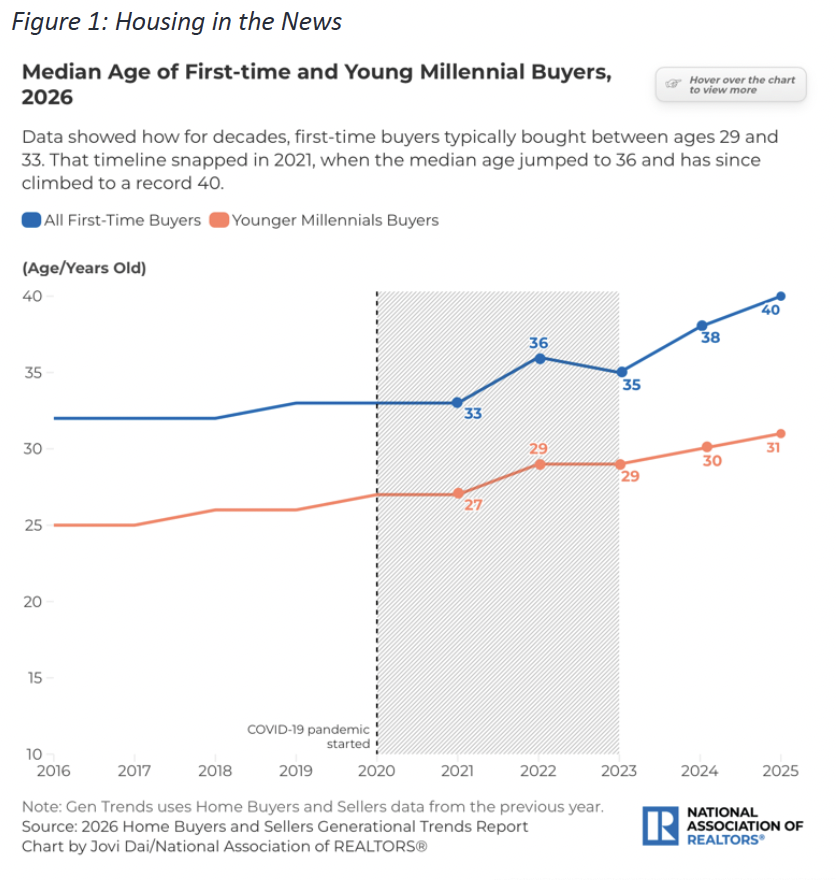

On Tuesday, June 23, the US Congress passed the 21st Century ROAD (“Renewing Opportunity in the American Dream”) to Housing Act, a piece of legislation focused on increasing the supply of housing in the United States by reducing various federal regulations and costs imposed by unnecessary environmental reviews. The bill also places some restrictions on home purchases by institutional investors (those owning more than 350 homes), although a number of exemptions mean that this part of the legislation is less restrictive than originally intended. Housing starts fell 15.4% in May, and new home sales declined 7.3%, highlighting the housing market issues the bill attempts to address. Buyers—especially first-time buyers—have put off home purchases as home prices have risen sharply (note: “younger millennials” are defined as those born between 1990 and 1998). President Trump has declined to sign the legislation, but it will become law within two weeks, automatically.

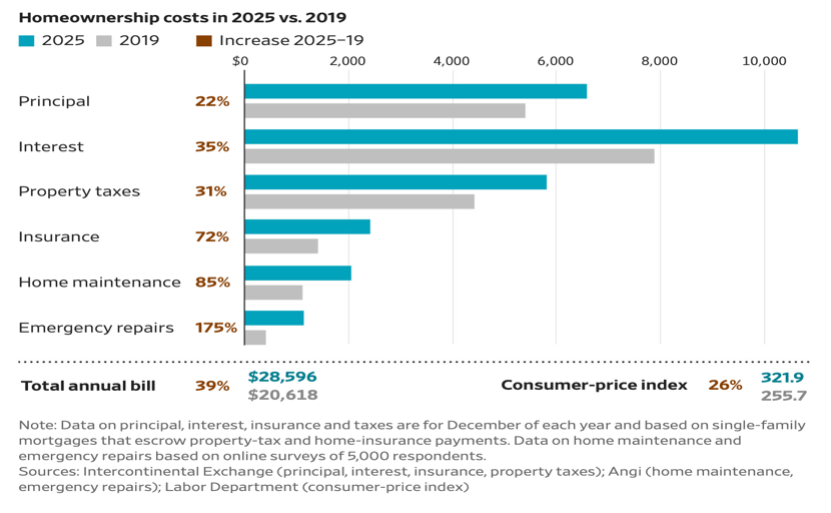

The challenge of housing affordability is highly complex. Today’s millennials (ages 28-45) are generally thought to be better positioned in terms of income and ability to qualify for a mortgage than previous generations at the same age markers. The sharp increase in the cost of insurance and home maintenance is viewed as influencing home buying decisions more than in the past, with colloquial evidence from home sellers indicating that prospective buyers are very focused on avoiding home repair/improvement expenditures post-purchase. Nevertheless, despite some well-publicized data showing insurance outlays for existing owners exceeding monthly mortgage expense, it would seem that a decline in both new home prices and financing costs would be of substantial benefit in making housing more attractive and accessible.

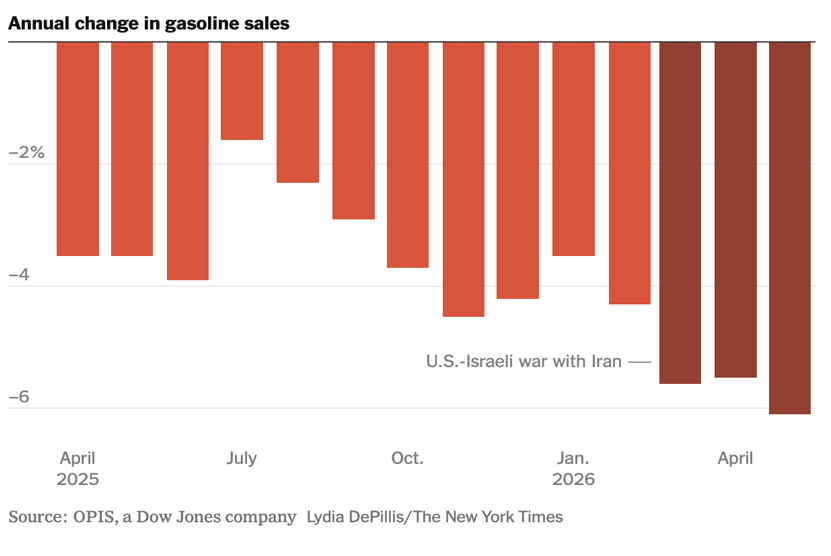

Gasoline sales also fell in May, below expectations (May is usually a time when holiday travel and school and family events tend to increase driving), but not necessarily surprising in light of the high prices at the pump. The year-long trend coincides with increased household costs and rising inflation from a variety of sources, including the imposition of tariffs and the conflict with Iran, suggesting that consumers are responding to the high price of gasoline in the context of other price pressures on household budgets. Used car sales continue to show car buyers seeking to improve fuel efficiency, a development that will have long-term impacts on gasoline consumption.

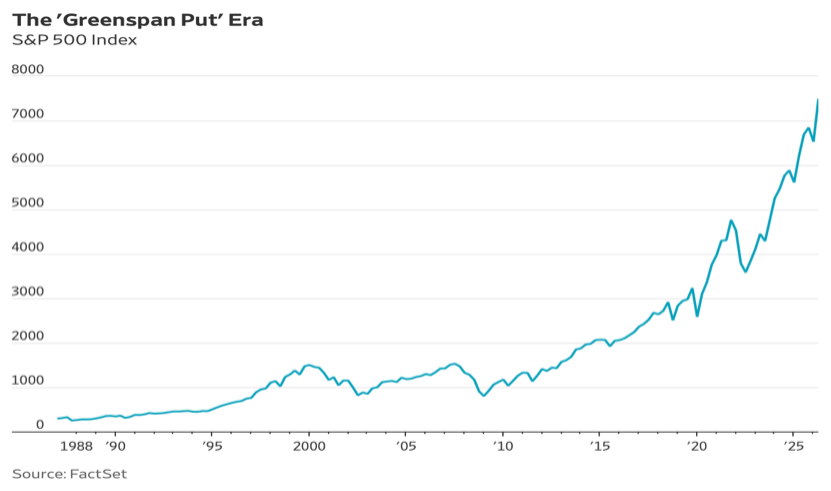

Household wealth has a substantial influence on home-buying decisions, beyond the obvious impact on financing the purchase. Many buyers have built up wealth in retirement accounts (IRAs and 401Ks typically are not qualifying assets for mortgages), and the security of that retirement protection can support a greater willingness to take on a large residential real estate expenditure. The growth in the stock market that has boosted the value of retirement accounts is attributable to many factors, but more than a few analysts consider the “Fed put” to be significant. The Fed put was originally called the “Greenspan put” and is characterized as the Federal Reserve aggressively assisting the economy (and its associated risk taking) in times of difficulty by cutting interest rates and ensuring abundant liquidity. In honor of the passing of legendary and controversial Fed Chairman Alan Greenspan, we bow our heads to the (possible) power of the Greenspan/Fed put.

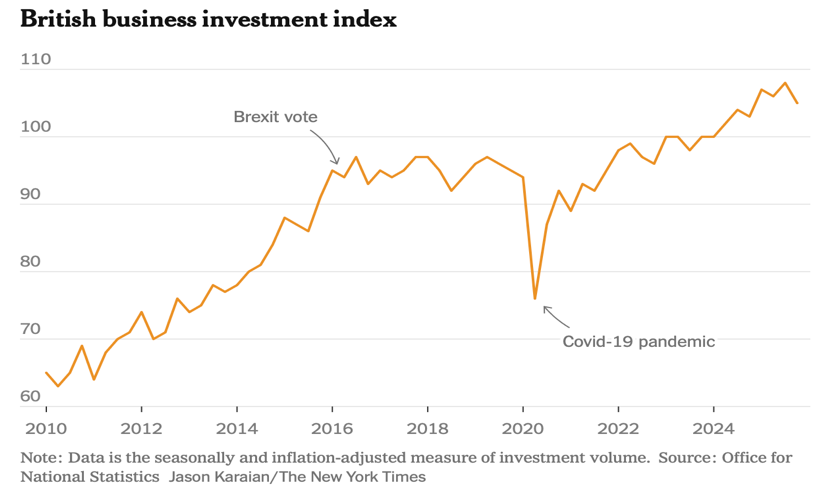

As the United States embarks on the celebration of the 250th anniversary of its breaking away from Britain . . . the divergent experience of the Colonies and their former overseer continues to this day. The resignation of Prime Minister Starmer has encouraged heightened discussion of where Britain has been (or not been) and where it is going (or not going), economically. Much of the debate centers on the long-lasting effect of the Brexit vote to depart the EU (European Union), but economists with longer hindsight will reference a historical, possibly institutional, bias against efficiency, productivity and investment. The new Prime Minister, and the population at-large, face a considerable demand to participate in economic growth increasingly determined by a willingness of the private sector to invest. Both domestic business investment and foreign direct investment have grown at a pace well below the pre-Brexit trend rate, which itself may not have been sufficient to keep up with the US, China, Asian economies, and even selected EU economies.