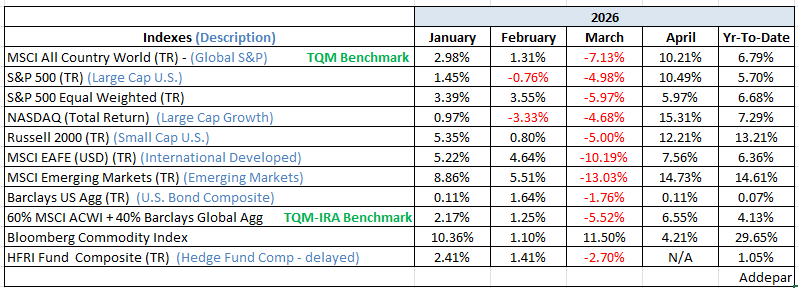

Recall how markets limped into the end of March—fatigued by four weeks of war with Iran, a significant portion of the world’s fuel supply effectively shut in, and a fragile hope that hostilities might soon end without further escalation.

There is an old saying: markets tend to do what fools the most. That is precisely what unfolded in April. The war did not end. Oil did not flow. Yet equities delivered one of the strongest monthly performances in history—more than offsetting March’s losses.

April became a case study in market resilience. Despite persistent geopolitical strain, equities pushed to new highs, largely looking through the noise. While multiple narratives competed for attention, one ultimately dominated: a renewed risk-on appetite fueled by a powerful rotation back into companies tied to artificial intelligence.

That willingness to look through adversity has carried into May. Even with the Strait of Hormuz effectively closed and energy prices elevated, markets have remained firm through the first several trading days.

Historically, top-decile monthly returns tend to be followed by constructive forward expectations, as models shift more bullish. This backdrop is reinforced by a remarkably strong earnings season, which lends fundamental support to the current advance and suggests a favorable trajectory into year-end.

That said, the path forward is unlikely to be linear. Any effort to resolve the conflict—particularly one involving the dismantling of Iran’s nuclear capabilities and the reopening of Hormuz—would almost certainly introduce periods of heightened volatility and the potential for sharp, tactical pullbacks.

In short, while a storm may lie ahead, the outlook on the other side remains constructive.

Be well,

Mike