Stuart Katz, Chief Investment Officer, October 28, 2020

WHAT IS YOUR PERSPECTIVE ON THE CURRENT ENVIRONMENT?

First, regarding the health crisis. Covid-19 related issues are still the dominant factor in personal and business activities, but we are encouraged that despite the resurgence of case counts in the US and Europe, mortality rates are lower as compared to previous levels suggesting the medical profession and scientific community have a greater understanding of how to treat the virus.

![]()

Second, regarding the economy. We see continued signs of economic progress across many data points. However, we believe the next twelve months will be a more uneven recovery.

Third, regarding the financial markets. Visibility in the markets is improving as evidenced by meaningful recent earnings revisions to the upside. We expect lower returns across equities and fixed income than the last cycle but better relative returns for equities compared with bonds going forward. Finally, regardless of the Presidential winner personal and corporate taxes will need to rise to pay for past and pending fiscal stimulus and state/local budget shortfalls.

WHAT ARE THE POLICY PRIORITIES YOU ARE PAYING MOST ATTENTION TO?

We are tracking several “top down” policy initiatives but I want to focus on three priorities including taxes, regulation and healthcare.

Taxes

Under a Biden scenario, higher corporate tax rates domestically and internationally and higher individual taxes are likely.

However, investors should not be too narrowly focused on the bottom-line tax impact without the “top down” realization of a stimulus package to accelerate growth and revenues. Remember, Obama passed an increased tax package at the beginning of his second term and the stock market appreciated more than 30% that same year.

Under Biden’s proposal, the US corporate tax rates will go up. In general, the companies that will be most impacted are those that derive a large portion of their revenues from the US. The potential roll back would shift the corporate tax rate in the US from the current 21% to 28%, which would be below the previous 35% tax rate that was in place before the Trump-era tax cuts took effect. We believe tax changes will be a major focus for Biden, with changes likely happening in 2021 for a 2022 implementation.

Finally, the Trump tax cut boosted S&P 500 earnings by approximately 8-9% and the current Biden proposed roll back is estimated to hit earnings by 5-6%.

Regulations

Under Biden there will be more regulation that would impact various sectors including energy, financials and technology around anti-trust and privacy. Practically speaking, we think the tech industry rate of innovation will make it hard for the regulatory regime to permanently impair the growth trajectory where antitrust concerns focus on “harm to the consumer”.

Many technology companies are either free or help to lower the cost of goods and services marking it hard for the DOJ to demonstrate any consumer harm. However, we do see an increased likelihood of substantial one-time fees and penalties and on-going compliance expenses. Many of these technology businesses are operationally very resilient to absorb these issues.

Healthcare

While Biden has many proposals as it relates to healthcare, it is important to remember that there is a limited amount of political capital to allocate in his first year in office. We expect taxes, infrastructure, the pandemic, and the economy to all be priorities for Biden given the current environment. With all of these competing priorities and limited political capital, if healthcare is a focus we expect the priority to be on expanding healthcare coverage. On this front, we believe expansion of the ACA and Medicaid will be prioritized over pursing a public option, which as a reminder, would be a net benefit for insurers in the space.

HOW ARE YOU THINKING ABOUT RISK AS IT RELATES TO THE UPCOMING US ELECTION?

A few considerations include the stimulus and time horizon.

Fiscal Stimulus

After the election, we are expecting the F-Bomb of fiscal stimulus to be employed with either a unified sweep or divided scenario.

The more important consideration is whether it’s fiscal stimulus with a capital “F” or lower case “f” where a unified government will provide closer to $2-3 trillion of stimulus vs. $1-2 trillion if it’s a divided government. We also believe the stimulus plus uneven economic recovery will be sufficient to prevent a double dip recession.

Near Term vs. Long Term Perspective

We caution investors against quick emotional reactions. We all recall watching the election returns four years ago. As the returns showed Donald Trump collecting the electoral college votes, the stock futures were melting downward. At one point, they indicated an opening of nearly nine hundred points in the red. Less than twenty-four hours later, the losses were erased, and the markets finished with substantial gains however the sectors such as infrastructure which were perceived as early beneficiaries ultimately underperformed other sectors.

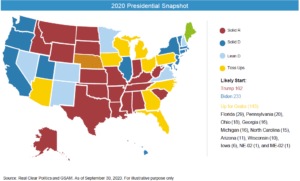

HOW ARE YOU THINKING ABOUT THE RISK OF A CONTESTED ELECTION AND WHAT THAT MAY MEAN FOR MARKETS?

We have seen the VIX “fear gauge” market pricing elevated volatility after November 3rd .

In our base case, because there is substantial voting by mail, we expect there to be delays in counting votes in certain key states such as Pennsylvania.

In terms of getting clarity of election results. Our focus is on Florida which counts it ballots before and on election day and may provide a clear sense who won the state late that night. If Biden is the Florida winner, we get a better sense of which way the election will likely go because it is hard to construct electoral vote maps where Trump can win in the absence of having Florida.

We have conviction that we will have a president sworn in on Jan 20th with a result that is seen as legitimate. From an investment perspective, we believe any volatility on the heals of contested election risk will be uncomfortable in the moment but will create opportunity for long term investors who keep their goals and plan in mind. We recommend using the volatility to add to high conviction positions and rebalance to your strategic targets.

WHAT KEY INVESTMENT THEMES SHOULD INVESTORS CONSIDER?

Equities

We think US investors continue to underappreciate Emerging Markets for total return especially with the backdrop of further dollar weakening sparked by anticipated fiscal stimulus and potential COVID vaccines. Additionally, the COVID

crisis is accelerating attractive sustainable and impact investment opportunities.

Alternatives

We have two priorities. Distressed Investing and Multi Family Real Estate.

We expect to see rising corporate default rates beyond 10% annually and corporate restructurings of so-called “good companies with bad balance sheets” offering opportunities for total return and potential return diversification for qualified purchasers.

Additionally, real estate multi-family properties may offer durable yield and portfolio ballast as a substitute for some portion of the traditional fixed income allocation.

Fixed Income

We also believe the various election outcome scenarios likely clear the path for at least of $1 trillion of stimulus and some forecasts for GDP growth in 2021 in excess of 5%.

Such spending may prove to be more inflationary than what the bond market is currently anticipating. Additionally, over the next 12 months as COVID uncertainty dissipates and the recovery takes hold long term rates would likely move modestly higher, causing the yield curve to steepen and inflationary breakevens may widen. Combined with the Fed wanting to achieve its objective of a modest inflation target overshoot we could possibly see a potential opportunity in TIPs for certain investors.

WHAT OTHER TOPICS ARE YOU DISCUSSING WITH CLIENTS?

The conversations we are having with clients focus on three key points including (i) underlying company fundamentals matter more than timing the markets, (ii) the importance of alternatives to complement a core long biased portfolio and (iii) the need to keep politics out of your portfolio.

We also advocate for active investment combined with selective passive solutions where quality managers apply judgement and common sense to deeply understand changing companies, industries and geographies. This is a time to invest with conviction in the winners and maintain discipline to avoid the losers.

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only. It does not constitute investment advice or a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, the opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Any discussion of U.S. tax matters should not be construed as tax-related advice. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2020 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.