By Stuart Katz, Chief Investment Officer

August 31, 2021 – By now it’s clear we are in the throes of a strong economic recovery, one that has shifted into the expansion phase and is on course to gain steam across regions and countries in the second half of the year.

The question isn’t whether we will have a powerful and sustainable recovery, but how powerful and sustainable it will be. And more critically, can it be sustained without fueling a permanent, rising inflation?

More specifically, the question for investors is whether growth in the face of various risks will be strong enough to meet optimistic earnings expectations without causing sustained inflationary pressures that could force the U.S. Federal Reserve and other central banks to tighten monetary policy.

Stocks saw a lot of volatility in 2020, particularly in the first half of the year with 38 single day S&P 500 stock moves +/-2%. This year, it’s been a smoother ride. As of July 31, we have had only four +/-2% days, according to Bloomberg. However, this aggregate benchmark is misleading as different geographies and asset classes such as emerging markets, digital currencies, special purpose acquisition companies and “meme stocks” have experienced elevated drawdowns and volatility.

Economic recovery accelerates, but with uncertain path

We expect global growth to be sequenced rather than synchronized, bolstered by vaccine progress, continued fiscal and monetary support, pent-up consumer demand and excess corporate balance sheet cash used to support buyback programs, M&A and capital investment. While the highly contagious Delta variant has created some of the recent economic vulnerabilities, we see indications these will improve as the current COVID wave dissipates. We are confident this growth will persist well into next year with easy financial conditions and rising global vaccination rates.

We are bracing for lower, more range bound returns with more volatility for risky assets. We also expect to see fewer tailwinds from rising valuation multiples and less margin of safety and diversification benefits from low yields and tight credit spreads.

We see risk, however, building in a number of areas. While we are heartened by the rising vaccination rates, the Delta variant and other virus mutations still threaten to drive up infection rates and trigger more restrictions. Equity and credit investors, of course, will continue to worry about central bank tightening and its impact on growth and duration exposure, respectively.

Further, we anticipate continued tensions as part of the bi-polar U.S.-China rivalry and disruptions from other geopolitical issues such as cybersecurity threats. We also face elevated inflation risks due to supply chain shortages, the housing boom, labor shortages and deglobalization.

Equities still rule—assuming no jumps in inflation

So what does this mean for investment opportunities? In short, we remain broadly pro-risk in our asset allocation, overweighting equities over fixed income, while favoring shorter duration credit within fixed income. We recommend a deliberate exposure to both value and growth.

Valuations remain high, but we believe there are still no practical alternatives to equities, as long as interest and inflation rates remain low. Generally speaking, equities can do well with a modest uptick in inflation but not a significant acceleration. Corporate profit growth is likely to remain the engine of further equity gains, limiting multiple expansion.

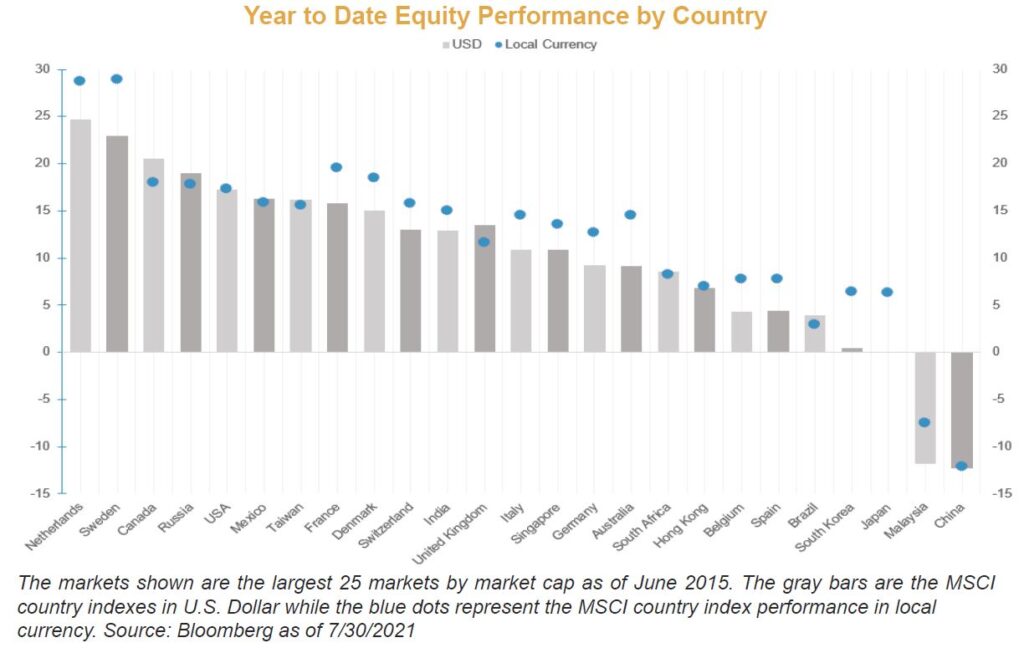

We are particularly optimistic about performance resulting from the varying speeds of economic recovery among geographic regions across the globe. We may see outperformance, for example, among non-U.S. equities as earnings per share for companies in many non-U.S. markets has not rebounded as quickly or strongly as it has for U.S. companies. The reflation theme plays well especially in non-U.S. markets which tend to be more exposed to value and cyclical sectors.

Recent weakness and volatility has been much more pronounced across emerging markets, and Asia in particular, reflecting the ongoing uncertainty in Chinese regulatory and social policy. With room for supportive monetary and fiscal support during this regulatory adjustment phase, we maintain a positive outlook for China and the broader emerging markets region given current valuations.

On the fixed-income front, we see a trend toward alternatives. For bond investors, rising inflation expectations and yields pose duration/interest rate risks, prompting an asset allocation shift to alternative yield and total return solutions in real estate and private credit opportunities.

We note, however, that the Fed’s more hawkish tone reduces the risk of inflation overshoot, increasing the odds of rising real yields. In addition, further spread tightening seems limited, providing less support to move down in credit quality.

Additionally, we believe the apparent disconnect between low U.S. Treasury yields and the strong restart of economic activity is partly caused by technical factors, such as excess liquidity driving strong demand for safe assets, traders unwinding positions that counted on rising bond yields, and aging demographics and foreign buying of Treasuries in search of yield. We believe the ultimate trajectory however, should be for higher nominal and real yields—in part why we underweight credit in portfolios and see risks to fixed income overall.

Across the environmental, social and governance (ESG) landscape, we see a number of public and private investment opportunities. Chief among them are areas related to climate change, which can boost global growth relative to a no-action scenario.

The green transition will unfold at the industry and sector level, warranting a purposeful asset allocation and security selection process.

We see two key aspects in the climate transition: technology and policy. The tech transition has already begun in some key sectors such as utilities and autos, and as deadlines approach to achieve net zero carbon dioxide emissions, we expect public policy initiatives and private demand to increase—potentially resulting in an accelerated transition.

Building a post-pandemic portfolio

A year ago, we asked how deep our recession will be as we gauged the severity of our economic contraction. Then, we asked what it will take to reverse our historic GDP decline as we turned our focus to rebounding. Now, in our expansion phase, we are wondering how strong our recovery will be and how long will it last.

Overall, we see a climate favorable for a more balanced exposure to non-U.S. geographies and asset class exposure to small- and mid-cap companies including value/cyclical companies with a cautious credit exposure. We also see thematic openings among emerging markets, healthcare innovation, sustainable opportunities and alternative strategies providing diversified return streams and ballast.

As the global economy and corporate profits continue to recover, investors should consider a few policy initiatives when building portfolios for a post-pandemic environment. Those include an accommodative monetary policy framework of “average inflation targeting” generating negative real interest rates, as well as substantive fiscal repair and recovery spending programs. Over the horizon, we view the more critical monetary landscape change—the Fed’s launch from zero rates—as still a distant event and believe we are unlikely to see a repeat of 2013’s taper tantrum.

Disclosures

Investment advisory services offered through Robertson Stephens Wealth Management, LLC (“Robertson Stephens”), an SEC-registered investment advisor. Registration does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. This material is for general informational purposes only and should not be construed as investment, tax or legal advice. It does not constitute a recommendation or offer to buy or sell any security, has not been tailored to the needs of any specific investor, and should not provide the basis for any investment decision. Please consult with your Advisor prior to making any Investment decisions. The information contained herein was carefully compiled from sources believed to be reliable, but Robertson Stephens cannot guarantee its accuracy or completeness. Information, views and opinions are current as of the date of this presentation, are based on the information available at the time, and are subject to change based on market and other conditions. Robertson Stephens assumes no duty to update this information. Unless otherwise noted, the opinions presented are those of the author and not necessarily those of Robertson Stephens. Indices are unmanaged and reflect the reinvestment of all income or dividends but do not reflect the deduction of any fees or expenses which would reduce returns. Past performance does not guarantee future results. Forward-looking performance targets or estimates are not guaranteed and may not be achieved. Investing entails risks, including possible loss of principal. Alternative investments are only available to qualified investors and are not suitable for all investors. Alternative investments include risks such as illiquidity, long time horizons, reduced transparency, and significant loss of principal. This material is an investment advisory publication intended for investment advisory clients and prospective clients only. Robertson Stephens only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of Robertson Stephens’ current written disclosure brochure filed with the SEC which discusses, among other things, Robertson Stephens’ business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. © 2021 Robertson Stephens Wealth Management, LLC. All rights reserved. Robertson Stephens is a registered trademark of Robertson Stephens Wealth Management, LLC in the United States and elsewhere. A1153