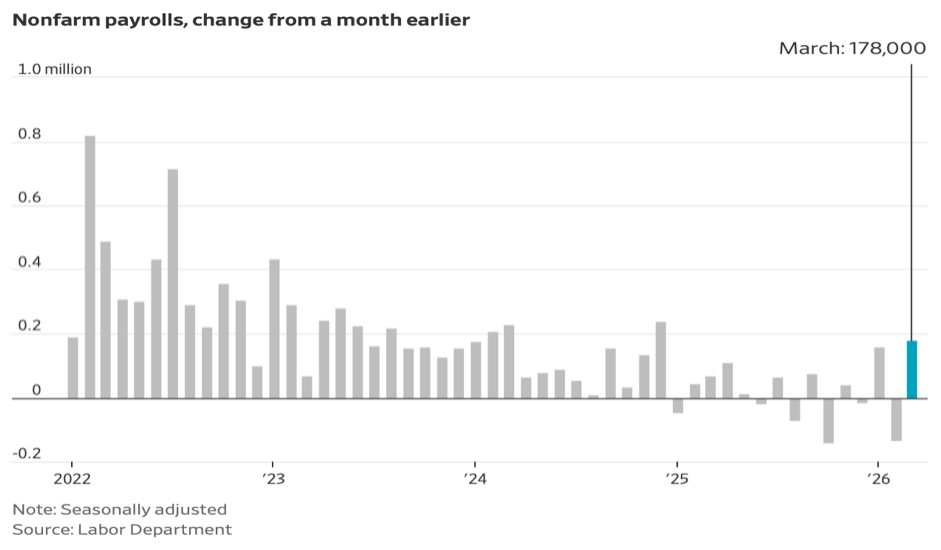

March nonfarm payroll numbers were, to say the least, a big surprise. The 178,000 net new jobs created contrasted nicely with a revised 133,000 job loss in February and confounded observers who have been tracking rising layoff announcements and falling job openings. That, too, should be no surprise, since layoff announcements are notoriously “soft” – one has no idea when the layoffs will occur, whether they include the elimination of jobs not filled, and whether job openings have been declining very much or very rapidly. Perhaps the most interesting part of the report was the decline in the unemployment rate to 4.3%, made possible by 400,000 people leaving the workforce.

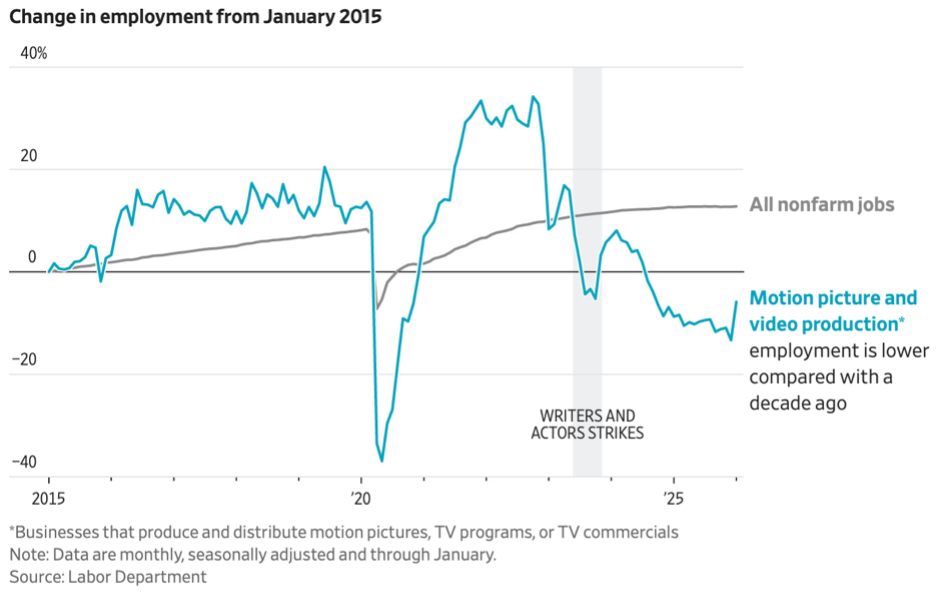

One through-line in employment growth has been the robust expansion of health care jobs. A different through-line is seen in the US motion picture industry, where employment trends have not been favorable for several years. At various times, the decline in motion picture industry jobs has been described as “The Death of Hollywood”, but the implied geography of the phrase ignores that employment is down broadly as the US industry copes with a changing entertainment industry landscape and shifts production jobs overseas to lower-cost locales.

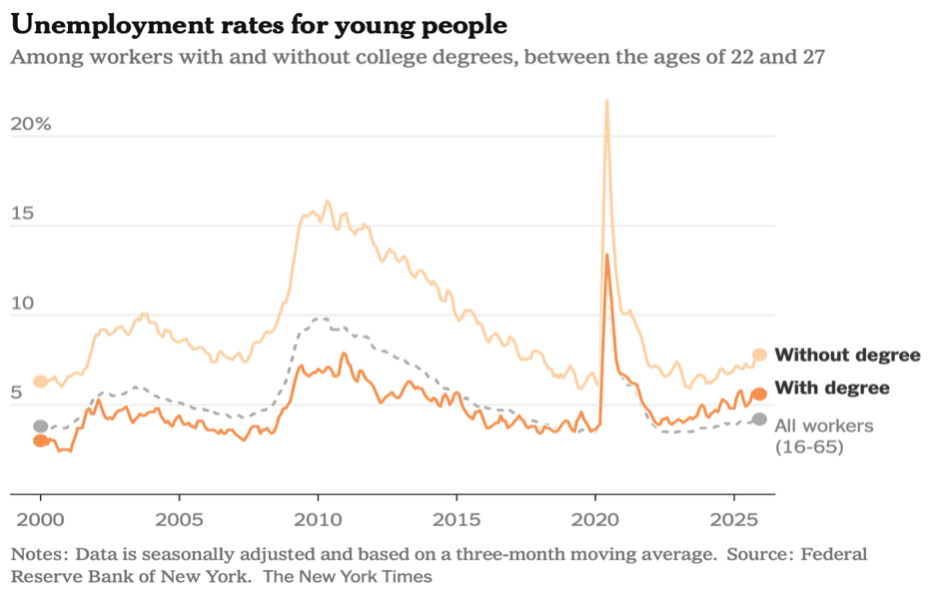

Unemployment rates are always a bit of a glass-half-full concept. Overall, US unemployment rates are quite low. Disaggregated, a different picture emerges and can be used to dispute the actual significance of, for example, the March drop in the unemployment rate. It is speculated that the difficulties recent college graduates face in finding a job make people anxious and nervous about the economic outlook; no doubt this is true for parents who may be hosting those graduates at home for an unexpectedly long time. However, a higher unemployment rate among young people during times of rising costs and slowing economic growth is a fairly typical development, as businesses must accept the greater cost of training a new entrant to the labor force. Furthermore, it is still true that unemployment rates are higher for those without college degrees. A bit more atypical at this point is the lower unemployment rate when older workers are included, reflecting what is known to be characteristic of current US employment: older workers are not leaving, and older workers are working longer (working to higher ages), and therefore the labor market is a bit “jammed up” for newer workers.

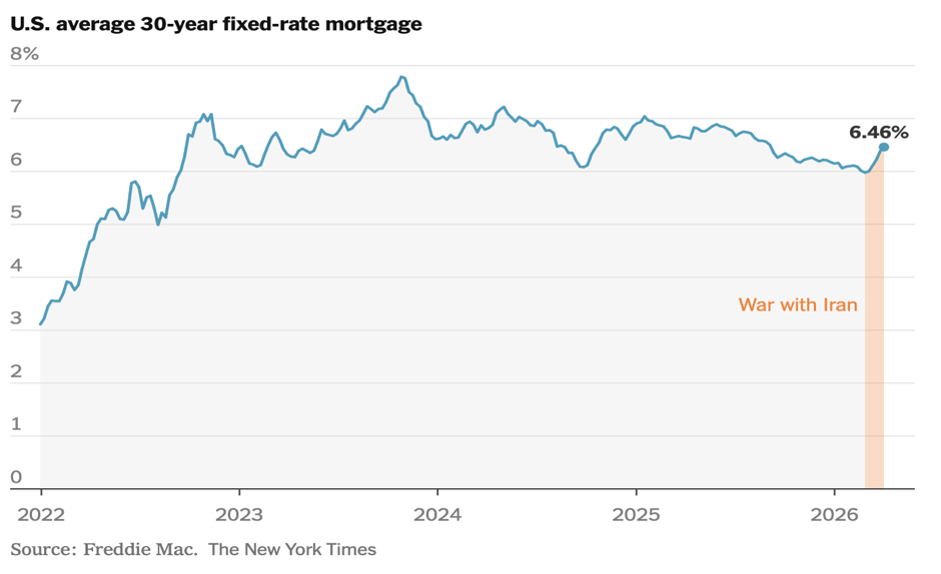

Mortgage rates are not making it any easier for homebuyers, whether they are working or not. The recent increase in mortgage rates is driven by the overall increase in Treasury rates since the start of the war with Iran and illustrates why a focus on Federal Reserve interest rate decisions can sometimes miss the point. Home prices have provided some counterbalance to interest rates; it is estimated that as much as one-third of homes for sale have had their asking prices reduced significantly in 2026. Yet this should not be interpreted as a decline in home prices, and the National Association of Realtors reported a slight 0.1% increase in existing home sale prices in February.

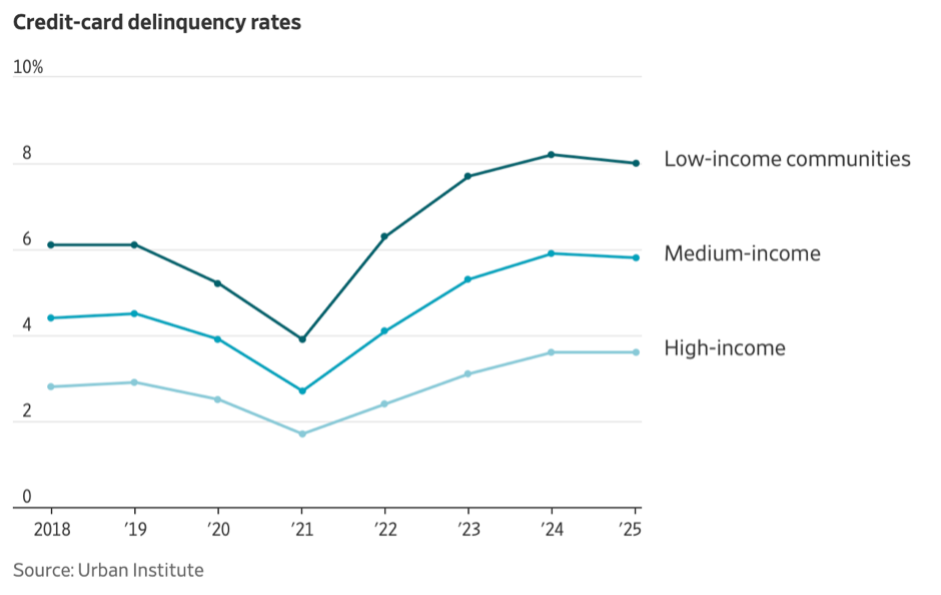

Rising interest rates also carry implications for credit card users and the balances they may carry on their cards. A slight decline in credit card delinquencies was noted by some measurements in 2025 and judged to have continued to decline marginally in 2026. Many banks have recently announced intentions to boost their small business lending and increase credit card sales as a result of regulatory relief from the Federal Government (reductions in reserve requirements, etc.), a move which also indicates that the banking industry does not yet see a substantial increase in household financial stress. It would not be an entirely unusual development if more aggressive bank credit card sales eventually lead to higher delinquency rates, especially if inflation continues to place cost-of-living pressures on American households.