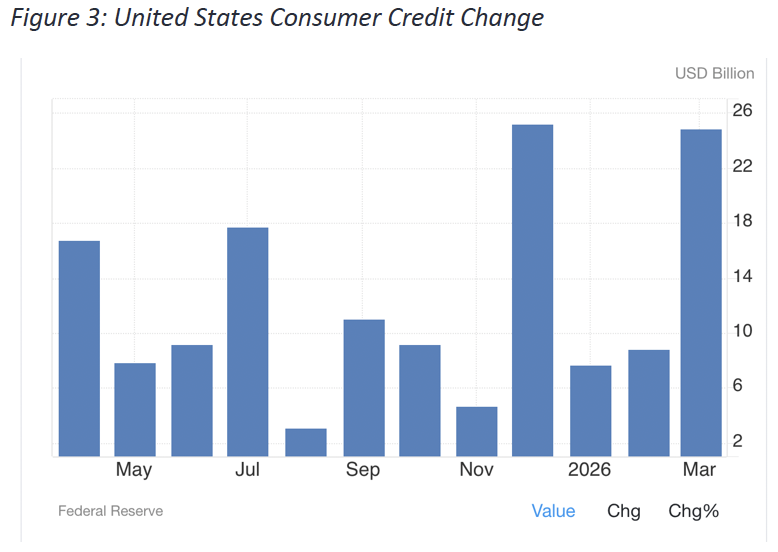

Not to be outdone by the Federal Government, consumer credit also rose sharply in March. There is something of a pattern of consumers increasing their use of credit card debt and then paying that debt down, but there is considerable cause for concern, as credit card debt in March seemed to be fueled by the increase in gasoline prices (pun intended) and a rate of inflation that now well exceeds the growth in wages. Since neither of those trends appears to be reversing in April, there are serious questions as to what comes next. Consumer spending has been remarkably resilient in the face of a stagnant labor market and declining consumer confidence, but as noted above with respect to first-quarter economic growth, consumption growth may be hitting some speed bumps.

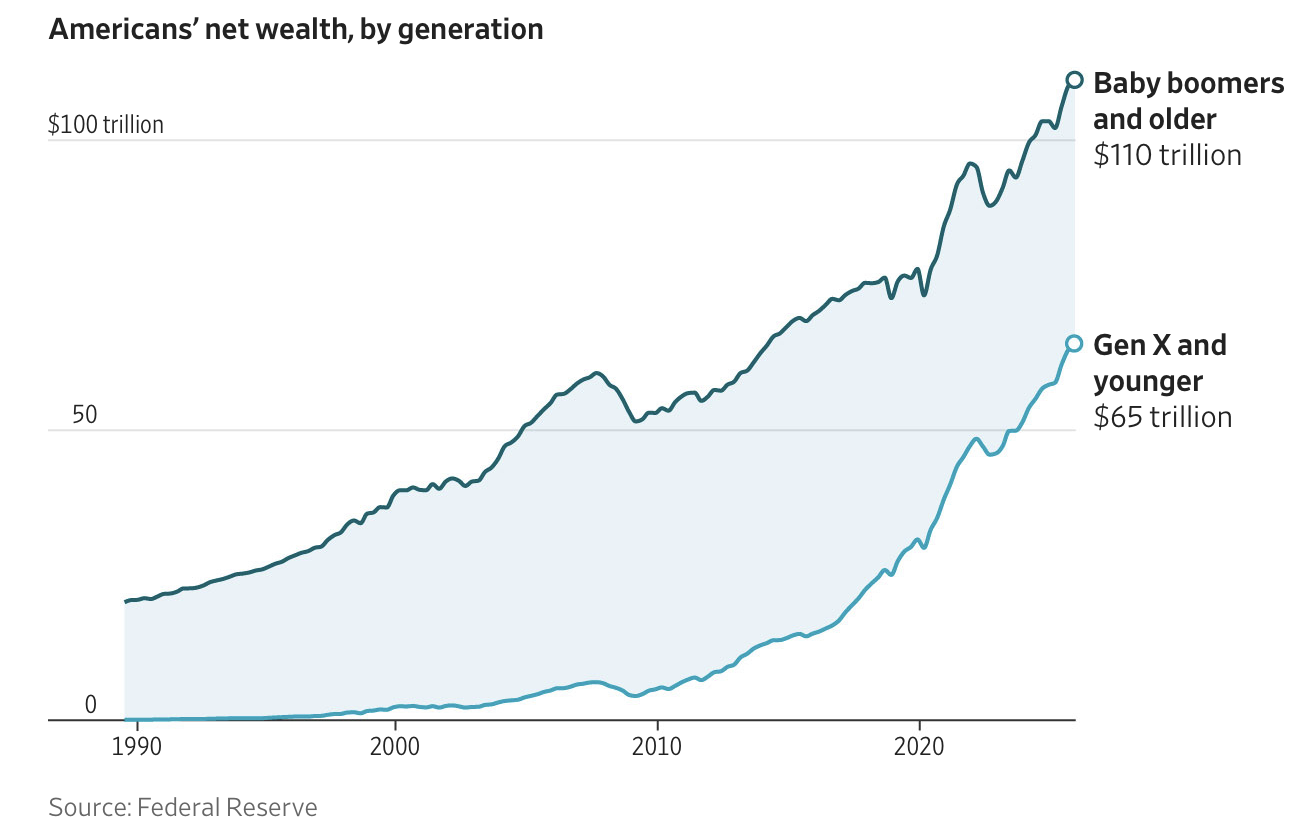

Americans’ wealth continues to rise, an important counterbalance to the peril of rising debt. Of course, aggregate figures belie what is happening under the surface, and not everyone is experiencing this wealth surge. Homeowners and individuals with investment accounts generally have seen their wealth position improve substantially during this decade. Yet there are many who cannot afford home ownership and who are challenged by the escalating cost of daily life, depleting their investments and savings.

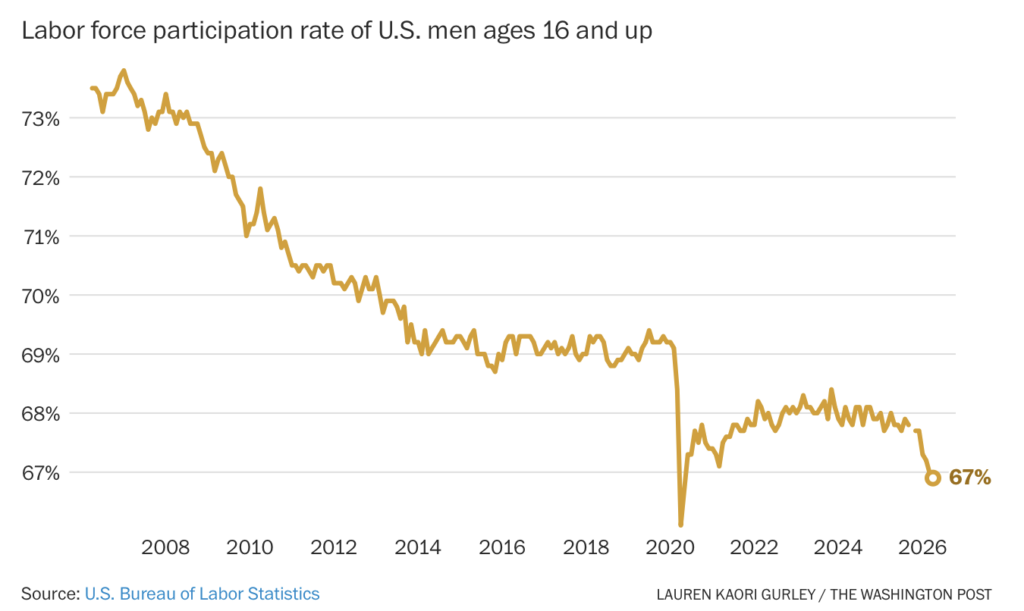

US nonfarm payrolls rose by 115,000 jobs in April, led by continuing employment growth in Health Care, Leisure/Hospitality, and Construction (thank you, all those data centers). The unemployment rate remained at 4.3%, and labor force participation was virtually unchanged. By many measures, labor markets can be characterized as not only “in balance” but also relatively solid. As always, there are very interesting things going on under the headline numbers, however. The decline of men in the workforce— a long-term trend— has accelerated even as the US labor market has firmed up. It appears that this change in male labor force participation is significantly attributable to both accelerating retirements in the upper age ranges and rising school enrollment by younger men. As such, this development is not necessarily cause for concern and may reflect basic and immutable demographic trends. It has certainly caught the attention of policymakers, but it is not at all clear what can and should be done.