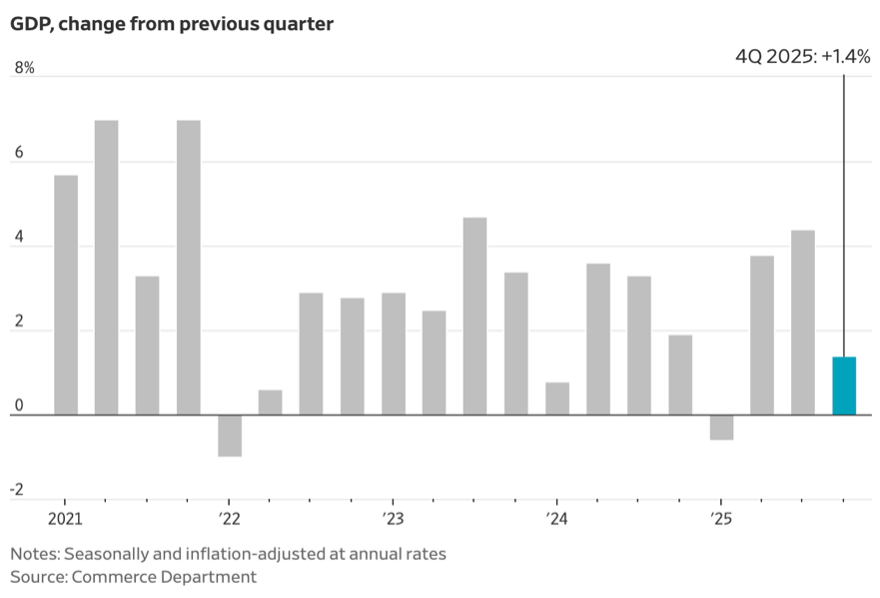

US GDP growth for the fourth quarter of 2025 was expected to be north of 3%. The number released a bit later than usual because of various government shutdowns was a major disappointment, apparently because of the government shutdowns themselves. A fairly complex explanation provided by the Bureau of Economic Analysis(BEA) about the manner in which the government shutdown between October 1, 2025, and November 12, 2025, impacted the GDP calculation is nevertheless causing some significant head-scratching. And a softening of consumer spending that was not signaled by retail industry data for much of the quarter is raising questions.

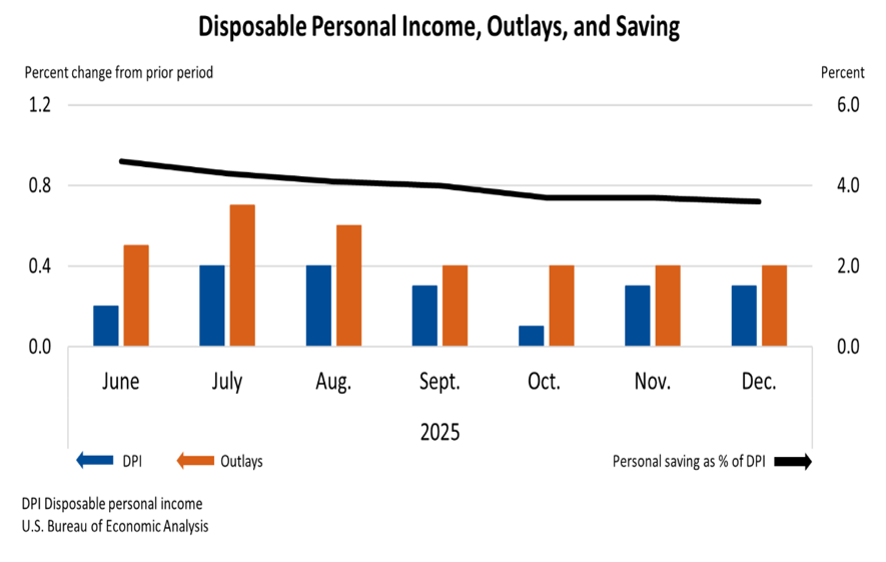

A nice summary of US consumer spending in the fourth quarter is illustrated by BEA data released today (February 20) on personal income, spending, and savings. The slowdown in both income and spending from the third quarter, when US GDP grew at 4.4%, is readily apparent. At the same time, the fourth quarter pace has seemed sustainable, and early data in 2026 may support an increase in consumer spending, barring the effects of extreme cold weather. The University of Michigan Consumer Sentiment Survey for February reported another small increase in consumer confidence for February, and a deceleration in consumer inflation expectations.

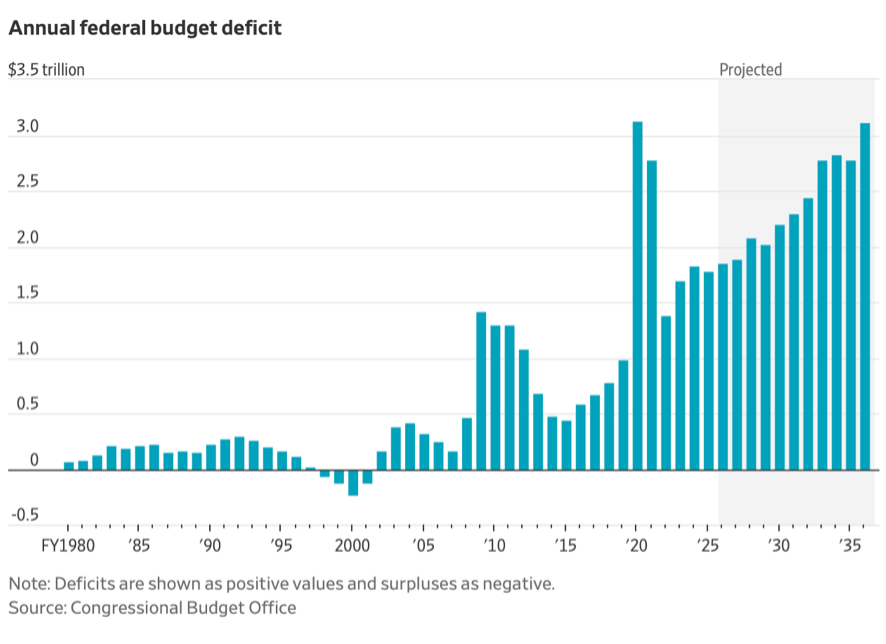

With the release of unexpectedly weak economic data for the end of 2025, fiscal authorities (read: White House) are not having a great week. Earlier, the Congressional Budget Office (CBO) distributed short- and long-term projections for the US budget deficit, highlighting the known fiscal problems confronting both the White House and Congress. Despite massive revenues from tariff receipts (some just now struck down by the Supreme Court), the outlook for the budget deficit continues to rise, with tax cuts passed in 2025 pushing the deficit in the wrong direction if economic growth does not pick up as planned.

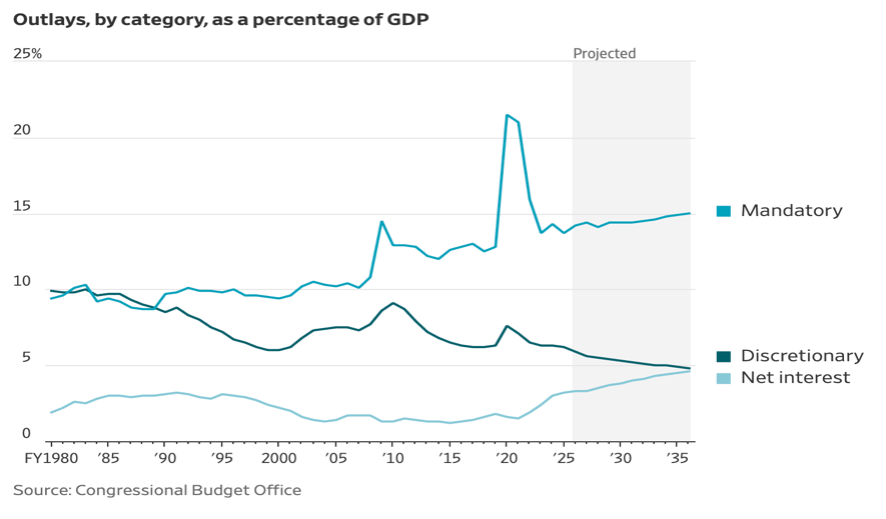

It is notable that discretionary outlays by the federal government have declined as a percent of GDP, while mandatory outlays for Medicare, Social Security, and other “social safety-net” programs have increased. Both developments reflect long-term trends influenced by demographics and underlying costs. The increase in net interest payments as a percent of GDP is a much newer development, however, associated with the massive increase in budget deficits kicked off by the sweeping tax code changes of the Tax Cuts and Jobs Act of 2017 (TCJA.)

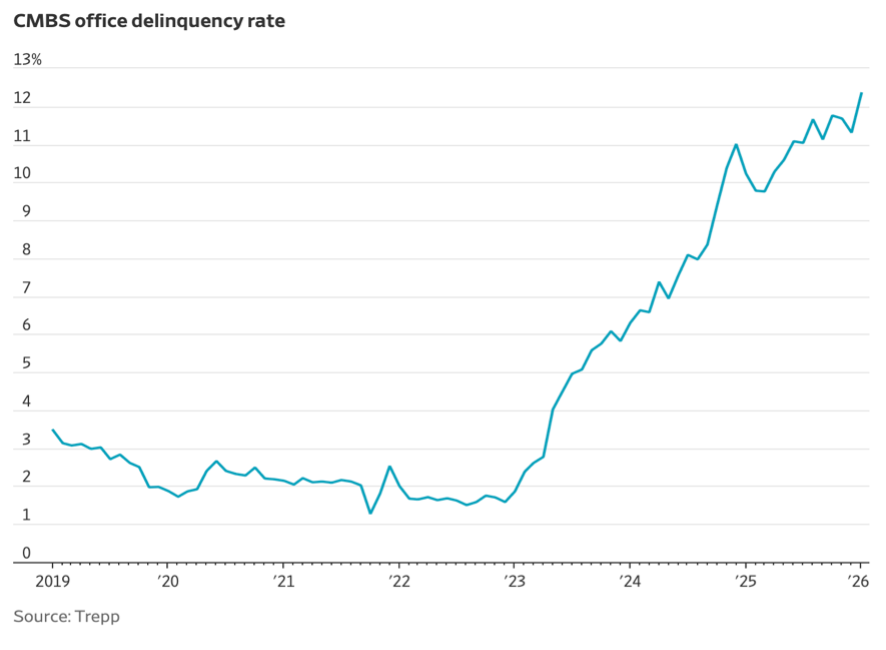

Another development associated with newer, possibly structural, changes is the rising delinquency rate in the Commercial Mortgage Backed Securities (CMBS) office marketplace. CMBS represents only an estimated 15% of total borrowings in the office building sector, but is considered an indicator of the ongoing problems associated with altered workplace use and location. While there is little implication of severe problems ahead for the financial sector at large as these properties are taken over by lenders, it is likely that some lenders and investors will indeed feel this pain. After numerous loan extensions and restructurings, it is also clear that this is not a problem that will be immediately fixed by economic growth.