Writing a monthly letter for March—now on April 7th, just hours from the latest Trump deadline, accompanied by the stark warning that “a whole civilization could die tonight”—feels almost beside the point.

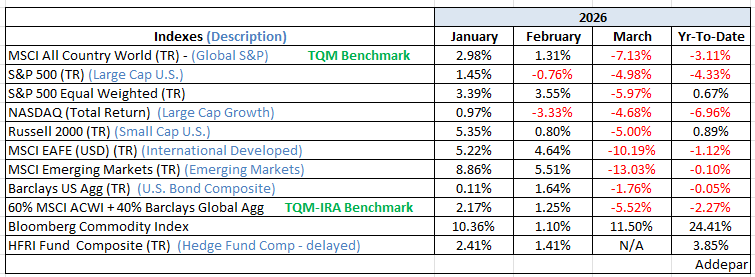

March, however, can be summarized succinctly: war with Iran. It began on the final day of February, and most market observers expected it to be resolved within weeks. That has not been the case. The chart below reflects the impact across major global asset classes over the past month. While we have seen a partial rebound in early April, both the war and the markets remain highly fluid.

As your wealth advisor, my focus is less on the day-to-day geopolitical developments and more on how markets interpret and respond to them. Markets, over time, convey a message through trend.

Prior to the conflict, we were in a mature—but still intact—bull market, with indicators leaning constructive. During March, that message weakened but did not break. The market shifted into a more neutral, trendless state—neither clearly bullish nor bearish.

Thus far in April, underlying indicators have improved more than headline price movements might suggest. That is a modest but meaningful positive and supports our decision to leave portfolios unchanged for now. As always, if the market’s message changes, we will adjust risk exposure accordingly.

Be well,

Mike