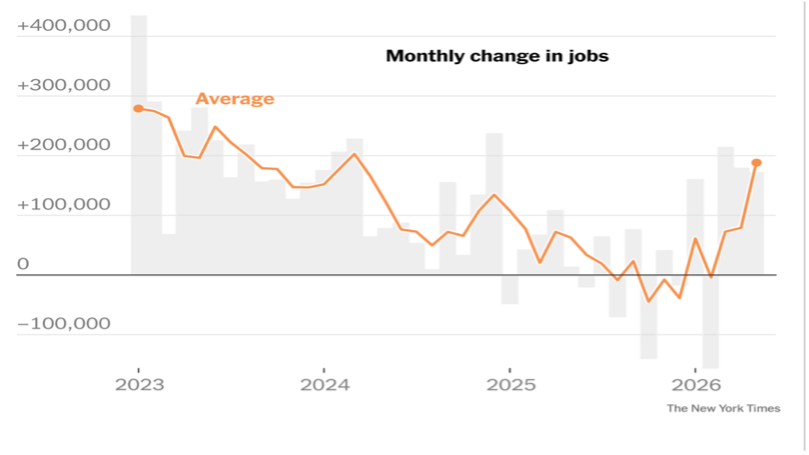

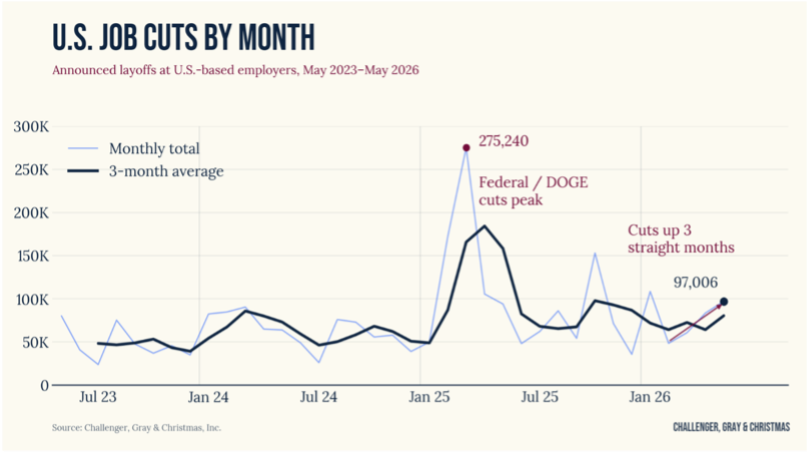

US Nonfarm Payrolls rose by an impressive 172,000 in May. Also notable was the sharp upward revision in March employment by 29,000 jobs and April employment by 64,000 jobs (placing April job growth at almost the same level as May). Unemployment held steady at 4.3%. Substantiating current estimates of GDP growth of 3% or higher in the second quarter, US labor markets appear to be strengthening, albeit not in every job category or sector. A significant portion of May job growth was in health care and the leisure, hospitality and entertainment industry. By contrast, the sharp increase in Challenger job cuts announced earlier – the highest level of private sector monthly cuts since May 2020 —was concentrated in the tech sector.

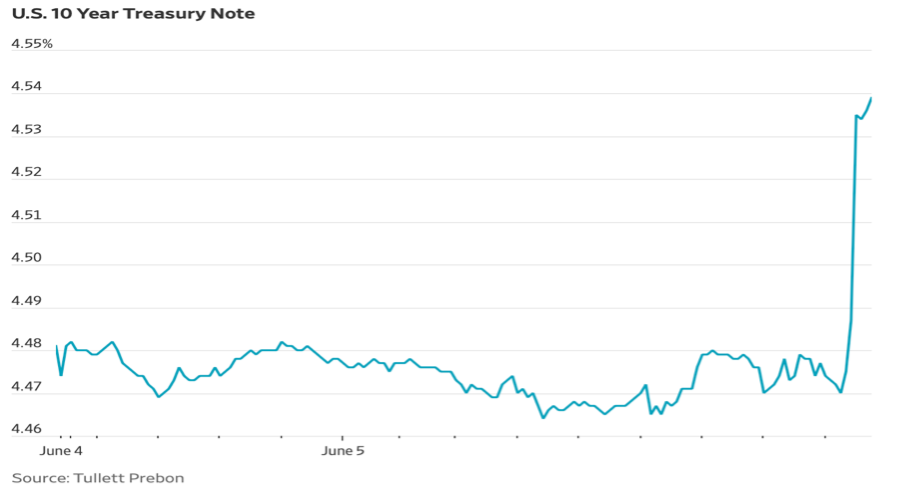

One early but clear reaction to the strong job numbers was witnessed in bond markets (see the Five Charts for the Week That Was, May 22 for greater detail on global bond markets and their power and influence). Labor markets do not presently seem to demand the attention of the Federal Reserve, freeing the Fed to concentrate on controlling inflation through a possible rate hike. Contributing to the optimism of monetary authorities on employment are temp agency reports of increased jobs for temp workers and a rising inventory of unfilled jobs. Although a higher Fed Funds rate is still not the base-case forecast of most analysts at this time, credit markets are decidedly reacting to an increasing possibility that some form of monetary tightening may be in the cards.

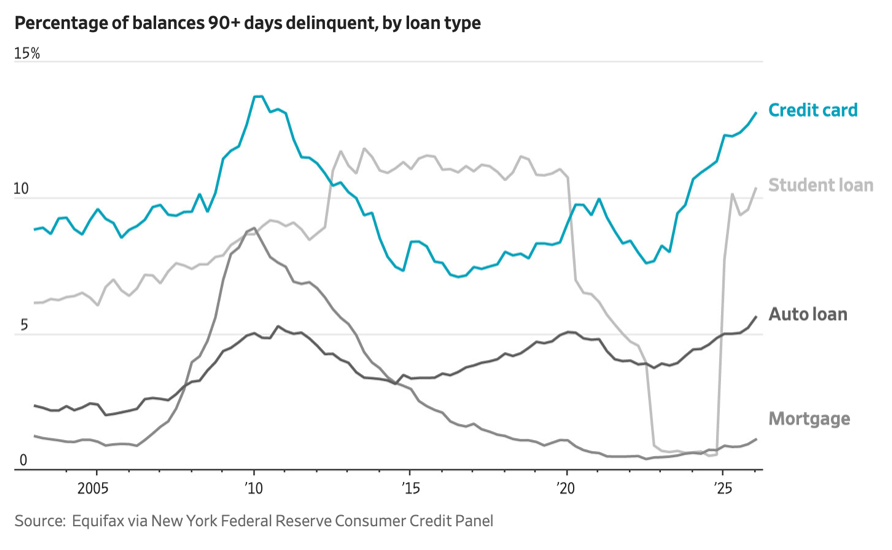

The timing of rising 10-year Treasury yields coincides with increasing consumer debt delinquencies, as can be typical at certain points in an economic cycle and not exclusively during downturns. Lenders have yet to express significant concerns, and the relatively low level of mortgage debt problem loans is notable. The high cost of a home purchase and the resulting weakness in housing sales have essentially limited some of the potential problems; households have not demonstrated much appetite for “stretching” to buy as much house as they can.

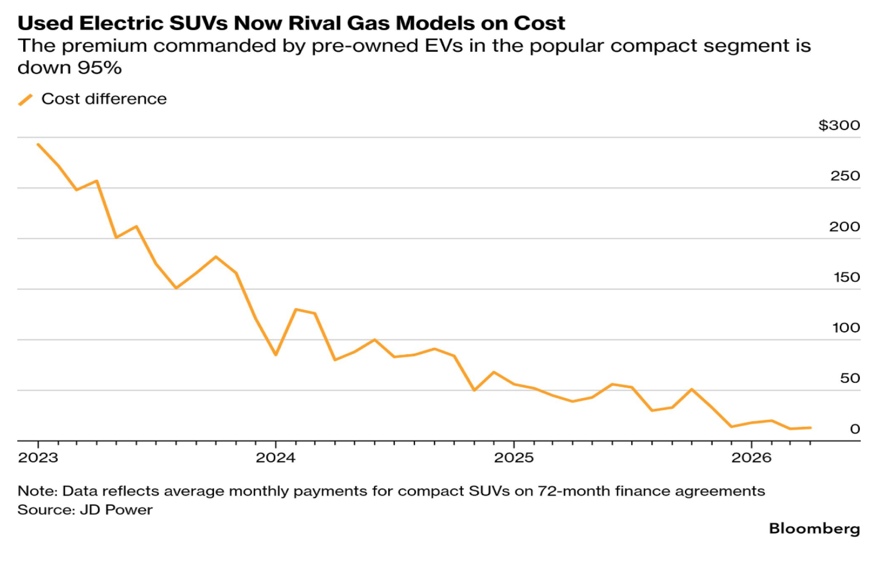

US automakers have been pessimistic about new-car sales in 2026. Recently, it has been estimated that as many as 1 million new car buyers have “disappeared” from the market, forced to the sidelines by the high prices and higher financing costs of new vehicles. Yet, people do need transportation, and cars do break down. The US used car market is alive and well, with an interesting twist provided by a somewhat unexpected increase in demand for used electric vehicles. It is not only the high price of gasoline that is shifting buyer interest; the large number of used electric vehicles available for purchase has reduced prices relative to non-electric used cars such that electric vehicles are now a direct competitor in the used car market. Given that the challenges of electric vehicles remain for many drivers – charging requirements and battery duration, primarily— there is a reluctance to pay a premium. But in an environment of $5+ gas prices, there is now definitely a reason to take a look. Used electric vehicles have increased by more than 30% this year, though such vehicles still represent only 2% of the market.