Following April’s powerful rebound from the March selloff, markets remained constructive in May, though not quite as euphoric as the month before (see returns chart below).

The primary drivers of last month’s gains were continued geopolitical de-escalation and a corresponding shift in investor focus. As concerns surrounding the conflict receded, markets were increasingly able to concentrate on fundamentals—most notably the S&P 500’s impressive 22% year-over-year operating earnings growth in the first quarter and the extraordinary capital spending associated with the ongoing artificial intelligence buildout.

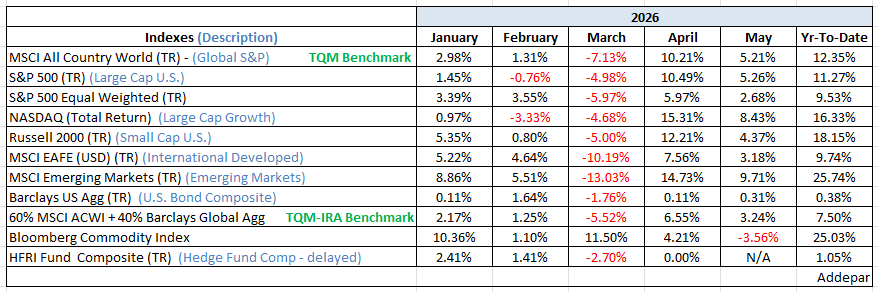

Through the first five months of the year, the S&P 500 has gained 10.7%, putting the index on pace for a fourth consecutive calendar year of returns exceeding 15%. The only other period in modern market history to achieve such a streak was the five-year run from 1995 through 1999. While there is considerable debate over how closely today’s market resembles the late-1990s environment, our greater concern remains what lies ahead in the second half of the year.

A few of the ingredients that ultimately contributed to the 2000 bear market—namely rising inflation pressures and emerging technical divergences—are beginning to appear today. At present, however, neither is flashing the type of warning signal that has historically ended a bull market.

As is often the case, today’s market presents investors with a collection of seemingly conflicting observations. In reality, markets are almost always sending both positive and negative signals simultaneously. The key is not simply identifying the signals, but understanding their timing. Forecasts can coexist for extended periods before ultimately resolving themselves.

From a momentum perspective, the evidence remains compelling. The S&P 500 has gained 16.1% over the past two months, representing its strongest two-month advance since May 2020 and the fourth-strongest such move in the post-war era. Historically, whenever the index has risen at least 15% over a two-month period, it has been higher one, three, and six months later in every prior instance.

At the same time, caution remains warranted. Even if a formal peace agreement emerges, the economic effects of war tend to arrive with a lag. Supply-chain disruptions, resource shortages, and shifting trade patterns often take months to work their way through the global economy. As a result, we continue to expect a more challenging economic backdrop during the second half of the year, accompanied by tighter monetary policy in several parts of the world.

Technology stocks also deserve close attention. Following their recent surge, the sector is among the most overbought on a two-month basis in decades and may be vulnerable to a near-term pullback—or at minimum, a period of consolidation. Returning briefly to the late-1990s analogy, investors witnessed several similar momentum bursts and subsequent pauses before the market ultimately reached its final peak.

For now, the weight of the evidence continues to favor the bulls. Earnings growth remains robust, liquidity conditions are supportive, and momentum is difficult to ignore. Nevertheless, elevated valuations, overextended technical conditions, andthe potential for delayed economic consequences from geopolitical events suggest that the path forward may be less straightforward than the strong gains of the past two months would imply.

Be well,

Mike