By Stuart Katz, January 19, 2021

With lawmakers embroiled in historic impeachment proceedings in the wake of the Capitol Hill event, the markets are once again confronting headlines most never thought imaginable. As much as we’d like to escape with a tidy perspective on 2020, there are signs volatility is following us into 2021.

Democratic victors of Georgia’s Senate elections ushered in a new “unified government.” But the current split suggests that more progressive elements of President-elect Joseph R. Biden Jr.’s agenda won’t simply coast through, especially as many moderate Democrats face mid-term elections in 2022.

Democratic victors of Georgia’s Senate elections ushered in a new “unified government.” But the current split suggests that more progressive elements of President-elect Joseph R. Biden Jr.’s agenda won’t simply coast through, especially as many moderate Democrats face mid-term elections in 2022.

However, we expect Biden to pass more of his agenda, including Covid-19 relief, tax hikes, climate change, infrastructure and healthcare reform. We also anticipate modestly more inflation and lower real interest rates than previous outlooks.

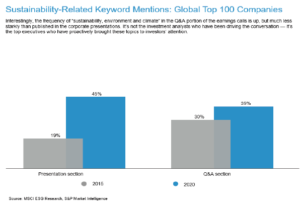

The upshot of this rare political confluence is that portfolio construction is now primed for selective equity risk assets driven by greater fiscal spending and faster GDP growth. The themes associated with this positive outlook include emerging markets, sustainable opportunities, healthcare transformation and alternative investments.

The upshot of this rare political confluence is that portfolio construction is now primed for selective equity risk assets driven by greater fiscal spending and faster GDP growth. The themes associated with this positive outlook include emerging markets, sustainable opportunities, healthcare transformation and alternative investments.

It is critical for investors to stick with their financial plan, as we believe time in the market is more important than timing the market. Broad equity indexes can stay expensive on a price-to-earnings basis for an extended period as earnings recovery strengthens during 2021. Broadly speaking, we anticipate asset class returns to be modest relative to history.

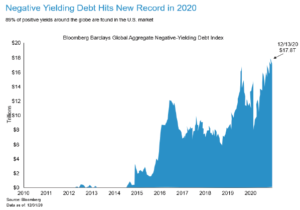

However, we are relatively more cautious regarding credit risk during the recovery period and prefer more limited overall credit exposure intentionally constructed with shorter duration and higher quality assets. In essence, we advocate deliberately avoiding excess risk in credit portfolios and focusing on capital preservation and stability rather than reaching for yield. Investors who work with disciplined active managers who know what they own are the ones who have the conviction to stay invested.

However, we are relatively more cautious regarding credit risk during the recovery period and prefer more limited overall credit exposure intentionally constructed with shorter duration and higher quality assets. In essence, we advocate deliberately avoiding excess risk in credit portfolios and focusing on capital preservation and stability rather than reaching for yield. Investors who work with disciplined active managers who know what they own are the ones who have the conviction to stay invested.

We remain vigilant with respect to the biggest near-term risks, namely, further social unrest and Covid-19. However, we believe these concerns are unlikely to cause a double-dip recession given the strong monetary and policy support combined with meaningful aggregate consumer savings.

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, the opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2020 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.