Stuart Katz, Chief Investment Officer, August 12, 2020

Politics and Markets

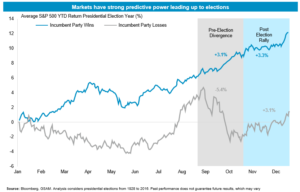

Markets dislike uncertainty and we are within three months of a U.S. presidential election, while in the middle of a pandemic. The S&P 500’s average historical performance during close election years implies that the market will trade in a tight range prior to the presidential election and generate modest appreciation immediately after the election. (see Figure 1)

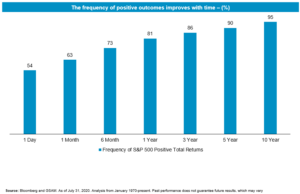

The CBOE VIX “fear index” is currently at ~22 which is above its long term average and almost exactly where it was at the end of the week before the 2016 election.1 While polls have proven to be difficult to rely upon even on the day of a presidential election, it is reasonable to assume volatility will increase between now and election day. However, it’s worth distinguishing between a shorter-term trading portfolio vs. longer duration investment portfolio where the benefit of time and patience is a good antidote for near term uncertainty. While the chance of a positive S&P 500 market return is slightly more than 50% on any given trading day it increases to approximately 75%, 85%, and 90% over 6 months, 3 years and 5 years, respectively. (see Figure 2)2

After the 2016 Trump election, materials and cyclicals appreciated relative to utilities and technology based on the near-term expectation Trump would implement meaningful infrastructure spending. However, the subsequent few years proved the short run market views were inaccurate. Currently, there are concerns about a Biden election rolling back the recent tax cuts. However, after Barack Obama used his political capital from his re-election to push through a tax increase, the S&P 500 in 2013 subsequently posted its best annual gain of 32% in 16 years.3

This suggests that concerns around a Biden victory and subsequent tax hike might create a buying opportunity, all else equal. Ironically, infrastructure might also do well in the hope that the Democrats might borrow money and invest in green renewables and other projects. If they also control the Senate, the pharmaceutical and technology industries will be facing increasing government intervention that may impair near term profit outlooks.

Lean on History

Since 1929, the stock market has performed better under Democratic Presidents than Republican.4

Since 1912, in the 100 trading days leading up to a Presidential election, the market has rallied every time a Republican was ultimately reelected and traded down 80% of the time when a Democratic candidate unseated the Republican.5

Since 1900, there have been six Presidents who have run for re-election when the economy has experienced a recession at some point in the two years before the election. With the exception of Calvin Coolidge in 1924, none of the six were re-elected. Without a recession, the U.S. has re-elected the sitting President every time.

Outlook

The Investment Office expects the deciding issues for markets will be the path of COVID-19, impact of government stimulus and corporate earnings outlook. We believe the market will continue to trade rangebound in the near term as investors await catalysts from headlines around COVID, geopolitics and the U.S. presidential election. Additionally, global central bank policy will influence the recovery which will differ by industry and region.

The most likely path in the aftermath of the pandemic is modestly higher inflation, accommodative monetary policy and higher taxes. Higher inflation expectations tend to be a negative for cash and bonds while neutral for equities and positive for real assets. If the Fed responds to higher inflation with higher interest rates before achieving its 2% target this may prove a headwind for equities trading at high multiples. Higher taxes will need to increase and help finance the debt burden which will strengthen demand for municipal securities. Ultimately, the prudent long-term strategy is a thoughtfully diversified portfolio constructed with real assets and international equities.

After the November election, a scenario of President Biden and Vice President Harris could likely be more China-friendly than Trump and certainly more Europe-friendly. This framework could help Europe and the emerging markets outperform the U.S. markets. Finally, the Investment Office is mindful of other longer-term considerations that include demographics, de-globalization, index construction, ESG, labor costs and social unrest. The markets always have both near-term and long-term risks and opportunities. As a result, one of our first principles is a rigorous process that includes active management in portfolio construction which seeks to buy the “winners” and avoid the “losers” while employing diversification by geography, strategy, asset class and alternatives.

Figure 1

Figure 2

1,2,3 Source: Bloomberg

4 Forbes, Democrats vs. Republicans. July 26, 2016.

5 Sentiment Trader, June 16, 2020

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. This material is for general informational purposes only. It does not constitute investment advice or a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, the opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Any discussion of U.S. tax matters should not be construed as tax-related advice. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. © 2020 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere. A1059