By Stuart Katz, March 29, 2021

With Bitcoin recently reaching record highs—in excess of $60,000 according to Bloomberg—investors may be conflicted over whether this more than $1 trillion market1 is too enticing to ignore or too volatile to touch.

Whether this asset, which received a market-moving $1.5 billion demand last month with a buy from Tesla, is a good opportunity depends first on an investor’s risk tolerance. Beyond that, its potential as a successful investment hinges on how it interacts with the rest of the portfolio. To understand whether it’s a good “team player,” we need to understand the evolution of the asset, the shifting paradigm of portfolio construction, and the interplay between the two.

In short, we see the advantages of Bitcoin in the context of a highly volatile return profile. That is not to say, however, that the asset is the only alternative to counter a low-yield environment and rising inflation expectations. To be sure, Bitcoin is not an ideal candidate to provide the ballast and income of high-quality credit nor an inflation hedge. But for portfolios that need to deliver long-term returns to clients, it’s time to explore alternatives—including but not limited to— certain real estate strategies which can also serve as an inflation hedge.

Accepting the Waning Relevance of the 60/40 Portfolio

For decades, equities and fixed income have played clear roles in the classical paradigm of portfolio construction. Investors have relied on equities to deliver long-term capital growth above the rate of inflation, dampening volatility from a 60 percent equity allocation with 40 percent exposure to high-quality bonds.

For the past 40 years, this worked because equities and government bonds were reliably negatively correlated: Bonds appreciated when equity markets fell, keeping the overall portfolio on an even keel by diversifying the equity risk.

Now that historic dual benefit of income and ballast provided by quality fixed income is materially challenged. As central banks have manipulated interest rates to near all-time lows, the yield component of the return on a portfolio of bonds has essentially disappeared.

That leaves capital appreciation as the sole source of future returns. But bond prices are now more likely to fall as yields increase with rising inflation expectations and equity price/earnings multiples broadly compress. These changing dynamics have forced investors to consider new allocations in their portfolio.

Enter Bitcoin: A Draft Pick for a Redesigned Team

Bitcoin, created in 2009, is the oldest cryptocurrency and has the most aggregate value at approximately $1 trillion. Unlike stocks and commodities, it trades 24/7 away from any regulated exchange, and is seen by many as an alternative to fiat currency, specifically the U.S. dollar and other traditional currencies.

Unlike stocks and bonds, Bitcoin doesn’t have any industrial use, utility or intrinsic value based on earnings, dividends or cash flows. But as with traditional currency, it holds value as long as people accept it as currency. Payment platforms such as PayPal and Square accept payments in Bitcoin, but a conversion to a fiat currency is required before the payments settle.

Bitcoin is created when programmers solve complex computations that are added to the blockchain—the public ledger that records all Bitcoin transactions—in a process called mining. It is generally believed there is a finite supply of 21 million Bitcoins to be mined. With roughly 2.4 million remaining of that supply as of January 20212, many anticipate their value to continue increasing over time.

The advantages of the purely digital asset are well-known. Bitcoins are stored in electronic programs called wallets secured by passwords. Once they are transferred, they can’t be retrieved nor can their transactions be disputed.

While it lacks a regulated exchange, Bitcoin has been increasingly embraced by large public companies and other institutional investors and endowments as a viable alternative to cash and other assets such as gold. Telsa recently announced it will accept cryptocurrency payments only in Bitcoin.

The asset, of course, is not without risks and disadvantages. Mining, a time-intensive process concentrated in Russia, Belarus and China, raises geopolitical and environmental concerns because of its significant draw on computing power and electricity.

And while their digital nature allows for verifiable and transparent transactions, those password-accessible features have little value for someone who no longer has a password. According to The New York Times, approximately 20% of Bitcoin, valued at approximately $140 billion, is forever gone because its owners lost their passwords.3

Additionally, the Internal Revenue Service (IRS) considers Bitcoin property rather than currency, and as taxable income if received as compensation as certain NFL players have negotiated. And investors who try to own Bitcoin beyond a digital wallet, such as through a trust structure, could face high fees, illiquidity constraints and valuations that trade at a premium to the underlying Bitcoin net asset value.

Currently, there are a handful of asset managers petitioning the U.S. SEC to approve their Bitcoin exchange-traded funds, compared to Canada, which has three Bitcoin ETFs trading on its exchanges.

What Position can Bitcoin Play on the Team?

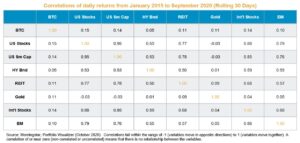

Certain investors may view Bitcoin as a safe-haven asset or diversifier. But, with high volatility and unstable correlations and valuations, even a nominal allocation will consume a large portion of a portfolio’s risk budget and tracking error. Therefore, we view Bitcoin as a speculative call option on a highly volatile return profile.

It’s comforting to know that an investor can lose a limited amount by owning options. But if either the volatility of the underlying finishes well below the volatility paid for the option or the market’s prediction of future volatility drops after purchasing the option, it can be very difficult to make money and, over time, paying too much for options can be a meaningful drag on returns.

It’s comforting to know that an investor can lose a limited amount by owning options. But if either the volatility of the underlying finishes well below the volatility paid for the option or the market’s prediction of future volatility drops after purchasing the option, it can be very difficult to make money and, over time, paying too much for options can be a meaningful drag on returns.

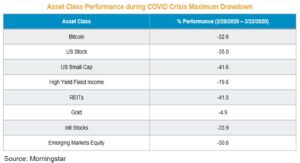

If investors can stomach the volatility, Bitcoin could potentially play a role as an uncorrelated hedge over certain periods of time against equity market downturns. However, investors must be prepared for the downside and understand the limitations of its role on the portfolio team. For example, during the S&P 500 maximum drawdown period from February 2020 to March 2020, Bitcoin did not play the role as a safe-haven asset or portfolio diversifier as it declined 32% vs. the S&P 500 decline of 35%.

So What’s in Your Digital Wallet?

As with any game, there are external forces that teams have little control over—namely, referees and professional leagues. Rules can be changed in the middle of games and sports can fundamentally evolve under the direction of governing bodies, particularly when their popularity begins to snowball.

Those same concepts apply to Bitcoin. Global regulators and policymakers, particularly in the U.S. and China, have become more aggressive about overseeing digital dollars such as Bitcoin and central bank digital currency (CBDC) as cryptocurrencies have undergone expansive growth. Bitcoin could be outlawed, similar to when the U.S. government made it illegal to privately own gold as part of the Gold Reserve Act of 1934. At the same time, U.S. regulators have indicated a growing receptiveness to issuing a digital dollar:

“To the extent that somebody is offering an investment contract or security that’s under the SEC’s remit, and they have exchanges that operate there, then we have to make sure there’s investor protection.” On the other hand, “If it’s not that, and it’s a commodity, as Bitcoin has been deemed to be, then it’s either a question for Congress … or it’s possibly a question for the Commodity Futures Trading Commission (CFTC).”

The SEC must ensure that crypto markets “are free of fraud and manipulation,” elaborating: “I think that’s the greater challenge, frankly, because some markets, usually operating overseas, have been rife with fraud.”— President Biden’s nominee to head the U.S. Securities and Exchange Commission, Gary Gensler (Mar. 2, 2021) 4

Developing a digital dollar is a “very high priority project” for the Federal Reserve.— Federal Reserve Chair Jay Powell (Feb. 23, 2021) 5

“Too many Americans really don’t have access to easy payment systems and to banking accounts, and I think this is something that a digital dollar—a central bank digital currency—could help with.”—Treasury Secretary Janet Yellen (Feb. 22, 2021) 6

“My hunch is that [a digital euro] will come . . . If it’s cheaper, faster, more secure for the users, then we should explore it.”—European Central Bank President Christine Lagarde (Nov. 12, 2020) 7

“CBDC, whilst offering much potential, also raises profound questions … The Bank of England is exploring these issues …”—Bank of England Governor Andrew Bailey (Sept. 3, 2020) 8

These discussions have raised questions about the potential design, availability and functionality of a U.S. CBDC and, accordingly, a host of policy and regulatory questions, touching on payment finality, commercial law, data privacy, financial crimes, monetary policy and commercial banking sector implications.

The Fed’s authority to issue a retail CBDC is unclear under existing law; legislation is likely necessary to authorize and implement it. Electronic central bank money exists in the U.S. today. The Federal Reserve System issues and allows its members to hold and transact in U.S. dollars in electronic-only form through accounts at Federal Reserve Banks. The key difference between existing central bank digital money—available only to Federal Reserve member banks through Federal Reserve Bank accounts—and CBDC is that a CBDC would be available broadly to retail and commercial users.

Individuals and businesses could directly hold CBDC and use it for payments, rather than using commercial bank deposits or other payment instruments like checks, debit cards and credit cards for this purpose. As of March 2021, three bills to implement a digital dollar have been introduced in the U.S. Congress. None has meaningfully progressed to committee or full chamber votes. 9

All three bills provide for Federal Reserve Banks to establish and maintain digital dollar wallets branded as FedAccounts that would allow individuals and businesses to hold dollar balances consisting of digital ledger entries recorded as liabilities in the accounts of any Federal Reserve Bank. However, there is debate over whether a token-based system, which relies on verifying the validity of the object used to make a payment, or an account-based system, which relies on verifying the identity of the payer, would be best.

The best outcome, perhaps, is one where Bitcoin and other forms of money like the U.S. dollar thrive side by side, performing different and important roles in our economy, our lives and our portfolios.

Sources

1 https://www.statista.com/statistics/377382/bitcoin-market-capitalization/#:~:text=The%20market%20capitalization%20currently%20sits%20at%20more%20than%20600%20billion%20U.S.%20dollars.

2 beincrypto.com, “How Many of the 21 Million Bitcoin Are Left?” 1/13/21

3 New York Times, “Lost Passwords Lock Millionaires Out of Their Bitcoin Fortunes,” 1/12/21

4 https://www.cnbc.com/2021/03/02/biden-sec-pick-gensler-grilled-over-bitcoin-gamestop-mania-and-board-diversity.html

5 https://www.forbes.com/sites/sarahhansen/2021/02/23/fed-chair-powell-says-digital-dollar-is-a-high-priority-project/?sh=4bba68707e4c

6 https://video.snapstream.net/Play/4l8tVHc6SEmzfVvMDklR4p?accessToken=45mrp3l943lu

7 https://www.bloomberg.com/news/articles/2020-11-12/lagarde-says-her-hunch-is-that-ecb-will-adopt-digital-currency#:~:text=%E2%80%9CMy%20hunch%20is%20that%20it,think%20we%20 should%20explore%20it.%E2%80%9D

8 https://www.bankofengland.co.uk/speech/2020/andrew-bailey-speech-on-the-future-of-cryptocurrencies-and-stablecoins

9 https://www.congress.gov/116/bills/s3571/BILLS-116s3571is.pdf; https://www.congress.gov/116/bills/hr6321/BILLS-116hr6321ih.pdf; https://www.congress.gov/116/bills/hr6553/BILLS-116hr6553ih.pdf

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, the opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2021 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere.