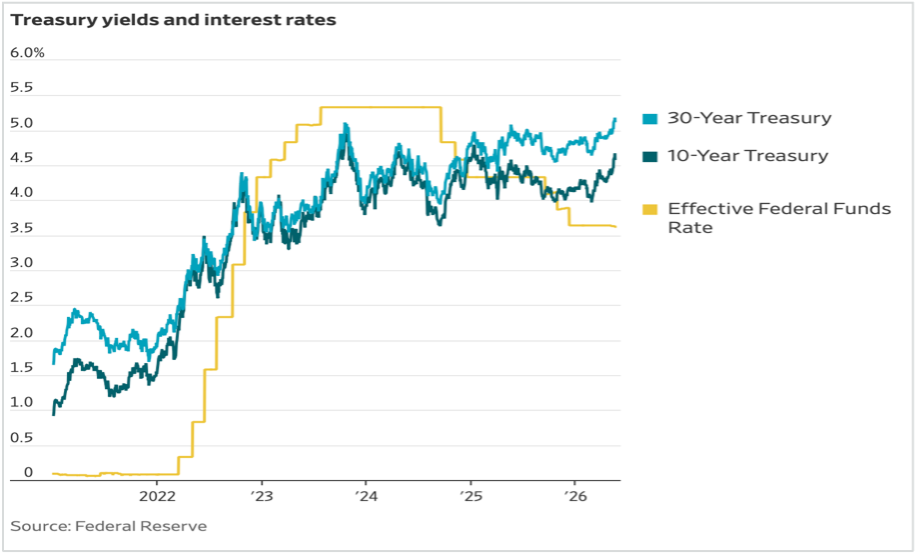

Bond yields got everyone’s attention this week. The 30-year Treasury hit its highest level in almost 20 years (going back to just before the Great Financial Crisis), and the 10-year Treasury reached some of its more hand-wringing heights of the last three years. The speed with which this move occurred was almost as relevant as the level itself. It appeared as if bond markets suddenly realized that inflation was accelerating and government deficits were increasing globally. A more plausible explanation is that institutional bond buyers gave up on the possibility of any meaningful near-term change in the conflict with Iran (precisely as a few ships started to pass through the far-too-long closed Strait of Hormuz, of course). Bond markets don’t usually move like this, but these are highly unusual times, and yields can come down just as fast as they went up. An important caveat is warranted, however: the longer the Strait of Hormuz remains closed, the greater the economic damage and the more difficult it becomes to service the debt on those growing government deficits.

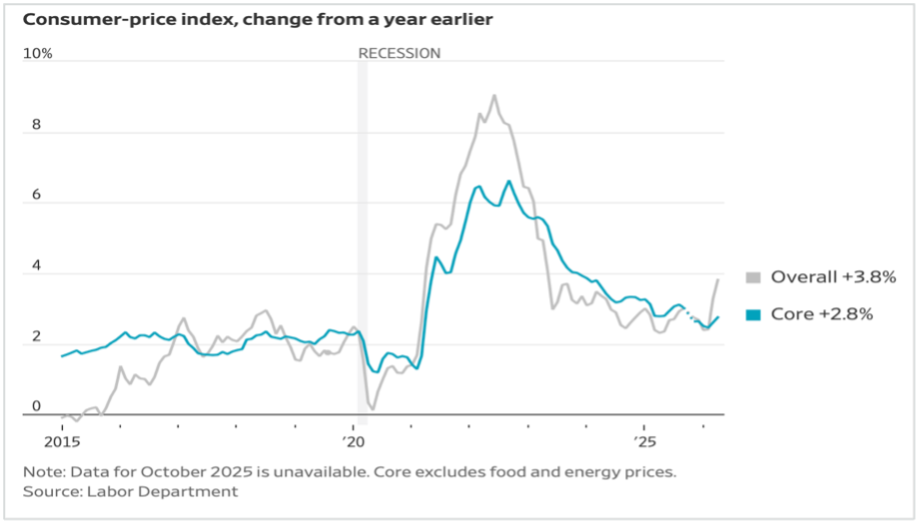

Monetary authorities that set target interest rates are trying to find greater patience than bond markets. The Fed and other central bankers are fervently hoping for a sustainable resolution to the shipping constraints that have raised prices and curtailed supplies for so many energy and industrial commodities. Truthfully, no one likes raising interest rates and adding to the pain from war and tariffs being felt by businesses and consumers. Yet patience is wearing thin and concern is mounting, especially in the United States, that rising inflation expectations may soon become embedded in the broad economy. The fact that wage growth in the United States has not accelerated, despite relatively strong economic activity, is possibly the only thing keeping the Fed’s hand on raising interest rates, an action almost certain to cause a major confrontation with the White House. Recently released minutes from the Federal Reserve’s interest rate setting meeting at the end of April showed a surprising amount of discussion of and support for higher interest rates if inflation stays in the 3-4% range, irrespective of the clear intention of new Fed Chair Warsh to move rates lower.

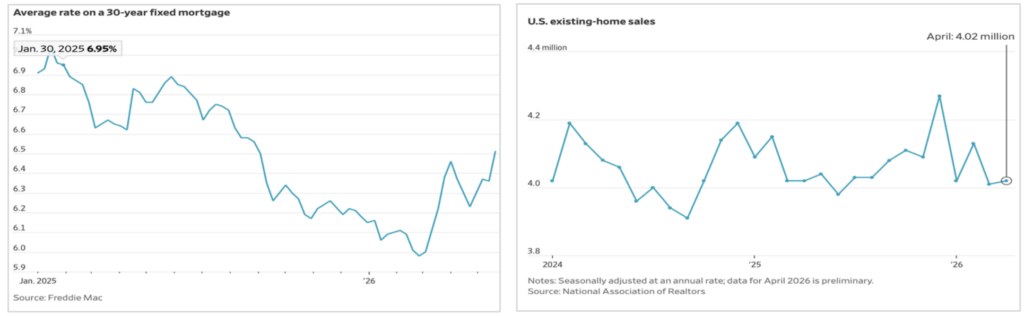

US mortgage rates are highly sensitive to fluctuations in bond yields, especially the US 10-Year Treasury yield. Declining mortgage rates early in 2026 provided a significant and hopeful boost to existing home sales, but as war broke out, inflation rose, and the Fed went into a holding pattern on rates – and bond yields started to climb—mortgage rates quickly moved back above the key 6% bar. Perhaps unsurprisingly (but it did turn out to surprise many), existing home sales in April flatlined.

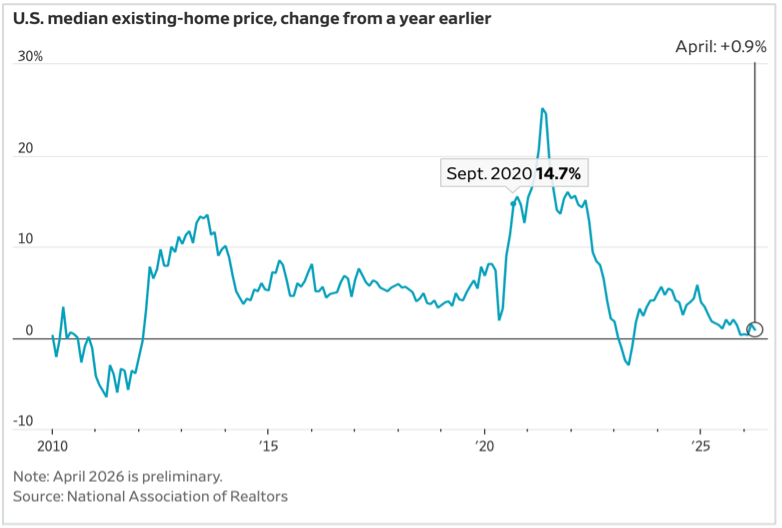

The weakness in housing sales is all the more notable given the considerable evidence that this may be the best market in years for which to search for and buy a home. Many real estate markets have turned into “buyer’s markets”, with sellers willing to offer discounts and other accommodations to close a sale. Escalating home prices during the pandemic were a significant contributor to the high inflation numbers that pushed the Fed to raise interest rates. Home prices are not playing a similar role in the current rising inflation trend and are likely to continue to be a factor pulling inflation lower, not higher.