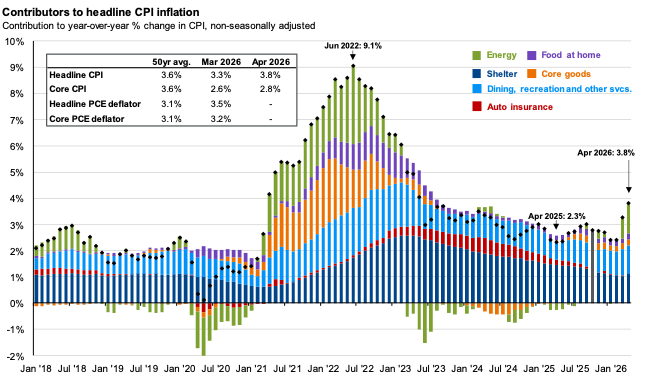

May 15, 2026 – Incoming Federal Reserve Chair Kevin Warsh is inheriting a very different world from the one Jerome Powell took over eight years ago. One sign of that difference is the Consumer Price Index (CPI) reading that was coincidentally released on the day of his confirmation. It came in at 3.8%, the highest level since June 2023.

While the immediate cause of the recent increase is energy prices—driven by continued disruption in the Strait of Hormuz—the reading also reflects the inflation environment we’ve been living in for the past four years. In the post‑2022 world, 2% is no longer the ceiling on inflation; it is the floor. Instead of bumping up against it, we are bouncing off it.

The causes of this shift are complex, but they reflect the two forces that tend to drive inflation: strong demand and constrained supply. Both have been present over the past four years. Demand surged during the pandemic, when shifts in consumer behavior and significant government stimulus pushed inflation above 9% in June 2022. Even as the pandemic subsided, supply constraints persisted. Later, tariffs and disruptions in global energy markets—from the war in Ukraine and, more recently, the conflict involving Iran—continued to put upward pressure on prices. Four years later, inflation has declined, but it has not returned to the 2% level that defined the prior decade.

There is also a social element to inflation that is playing out around us. Inflation tends to hit a particular nerve with consumers. It creates the sense that wages and savings are steadily losing ground and that the effort required to maintain a given standard of living is increasing. The hamster wheel is not only ever turning, but it’s also speeding up. In response, workers seek higher wages, which can in turn raise production costs and reinforce inflationary pressures.

Importantly, the higher inflation environment we are living in also reflects the strength of the U.S. economy over the past several years. For much of the decade following the Global Financial Crisis of 2008, economists yearned for signs of inflation that would indicate stronger economic activity. In Europe, concerns about disinflation—an even more challenging dynamic, in which falling prices discourage investment and hiring—led the European Central Bank to experiment with policies such as negative interest rates.

In all, today’s environment looks very different from the one Powell inherited in 2018. Growth has been stronger, but also more K-shaped, leaving parts of the population behind. Corporate earnings have remained solid, and profit margins are near historic highs, even as concerns about AI-driven job displacement are rampant. Globally, multiple regions are showing signs of economic resilience, though supply chains remain strained and are no longer organized solely around efficiency.

This environment presents a unique challenge for incoming Fed Chair Kevin Warsh. He enters the role with the added task of demonstrating independence from the White House, which continues to push for lower interest rates. Recent employment data has provided some reassurance that the economy remains resilient despite higher prices, but the Federal Reserve’s dual mandate—balancing maximum employment and price stability—leaves the new Chairman on an uncomfortably high tightrope.

Please reach out if you would like to discuss how a higher-for-longer inflation environment may affect your financial plan.

— AMD

Source: BLS, FactSet, J.P. Morgan Asset Management. Contributions mirror the BLS methodology on Table 7 of the CPI report. Values may not sum to headline CPI figures due to rounding and underlying calculations. “Shelter” includes owners’ equivalent rent, rent of primary residence and home insurance. “Food at home” includes alcoholic beverages. Headline and core PCE deflator inflation shown are based on seasonally adjusted data due to data availability. Official October 2025 data unavailable due to government shutdown and data shown are J.P. Morgan Asset Management estimates. Guide to the Markets – U.S. Data are as of May 13, 2026.