Good morning,

Friday’s stronger-than-expected May employment report appeared to have an outsized impact on markets. Following a more than 20% advance in the S&P 500 Index over just three months, some degree of pullback was to be expected. The jobs report served as the catalyst—not the underlying reason—for the S&P 500’s -2.6% decline on Friday.

Notably, the market’s initial reaction to the employment data was muted, with futures trading essentially unchanged. However, once the cash market opened an hour later, a steady stream of sell orders emerged and persisted throughout the day. In an overbought market where investors are sitting on substantial recent gains, selling can quickly become self-reinforcing. Friday’s decline looked more like an overdue correction than a fundamental shift in trend, with the heaviest pressure falling on the sectors that had generated the largest profits over the previous three months.

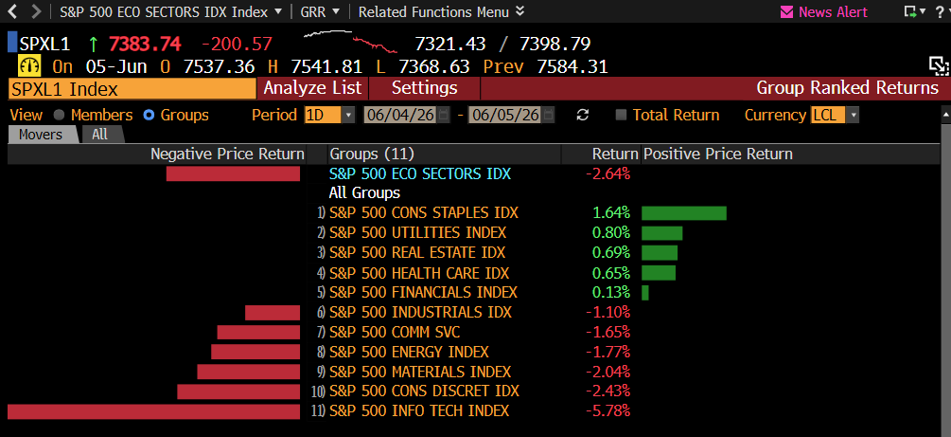

Interestingly, five of the eleven S&P 500 sectors finished higher on Friday. Technology, however, bore the brunt of the selling, declining -5.78% and accounting for most of the index-level weakness. See Friday’s sector performance chart below (Bloomberg).

Has the market pivoted lower? Has this bull market finally topped out? Unlikely. At worst, Friday may mark the beginning of a topping process that could take months to unfold. More likely, the market will make new highs before this bull cycle ultimately retires. That remains the message from the weight of the evidence today. When that message changes, I won’t wait for a Monday Morning Note to tell you.

The week ahead is packed with potential market-moving events. Today marks the start of Apple’s Worldwide Developers Conference, where investors will be looking for either meaningful AI progress or disappointment. Midweek brings CPI and PPI inflation reports, and Friday is expected to feature the highly anticipated SpaceX IPO—the largest public offering in history.

There is certainly no shortage of catalysts for volatility, and I suspect investors are well aware of that fact. But remember, the market has a habit of fooling the greatest number of participants at the most opportune time. It is entirely possible that Friday’s storm has already passed. The VIX briefly surged above 20, a level often associated with heightened investor anxiety, and may retreat back toward calmer levels if this week’s news flow proves less threatening than feared. As always, we’ll let the market tell us the story.

Be well,

Mike