The Tariff Tantrums are back. Europe continues to work on cutting deals with Washington, now just a bit more frantically. “Tariff Letters” sent out this week warning of significant action on August 1, at the latest, caught several Asian trading partners by apparent surprise however. In what can be only termed extraordinary, the head of the Japan Business Federation criticized the Japanese government for taking an imprudent stance in responding to the US trade negotiation team by refusing any concessions. More to come.

The unexpected announcement of a 50% tariff on copper imports certainly qualifies as “more.” Copper prices shot up immediately, much to the dismay of the construction industry (approx. 45% of US copper consumption) and electrical and electronic manufacturers (approximately 23% of US copper consumption.) The US has substantial copper reserves, but lacks smelting and refining capacity; historically, it takes more than 10 years to build a new smelting/refining facility. On-shore copper inventories have been built up this year, in anticipation of some sort of tariff action – the availability is there, it just is going to cost a lot more. And no, this is not the way to make US homes more affordable.

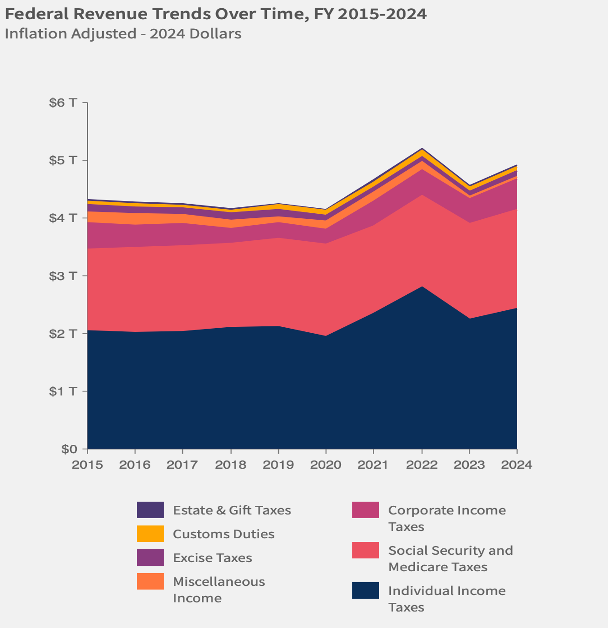

Tariffs (Customs Duties) are a small part of government revenues, hovering around 1.6%. These revenues are up sharply this year – raising an estimated $100 billion thus far, compared to roughly $75 million for all of 2024—but will still be a relatively small part of Federal Budget calculations. The FY2025 US Budget Deficit as of April 2025 was $1.1 trillion, and the Congressional Budget Office is projecting a full-year 2025 budget deficit of $1.9 trillion, including reasonable projections for tariff receipts.

It appears that some recovery in the US Dollar exchange rate has been aborted by the recent flurry of tariff announcements. Global concerns about US economic health, particularly in terms of the projected impact on national debt from the One Big Beautiful Bill Act (“OBBBA”), had been moderated somewhat by the perceived strength of second quarter US economic growth and relatively healthy job creation. However, both growth and inflation worries for the second half of 2025 have now been re-introduced.

Sometimes the data that one wants the most to see arrives with considerable lag. There is a great deal of talk about the status of the US dollar as a reserve currency, and much speculation as to the current state of global central bank reserves. As of the end of 2024, the US dollar was still the dominant central bank reserve holding, with no significant change in the holdings of Euros. But holdings of gold had increased noticeably. It is likely that this trend has continued to unfold in 2025 and may very well have accelerated, placing on-going downward pressure on the US Dollar exchange rate; good news for US exporters but more bad news for import prices.